A Trader's Guide to Shorting a Put Option

If a stock moves past your strike, the option can be assigned — meaning you'll have to sell (in a call) or buy (in a put). Knowing the assignment probability ahead of time is key to managing risk.

Posted by

Related reading

A Step-by-Step Covered Calls Example for Consistent Income

Unlock consistent income with our step-by-step covered calls example. This guide breaks down the strategy, risks, and outcomes to help you trade confidently.

Long Call and Short Put The Ultimate Synthetic Stock Guide

Unlock the power of the long call and short put strategy. This guide explains how synthetic long stock works, its benefits, risks, and how to execute it.

What is a Call Spread? A Clear Guide to Bull and Bear Spreads

What is a call spread? Discover how bull and bear spreads limit risk and sharpen your options trading strategy.

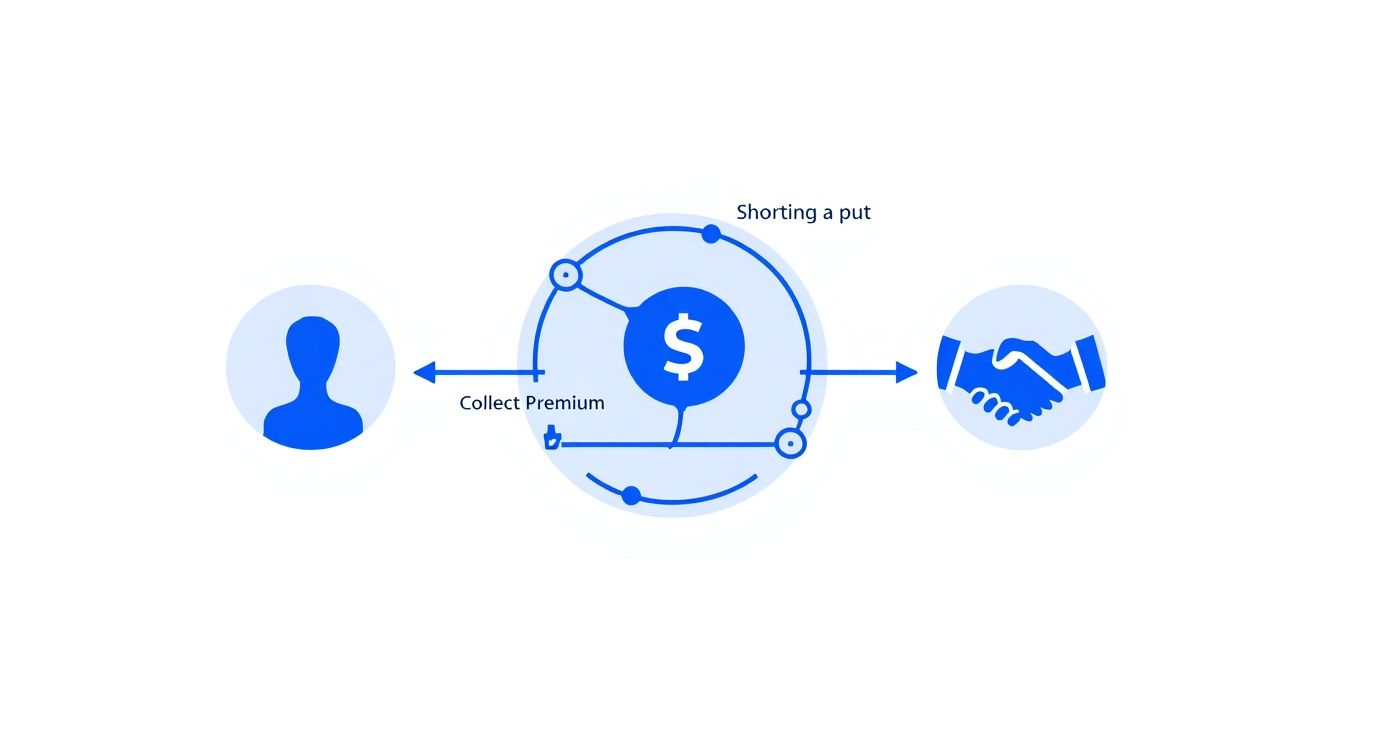

Shorting a put option is a bit like acting as an insurance company for a stock. You get paid an upfront fee (the premium) for agreeing to buy shares from someone if the price drops below a certain level by a specific date.

It’s a powerful way to generate income or buy a stock you already like at a discount.

What Shorting a Put Option Really Means

When you short a put, you’re selling someone else the right to sell you 100 shares of a stock at a specific price, known as the strike price. In exchange for taking on that obligation, you immediately collect a cash premium.

This strategy is perfect for when you're neutral to bullish on a stock. You believe the price will either stay where it is or go up.

Put sellers usually have one of two goals in mind:

- Consistent Income: If the stock’s price stays above your strike price when the option expires, it becomes worthless. You simply keep the entire premium you collected as pure profit. You never have to buy a thing.

- Buying Stock at a Discount: Let's say you want to own a stock, but you think its current price is a little too high. You can sell a put at a lower strike price you'd be happy to buy at. If the stock falls and you're assigned the shares, your actual purchase price is the strike price minus the premium you were paid. You essentially get a built-in discount.

Before we dive deeper, let's summarize the key aspects of this strategy.

Short Put Strategy at a Glance

This table breaks down the core characteristics of a short put trade. It's a quick reference for understanding what you're getting into.

| Characteristic | Description |

|---|---|

| Strategy Goal | Generate income or acquire stock at a lower effective price. |

| Market Outlook | Neutral to Bullish (you believe the stock will stay flat or rise). |

| Maximum Profit | Limited to the premium received when you sold the option. |

| Maximum Risk | Substantial; the stock could theoretically fall to zero. |

| Break-Even Point | Strike Price - Premium Received |

| Ideal Scenario | The stock price stays above the strike price through expiration. |

This table shows that while the profit is capped, the strategy offers a clear path to income if your market outlook is correct.

The Core Agreement of a Short Put

The person buying the put from you is looking for protection. They want the ability to unload their shares at your agreed-upon strike price, no matter how far the stock might fall.

You, as the seller, are making a calculated bet that the stock won’t drop below that strike price before the option’s expiration date.

In essence, you are paid a premium to express a specific belief: that a stock will remain stable or rise in value over a defined period. This makes it a popular strategy for investors looking to create cash flow from stocks they are comfortable owning.

This give-and-take is the heart of the short put. It allows you to set your own terms for buying a stock while getting paid to wait. Next, we’ll explore the mechanics of how this trade is structured and its potential outcomes.

How a Short Put Trade Actually Works

Think of selling a put option as a simple agreement with a clear beginning, middle, and end. When you sell a put, you’re creating a contract with three core pieces: the underlying stock, an agreed-upon strike price, and a specific expiration date.

Your goal is pretty straightforward: you want the stock’s market price to stay above your chosen strike price until the contract expires. If you’re right, the option becomes worthless, the obligation disappears, and the premium you collected is yours to keep as pure profit. For an income-focused trader, this is the perfect outcome.

This visual breaks down that core exchange. You receive cash upfront in exchange for taking on an obligation.

As the diagram shows, the trade is a simple give-and-take. You’re being paid for your willingness to buy a stock at a predetermined price if the buyer chooses to sell it to you.

The Break-Even Point Calculation

The single most critical number you need to master is the break-even point. This is the exact stock price at expiration where you don't make or lose a dime. Anything above this price is profit; anything below is a loss.

The formula couldn’t be simpler:

Break-Even Price = Strike Price – Premium Received

Let’s say you sell a put with a $100 strike price and collect a $3 premium ($300 per contract). Your break-even point is $97. So long as the stock closes above $97 on expiration day, your trade will be profitable. This basic math is the bedrock of managing your risk.

The Three Outcomes at Expiration

When the expiration date finally arrives, only one of three things can happen to your short put. Knowing these scenarios ahead of time removes any guesswork and lets you anticipate what’s next.

Let's walk through each possibility:

- Stock Price is Above the Strike Price: This is the best-case scenario. The option is "out-of-the-money" and expires worthless. You keep 100% of the premium, and your obligation to buy the shares simply vanishes. The trade is over, and it was a success.

- Stock Price is Between the Strike and Break-Even Price: Here, the option is "in-the-money," and you'll be assigned the shares—meaning you have to buy 100 shares at the strike price. But because the premium you collected helps offset the cost, you still walk away with a small profit.

- Stock Price is Below the Break-Even Price: The option is now deep "in-the-money." You will be assigned the shares at the strike price, but your unrealized loss will be greater than the premium you collected. At this point, you own the stock at a cost basis higher than its current market value.

Cash-Secured Puts vs. Naked Puts

When you short a put, the most critical distinction is whether it's "cash-secured" or "naked." While both involve selling a put contract, this single difference completely changes the game—it alters your risk, what your broker demands from you, and why you’d even make the trade in the first place.

This choice is what separates a conservative income strategy from high-stakes speculation.

The Cash-Secured Put Approach

Think of a cash-secured put as making a promise with the money to back it up. You sell the put, and at the same time, you park enough cash in your account to buy 100 shares of the stock at the strike price if you have to.

This tells your broker—and more importantly, yourself—that you’re fully prepared to make good on your obligation if the stock price drops and the shares get assigned to you.

Because the cash is already set aside, the risk is perfectly clear. Your maximum possible loss is the strike price (times 100 shares) minus the premium you pocketed upfront. It’s a favorite strategy for investors who are genuinely willing—or even hoping—to buy a stock they like at a discount.

- Goal: Mostly for generating income, but also a great way to enter a stock position at a price you choose.

- Risk Profile: Defined and limited. You know exactly what’s on the line from day one.

- Margin: Simple. It's the cash you've already earmarked to buy the shares, minus the premium you received.

The Naked Put Approach

A naked put (or unsecured put) is the polar opposite. You sell the contract without setting aside the cash to buy the shares. You’re selling the promise "naked"—without any collateral.

This cranks the risk up to eleven. If the stock price craters, you're still on the hook to buy 100 shares at the strike price, but now you have to scramble to find the cash.

A naked put exposes you to substantial, sometimes catastrophic, losses. In theory, the stock could go to zero, leaving you with a massive bill. This makes it a tool almost exclusively for seasoned traders with a high tolerance for risk.

Naturally, brokers are much stricter about letting traders sell naked puts. They’ll require a significant amount of margin, calculated with complex formulas based on the stock's price and volatility. The odds of getting a dreaded margin call—where your broker demands more cash immediately—are far higher.

Because of the massive risk involved, most investors, especially those new to selling puts, should stick exclusively to the cash-secured method. It’s a smarter, safer way to play the game. Analysis of options data from providers like OptionMetrics has repeatedly shown how critical it is to manage the unbounded risk of a naked position. You can learn more about how historical data helps analyze options strategies.

Calculating Your Potential Profit and Loss

Alright, let's move past the theory and get our hands dirty with some real numbers. To really wrap your head around shorting a put, you need to see exactly how the math works out in different situations. This will help you map out the financial outcomes before you even think about placing a trade.

We'll start with the best-case scenario where the stock plays nice, and then we'll look at what happens when it moves against you. For each example, we'll zero in on the most important number: the break-even price.

Scenario 1: The Ideal Outcome

Imagine XYZ Corp is currently trading at $52 a share. You're feeling bullish and believe the stock will stay above $50. You decide to short a put option with these details:

- Strike Price: $50

- Premium Received: $2.00 per share ($200 total for the contract)

- Expiration: 30 days from now

Your goal is simple: for XYZ to close above $50 on expiration day. If it does—let's say it closes at $55—the option you sold expires worthless. The buyer has no reason to use it.

You get to keep the entire $200 premium as pure profit, and your obligation to buy the shares just vanishes. This is your maximum possible gain, and it's the perfect outcome for this trade.

Scenario 2: Getting Assigned the Stock

Now, let's flip the coin and look at the other side. Expiration day arrives, but this time, XYZ has dropped to $47 per share. Because the stock price is below your $50 strike, you get assigned.

This means you're now obligated to buy 100 shares of XYZ at the $50 strike price you agreed to, costing you $5,000. But remember that $200 premium you collected upfront? It helps cushion the blow.

Your effective cost basis for these new shares isn't $50—it's actually $48 per share ($50 Strike - $2 Premium). With the stock currently trading at $47, you have an immediate unrealized loss of $1 per share, or $100 total on the position.

Let's break down a few more price points to see how this plays out.

Short Put Payoff Scenarios Example (XYZ Stock, $50 Strike, $2 Premium)

This table illustrates the profit or loss you'd realize at various stock prices when your option expires.

| Stock Price at Expiration | Option Action | Profit/Loss per Share | Outcome |

|---|---|---|---|

| $55 | Expires Worthless | +$2.00 | Maximum Profit (keep the full premium) |

| $50 | Expires Worthless | +$2.00 | Maximum Profit (keep the full premium) |

| $48 | Assigned | $0.00 | Break-Even (premium covers the paper loss) |

| $47 | Assigned | -$1.00 | Loss (you own shares at a loss) |

| $45 | Assigned | -$3.00 | Larger Loss (you own shares at a larger loss) |

As you can see, your profit is capped at the premium you received, but your risk is that you end up owning a stock that's falling in price.

Key Takeaway: The break-even point is the line in the sand between making and losing money. In this trade, you calculate it as the Strike Price ($50) minus the Premium ($2), which lands you at $48. Any closing price above $48 at expiration is a win.

Understanding these calculations is your first step. But successfully managing the trade also means keeping an eye on how time decay and volatility are affecting your position. To get a much deeper feel for these dynamics, it’s worth learning about the options trading Greeks, which measure how sensitive your option is to different market shifts. That knowledge adds a whole other layer of precision to your trading.

How to Select and Manage Your Trades

Successfully shorting a put isn’t about luck—it’s about making smart choices backed by data. Nailing your strategy comes down to two things: picking the right strike price and knowing how to manage the trade once it's live. This is where you learn to read the market’s signals and stack the odds in your favor.

One of the best tools for this is an option "Greek" called Delta. While the textbook definition is a bit technical, you can simply think of Delta as a quick probability gauge. A put option with a 0.20 Delta, for instance, has roughly a 20% chance of expiring in-the-money. It's that straightforward.

Many income-focused traders make a living selling low-delta puts (like anything below 0.30 Delta). Why? Because it immediately gives them a high probability of success right from the start. Getting comfortable with how to read option chains is the key to spotting these opportunities instantly.

Using Volatility to Your Advantage

Another critical piece of the puzzle is implied volatility (IV). This metric tells you how much the market expects a stock to swing in the future. When IV is high, it means fear is up, and that makes option premiums much more expensive. For a put seller, this is exactly what you want to see.

Selling puts when implied volatility is high means you collect a richer premium for taking on the same amount of risk. You're essentially being paid more to provide that "stock insurance" because the market perceives a greater need for it.

Think of it like selling umbrellas when the sky turns dark—you can charge a much higher price. This is why many seasoned traders are patient, waiting for those spikes in IV before they even consider opening a new short put position.

Essential Rules for Trade Management

Once your trade is on, your job isn’t done. You have to actively manage it to lock in gains and prevent small losses from turning into big problems. Two simple rules are a great place to start:

- Take Profits Early: Don't feel the need to hold the trade all the way to expiration. A popular rule of thumb is to close the position once you've captured 50% of the maximum possible profit. This frees up your capital and gets you out of the trade, protecting you from a sudden, sharp reversal in the stock price.

- Define Your Exit for Losses: Before you even click "sell," decide where you'll cut your losses. This could be when the stock price hits your strike or when your paper loss hits a certain dollar amount or percentage. Have a line in the sand.

Knowing how to react in different market conditions is also huge. A study on S&P 500 ETF trades found that during high-volatility periods, traders who actively cut their losses did significantly better than those who just held on and hoped for the best. You can check out the full findings in this comprehensive short put management analysis. Having strict exit rules keeps you in control, no matter what the market throws at you.

Understanding the Real Risks and Margin Rules

Every trade has a flip side, and shorting a put is no exception. While your profit is always capped at the premium you collect, the potential loss can sting if the stock takes a nosedive. It's something you absolutely have to get your head around before you hit the "trade" button.

The two big dangers you need to keep on your radar are gap risk and assignment risk. Gap risk is when a stock opens way lower than it closed—maybe some ugly news broke overnight—and you have zero time to react. Assignment risk is the chance you'll be forced to buy the stock before it even expires, which can happen if your put goes deep in-the-money.

The biggest threat when shorting a put isn't just that the stock will fall—it's that it will fall faster than you can manage your position. Smart trading means preparing for the worst-case scenario from the very beginning.

How Your Broker Manages Margin

How your broker handles the cash required for these trades comes down to one simple question: is your put cash-secured or naked?

With a cash-secured put, it's straightforward. The "margin" is simply the cash you’ve already parked in your account to cover the purchase of the shares. There's no fear of a dreaded margin call because the money is already there, waiting.

Naked puts, on the other hand, are a different beast entirely. Since you haven't set the cash aside, your broker will require you to hold a certain amount of capital as collateral. This isn't a fixed number; it can fluctuate based on the stock's price and how volatile the market is. If the stock drops hard, your margin requirement could spike, triggering a margin call where your broker demands more cash, now. You can learn more in our complete guide explaining how brokers calculate these complex options margin requirements.

This isn't just theory; it's how markets work. Research on the 2008 Short-Sale Ban showed that when traditional short-selling gets more expensive or difficult, traders often shift their bearish bets over to the options market. You can learn more about how put options trading is influenced by market structure and see how these dynamics play out.

Of course. Here is the rewritten section, designed to match the expert, human-written style of the provided examples.

Your Top Questions About Shorting Puts

Even once the mechanics click, traders new to shorting puts usually have a few lingering questions. Let’s tackle the most common ones so you can trade with more confidence.

What's the Difference Between Selling a Put and Buying One?

Think of them as two sides of the same coin—complete opposites.

When you sell (or short) a put, you’re paid a premium upfront. In return, you accept the obligation to buy 100 shares of the stock at the strike price, but only if the stock drops below that level. You’re essentially betting the stock will stay flat or go up.

When you buy (or go long) a put, you’re the one paying the premium. This gives you the right, but not the obligation, to sell 100 shares at the strike price. You’re betting the stock is going down.

To put it simply:

- Put Seller: Is bullish or neutral. They want the option to expire worthless so they can keep the premium.

- Put Buyer: Is bearish. They want the stock to fall so their option becomes more valuable.

Can I Lose More Than the Premium I Collect?

Yes, absolutely. This is the single most important risk to understand before you sell your first put.

While your maximum profit is always capped at the premium you received, your potential loss can be significant. If the stock takes a nosedive, you’re still on the hook to buy those shares at the much higher strike price.

Your worst-case scenario? The stock goes to zero. Your loss would be the strike price (times 100 shares) minus the small premium you collected. This is exactly why disciplined risk management is non-negotiable.

Why Would Anyone Sell a Put Instead of Just Buying the Stock?

It really comes down to two powerful strategic advantages that you just don't get with buying shares outright.

- Generating Income: If you’re right and the stock stays above your strike, you simply keep the premium as pure profit. You never had to tie up the large amount of capital needed to buy the shares, making it an incredibly efficient way to generate cash flow.

- Buying Stock at a Discount: Let's say you already like a stock and want to own it, but you think the current price is a little steep. Selling a put lets you get paid while you wait for a better entry point. If the stock drops and you get assigned, your effective purchase price is the strike price minus the premium you were paid—a built-in discount.

Ready to stop guessing and start making data-driven decisions? Strike Price provides real-time probability metrics for every strike, sending you alerts on high-premium opportunities and rising assignment risks. Turn your income goals into an actionable strategy and trade with confidence. Start your free trial at Strike Price today.