A Trader's Guide to Options Trading Greeks

If a stock moves past your strike, the option can be assigned — meaning you'll have to sell (in a call) or buy (in a put). Knowing the assignment probability ahead of time is key to managing risk.

Posted by

Related reading

A Step-by-Step Covered Calls Example for Consistent Income

Unlock consistent income with our step-by-step covered calls example. This guide breaks down the strategy, risks, and outcomes to help you trade confidently.

Long Call and Short Put The Ultimate Synthetic Stock Guide

Unlock the power of the long call and short put strategy. This guide explains how synthetic long stock works, its benefits, risks, and how to execute it.

What is a Call Spread? A Clear Guide to Bull and Bear Spreads

What is a call spread? Discover how bull and bear spreads limit risk and sharpen your options trading strategy.

Options trading can feel like navigating a maze in the dark. But what if you had a dashboard that lit up the path, showing you every twist and turn before you took it? That's exactly what the options Greeks do.

Think of them as the vital signs for your trades. They measure how sensitive your option's price is to changes in the market—like the stock's price, the passage of time, or shifts in overall market fear. Getting a handle on the Greeks is the single biggest step you can take from making speculative guesses to executing calculated, strategic trades.

Decoding the Dashboard of Your Trades

Imagine trying to drive a car with no speedometer, no fuel gauge, and no engine temperature warning. It would be a chaotic, unpredictable, and downright dangerous journey. In the world of options, trading without understanding the Greeks—Delta, Gamma, Theta, and Vega—is just as risky.

These aren't just abstract terms for finance professors. They are practical, real-time indicators that spell out the risks and potential rewards of every single option you buy or sell.

The whole concept of using options trading greeks really took off with the Black-Scholes model back in 1973. This model gave traders a mathematical framework to value options and, just as importantly, to understand their sensitivities. Before that, pricing was more of an art than a science. The Greeks gave traders a shared language to finally talk about and manage risk effectively.

Why Every Trader Needs to Understand the Greeks

If you ignore the Greeks, you're flying blind. It's that simple. A position that looks profitable one minute can flip to a loss the next, all because of factors you weren't even watching, like time ticking away or a sudden drop in market volatility.

By learning what each Greek measures, you can start answering the questions that truly matter for your positions:

- Directional Risk: If the stock moves $1, how much will my option's value change? That's Delta.

- Rate of Change: How fast will my directional risk change as the stock moves? That's Gamma.

- Time Decay: How much money am I losing every single day just because the clock is ticking? That's Theta.

- Volatility Impact: How much will my option's price change if the market gets more fearful or more complacent? That's Vega.

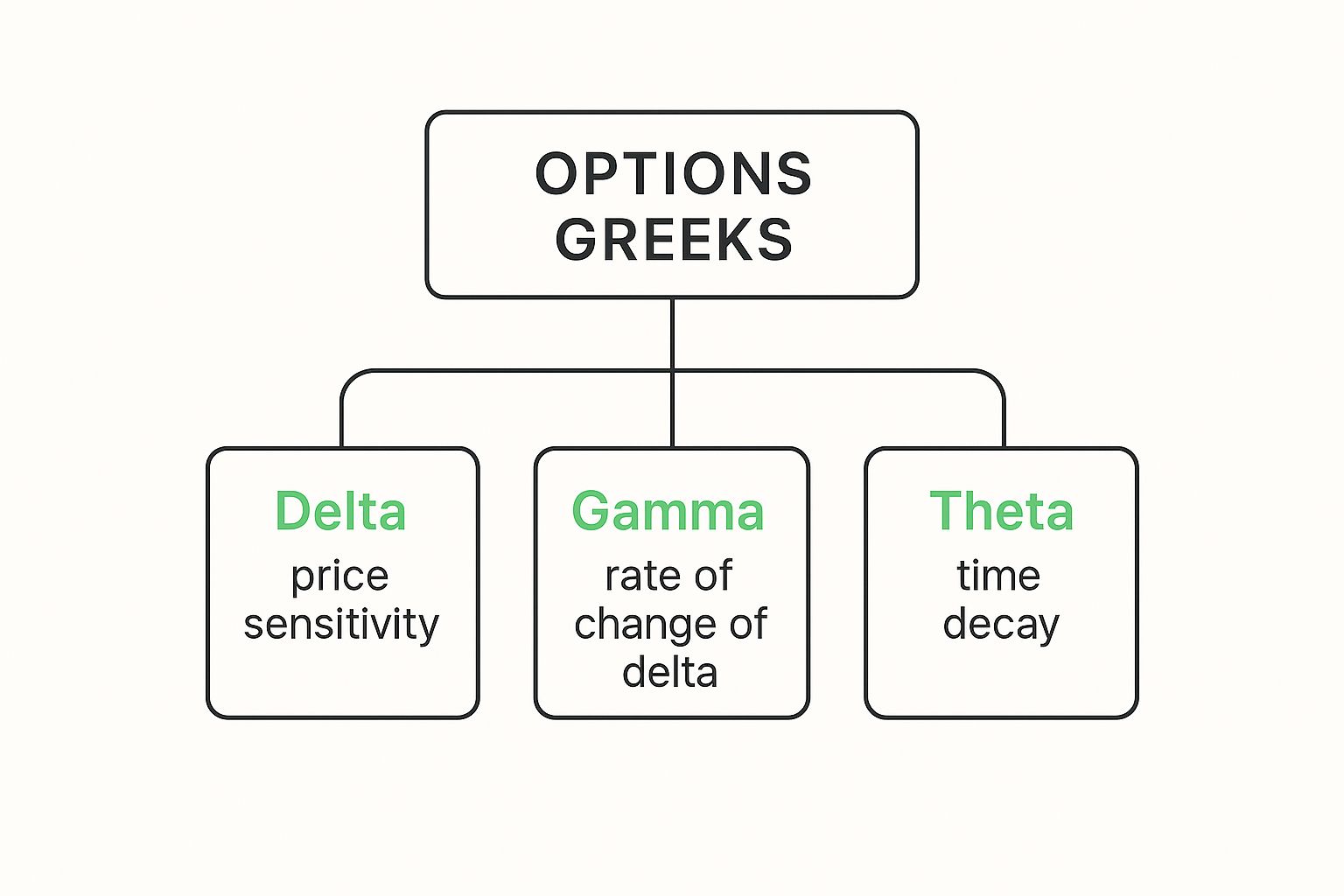

This diagram breaks down the hierarchy of the most important Greeks, showing how they measure price sensitivity, its rate of change, and the constant, nagging effect of time.

As you can see, Delta, Gamma, and Theta are the big three, driving most of an option's behavior as it relates to price and time. If you're looking to build a stronger foundation in options and other strategies, you can explore the trading fundamentals on our Academy page.

To keep things simple, here's a quick rundown of the main players you need to know.

Quick Overview of the Primary Options Greeks

This table gives you a high-level summary of the five main Greeks, what they measure, and why they matter to you as a trader.

| Greek | What It Measures | Key Takeaway for Traders |

|---|---|---|

| Delta | The rate of change in an option's price for every $1 move in the underlying stock. | Tells you how much your position will gain or lose based on the stock's direction. It's your primary measure of directional risk. |

| Gamma | The rate of change in Delta for every $1 move in the underlying stock. | Shows how quickly your directional risk (Delta) will accelerate. High Gamma means your position's value can change very fast. |

| Theta | The rate of change in an option's price for every one-day decrease in time to expiration. | This is the cost of time, or "time decay." As an option seller, Theta is your best friend; as a buyer, it's your enemy. |

| Vega | The rate of change in an option's price for every 1% change in implied volatility. | Measures sensitivity to market "fear" or uncertainty. Higher Vega means the option is more sensitive to changes in volatility. |

| Rho | The rate of change in an option's price for every 1% change in interest rates. | Generally has the smallest impact, especially on short-term options, but it's still good to know what it does. |

Getting comfortable with these concepts is like learning the rules of the road. Once you know them, you can navigate the markets with much more confidence and control, turning what was once a guessing game into a repeatable strategy.

Understanding Delta: The Compass for Your Trade

If you're going to master any of the options trading greeks, start with Delta. It's the most important one, hands down.

Think of it as the compass for your trade. It gives you an instant sense of direction and speed, answering the most critical question on any trader's mind: "If the stock moves, how much does my option's price change?"

Delta measures the expected change in an option's value for every $1 move in the underlying stock. It’s the bedrock for understanding your directional risk and the first step toward making smarter, more calculated trades.

How to Read Delta Values

Delta is a number that ranges from 0.0 to 1.0 for call options and 0.0 to -1.0 for put options. The sign (+ or -) just tells you if the option moves with the stock (calls) or against it (puts). Simple as that.

Here’s what those numbers mean in the real world:

- Call Options (Positive Delta): A call with a Delta of 0.70 should gain about $0.70 in value for every $1 the stock price goes up. On the flip side, it would lose roughly $0.70 if the stock drops by $1.

- Put Options (Negative Delta): A put with a Delta of -0.40 should gain about $0.40 in value for every $1 the stock price drops. It would lose that same $0.40 if the stock rallies by $1.

Key Takeaway: The closer Delta is to 1.0 (for calls) or -1.0 (for puts), the more your option acts like the stock itself. A lower Delta means it’s less sensitive to the stock’s price swings.

Let's say you're looking at a call option for SPY, which is trading at $450. You spot an option with a 0.70 Delta. If SPY climbs to $451, you can expect your option premium to increase by about $0.70. Since one contract controls 100 shares, your position’s value would jump by $70 ($0.70 x 100). That immediate feedback is why Delta is king.

For a deeper dive, check out our complete guide on what Delta is in options trading.

Delta as a Probability Gauge

Here's the cool part. Delta isn't just about price sensitivity. Experienced traders use it as a quick-and-dirty estimate for an option's probability of expiring in-the-money (ITM). It’s not a perfect science, but it’s a surprisingly accurate shortcut.

An option with a 0.30 Delta has roughly a 30% chance of finishing ITM. A 0.80 Delta implies an 80% chance.

This dual purpose makes Delta incredibly powerful. It tells you your directional risk and helps you quickly size up a trade's odds of success.

The Dynamic Nature of Delta

Delta isn't a "set it and forget it" number. It's constantly changing as the stock price moves and time ticks away toward expiration. This is where its relationship with the other Greeks, especially Gamma, kicks in.

Here’s a simple breakdown of how it behaves:

- Deep Out-of-the-Money (OTM): These options have Deltas near 0. They barely flinch when the stock moves because the market gives them almost no chance of becoming profitable.

- At-the-Money (ATM): These options have Deltas right around 0.50 (or -0.50 for puts). They’re sitting on a 50/50 probability and are extremely sensitive to the stock’s next move.

- Deep In-the-Money (ITM): These options have Deltas that creep toward 1.0 (or -1.0 for puts). They start moving almost dollar-for-dollar with the stock.

Imagine a stock rallies hard. A call option that was once OTM might become ATM, causing its Delta to climb from near zero to around 0.50. If the rally continues, that same option can become deep ITM, with its Delta pushing toward 1.0. Understanding this constant motion is at the very core of options trading.

Mastering Gamma: The Accelerator of Your Position

If Delta is your option's speedometer, Gamma is the gas pedal. It tells you how fast that speedometer’s needle is going to move. In the world of options trading greeks, Gamma measures the rate of change of Delta itself.

Simply put, Gamma answers the question: "If the stock moves up $1, how much will my Delta change?" This makes it the accelerator for your entire position. A high Gamma means your Delta can swing wildly with even small moves in the stock, turning a slow trade into a high-speed vehicle almost instantly.

Understanding this acceleration is critical. It’s why an option’s risk can shift so quickly, especially as it nears its strike price and expiration date.

Why Gamma Is a Double-Edged Sword

High-gamma options are where the real action is, but they can be dangerous. They offer explosive potential for gains but carry just as much risk for devastating losses. Why? Because a high Gamma amplifies everything.

When the trade goes your way, your Delta ramps up, and your profits accelerate. But if the stock moves against you, your Delta collapses just as quickly, and losses can pile up with shocking speed. This is what traders call "Gamma risk."

If you're selling options—like writing covered calls—you're especially sensitive to this. A sudden rally in the stock can cause the Delta on your short call to skyrocket, quickly erasing your premium and putting your shares at risk.

Key Takeaway: Gamma is at its absolute peak for at-the-money (ATM) options that are close to expiration. These options live on a knife's edge, with a Delta that's ready to jump in either direction at a moment's notice.

This means you have to stay vigilant. A position that looked perfectly safe yesterday can become wildly directional in a matter of hours if you aren't watching Gamma.

Gamma in Action: A Tale of Two Options

Let's make this real. Imagine a stock is trading at $100, and we're looking at two different call options.

Option A: At-the-Money (ATM) Call

- Strike Price: $100

- Delta: 0.50

- Gamma: 0.15

Option B: Deep Out-of-the-Money (OTM) Call

- Strike Price: $120

- Delta: 0.05

- Gamma: 0.01

Now, watch what happens when the stock rallies by $2 to $102.

For Option A (the ATM one), its high Gamma of 0.15 kicks in hard. For each dollar the stock moves, its Delta increases by 0.15. So, after a $2 move, the new Delta is roughly 0.80 (0.50 + 2 * 0.15). The option’s sensitivity just accelerated dramatically. It's now behaving much more like the stock itself.

But for Option B (the OTM one), its tiny Gamma of 0.01 barely makes a difference. After that same $2 rally, its new Delta is only about 0.07 (0.05 + 2 * 0.01). The position is still a long shot, with almost no change in its directional risk.

This contrast shows exactly why ATM options are so dynamic. Their high Gamma is what allows them to transform from a 50/50 bet into a position that mirrors the stock's every move. Understanding this relationship between Delta and Gamma is a core concept for anyone serious about options trading greeks and is key to managing those high-risk, high-reward situations.

Navigating Theta and Vega: The Unseen Forces of Time and Fear

While Delta and Gamma are all about which way a stock is headed, two other members of the options Greeks family are working behind the scenes. They influence your trade's value in ways that are less obvious but just as powerful.

Meet Theta and Vega—the forces that represent the constant pressures of time and fear.

Theta: The Melting Ice Cube

Think of Theta as a melting ice cube. Every single day, a tiny piece of your option's value disappears, dripping away like water. This is time decay, a relentless force that works against option buyers and for option sellers.

Theta tells you exactly how much value your option is set to lose each day, assuming the stock price and volatility don't change.

A Theta of -0.05 means your option's premium will drop by $0.05 every day. For a standard 100-share contract, that's a $5 loss each day just from the clock ticking. But if you're the one who sold that option? That $5 is daily income flowing into your pocket.

The Inescapable March of Time Decay

Time decay isn't a slow, steady drip. It accelerates. An option with 90 days left on the clock loses value very slowly. But as you get closer to expiration—especially in the last 30 days—the decay speeds up dramatically. The ice cube starts melting much, much faster.

This is exactly why selling short-term options, like weekly covered calls, is such a popular income strategy. Sellers are trying to capture that accelerated decay. On the flip side, buyers of short-term options are in a frantic race against time, needing a big price move to outrun the daily value erosion from Theta.

Key Takeaway: For option sellers, Theta is your best friend. For option buyers, it is your greatest enemy. Understanding its impact is non-negotiable for success.

Data backs this up. Empirical analysis from firms like OptionMetrics.com shows that Theta for short-dated equity options often averages around -0.05 per day. A typical option can see its value get chipped away daily as expiration looms.

Vega: The Fear Gauge

If Theta is the slow, steady march of time, Vega is the wild card—the market’s "fear gauge."

Vega measures how sensitive your option's price is to changes in implied volatility (IV). Implied volatility is simply the market's best guess of how much a stock will swing around in the future. When uncertainty spikes, IV goes up, and so do option prices.

Vega tells you precisely how much your option’s premium will change for every 1% shift in IV. For example, if an option has a Vega of 0.10, its price will jump by $0.10 if IV rises by 1%. For a full contract, that’s a $10 gain—even if the stock itself doesn't move an inch.

This is a huge deal. Major market events—earnings reports, Fed announcements, or geopolitical news—can send IV through the roof. This inflates option premiums, which is great for anyone holding options. But once the event passes, that uncertainty vanishes, IV collapses (an effect known as "volatility crush"), and option premiums plummet, which is exactly what sellers want to see.

Want to go deeper on this? Check out our guide on how to calculate implied volatility.

Impact of Theta and Vega on Option Strategies

So, how do these two forces affect your actual trades? Whether you're buying or selling, Theta and Vega are in a constant tug-of-war, pulling your profits in different directions. Understanding this dynamic is key to picking the right strategy.

Here's a quick comparison of how they impact common option strategies.

| Factor | Impact on Buying Options (e.g., Long Call) | Impact on Selling Options (e.g., Covered Call) |

|---|---|---|

| Time (Theta) | Negative (-). Time decay is a constant headwind, eroding your option's value every day. You are "paying" for time. | Positive (+). Time decay works in your favor, as the option you sold loses value, bringing you closer to keeping the full premium. |

| Rising IV (Vega) | Positive (+). An increase in implied volatility will inflate your option's premium, increasing its value. | Negative (-). A spike in implied volatility increases the value of the option you sold, which works against your position. |

| Falling IV (Vega) | Negative (-). A drop in implied volatility (volatility crush) will deflate your option's premium, hurting your position. | Positive (+). A collapse in implied volatility reduces the value of the option you sold, which is your goal as a seller. |

Ultimately, great options trading is about more than just predicting where a stock will go. It's about managing these non-directional risks. By mastering the dynamics of Theta and Vega, you can position yourself to profit not just from price moves, but from the simple passage of time and the market's ever-changing mood.

Putting the Greeks into Practice with Real Trades

Okay, so we’ve broken down what each Greek means. But knowing the definitions is one thing—seeing how they work in a live trade is where it all clicks. The Greeks aren't just abstract numbers on your screen; they tell a story about an option's risk and its potential reward.

Let's walk through how to read that story using two of the most popular income strategies out there: the covered call and the cash-secured put.

Think of it this way: with over 40 million option contracts trading hands on an average day, the Greeks are your navigation system. A typical at-the-money SPY call might have a Delta of 0.50, Gamma of 0.07, Theta of -0.04, and Vega of 0.12. These aren't just random stats; they are the precise metrics you need to manage your position and make smarter decisions.

The Covered Call: A Strategic Balancing Act

Imagine you own 100 shares of Apple (AAPL), and it's currently trading around $195. You want to generate a little extra income by selling a covered call, but which strike price do you choose? This is where you lean on the Greeks to frame your decision.

Let's look at a hypothetical options chain for AAPL with about 30 days left until expiration. To get the most out of this, you'll want to be comfortable looking at an options chain. If you need a refresher, check out our guide on how to read option chains.

Scenario A: The Conservative Play ($205 Strike)

- Delta: 0.20 (Roughly a 20% chance your shares get called away)

- Theta: -0.04 (You collect $4 per day as time passes)

- Premium: $1.50 (That's $150 in your pocket per contract)

This is your classic low-risk, lower-reward move. The low Delta tells you it's pretty unlikely your shares will be assigned, meaning you'll almost certainly keep your stock and the premium. The trade-off? A smaller paycheck.

Scenario B: The Aggressive Play ($195 At-the-Money Strike)

- Delta: 0.50 (A true 50/50 shot at assignment)

- Theta: -0.07 (You're collecting $7 per day now)

- Premium: $4.50 (A much healthier $450 per contract)

Here, you're grabbing a much bigger premium and benefiting from faster time decay (that higher Theta). But with a 50% probability of assignment, you have to be totally okay with selling your shares at $195. This is a pure income play.

Key Insight: For covered calls, Delta is your probability gauge. Theta is your income engine. Your choice comes down to what you care about more: keeping your shares or maximizing the cash you collect.

With a tool like Strike Price, you see these probabilities directly, without needing to translate Delta in your head. It helps you find that sweet spot between safety and yield.

The Cash-Secured Put: Using Greeks to Buy Stocks on Your Terms

Now, let's flip the script. You want to buy 100 shares of AAPL, but you think $195 is a little steep. You’d be a happy buyer down at $185. A cash-secured put lets you get paid while you wait for your price.

You sell a put option with an $185 strike price, collecting a premium for making a promise: you'll buy the shares if the price falls to that level.

- Strike Price: $185

- Delta: -0.25 (About a 25% chance the stock drops below $185 and you have to buy)

- Theta: -0.05 (You earn $5 every day as the option's value decays)

- Premium: $2.00 ($200 per contract)

So, what are the Greeks telling you here?

- Probability of Assignment (Delta): The -0.25 Delta signals a low probability that you'll actually end up buying the shares. The market is paying you to take on a risk it doesn't think will happen.

- Time is Your Ally (Theta): Every single day that AAPL stays above $185, Theta works for you, chipping away at the option's value. If the contract expires worthless, you just keep the $200 premium, no strings attached.

This strategy is a perfect example of how the options trading Greeks help you measure your risk. You're not just guessing—you're making a decision backed by data. You know your odds of assignment and exactly how much you're getting paid each day for taking that risk. By looking at the Greeks, you turn a complex financial product into a clear trade with a defined game plan.

Got Questions About Options Greeks?

Once you get the basics of the options trading greeks down, you'll naturally start wondering how it all works in the real world. Let's tackle some of the most common questions that pop up.

Which Greek Should a Beginner Learn First?

If you’re new to options, your starting point is Delta. No question. It’s the single most important Greek to master first because it answers the most immediate question you’ll have: "What happens to my option's price if the stock moves?"

Delta gives you a quick read on your directional risk. But it also does double duty as a rough-and-ready estimate of the probability that your option will finish in-the-money. That dual role is why it's the foundation for nearly every basic options strategy.

Once you’re comfortable with Delta, turn your attention to Theta. As an option seller, Theta is your best friend—it's the time decay you collect day after day. For income strategies like covered calls and secured puts, understanding Theta is non-negotiable.

How Do I Find the Greeks for an Option?

Good news: you don’t need a fancy calculator or a degree in mathematics. Every modern brokerage platform I’ve seen shows the options greeks right in the option chain, listed next to the bid and ask prices.

When you pull up a stock, you’ll see columns for Delta, Gamma, Theta, and Vega. They're designed to be real-time tools for traders like us.

- Can't see them? Check your platform’s settings. You can usually customize the columns in your option chain to make sure all the Greeks are visible.

- No math required. The broker does all the heavy lifting, constantly updating these values as the market changes.

Can an Option Have High Theta and High Vega?

Absolutely. In fact, it happens all the time and sets up a classic trade-off for option sellers. You'll typically see this in options with about 30 to 60 days left until they expire, especially right before a big event like an earnings report.

The uncertainty around the event pumps up implied volatility, which means Vega is high. The option's price is extremely sensitive to shifts in market sentiment.

At the same time, the contract is in that sweet spot for time decay, so its Theta is also high. If you sell an option in this scenario, you're making a very specific bet.

The Trader's Bet: You're betting that after the event, all that uncertainty will evaporate, causing a "volatility crush" that deflates the option's value (thanks, Vega!). At the same time, you're collecting that accelerated time decay (Theta). The catch? You're exposed to a potentially massive price swing from the event itself.

Why Do My Option's Greeks Keep Changing?

The options trading greeks are anything but static. They are constantly shifting in response to market movements. Think of them as living numbers. Here are the three main drivers:

- The Stock Price Moves: As the stock price changes, your option gets closer to or further from its strike price. This directly impacts Delta and Gamma. An out-of-the-money option's Delta will grow as the stock moves toward its strike.

- Time Passes: Every day that goes by, Theta does its work. As you get closer to expiration, the rate of time decay speeds up, and Gamma for at-the-money options tends to spike.

- Implied Volatility (IV) Changes: Market fear isn't constant. A sudden jump in IV will boost Vega, making all options more expensive. A drop in IV will do the opposite.

The key takeaway is that your position’s risk profile isn't locked in when you place the trade. It evolves with the market, which is why you always have to keep an eye on it.

Ready to stop guessing and start making data-driven decisions? Strike Price gives you the real-time probability data you need to sell covered calls and secured puts with confidence. Our platform shows you the precise odds of assignment for every strike, helping you balance safety and premium to meet your income goals.

Discover how Strike Price can transform your trading strategy today.