Short a Put An Income Strategy for Options Traders

If a stock moves past your strike, the option can be assigned — meaning you'll have to sell (in a call) or buy (in a put). Knowing the assignment probability ahead of time is key to managing risk.

Posted by

Related reading

A Step-by-Step Covered Calls Example for Consistent Income

Unlock consistent income with our step-by-step covered calls example. This guide breaks down the strategy, risks, and outcomes to help you trade confidently.

Long Call and Short Put The Ultimate Synthetic Stock Guide

Unlock the power of the long call and short put strategy. This guide explains how synthetic long stock works, its benefits, risks, and how to execute it.

What is a Call Spread? A Clear Guide to Bull and Bear Spreads

What is a call spread? Discover how bull and bear spreads limit risk and sharpen your options trading strategy.

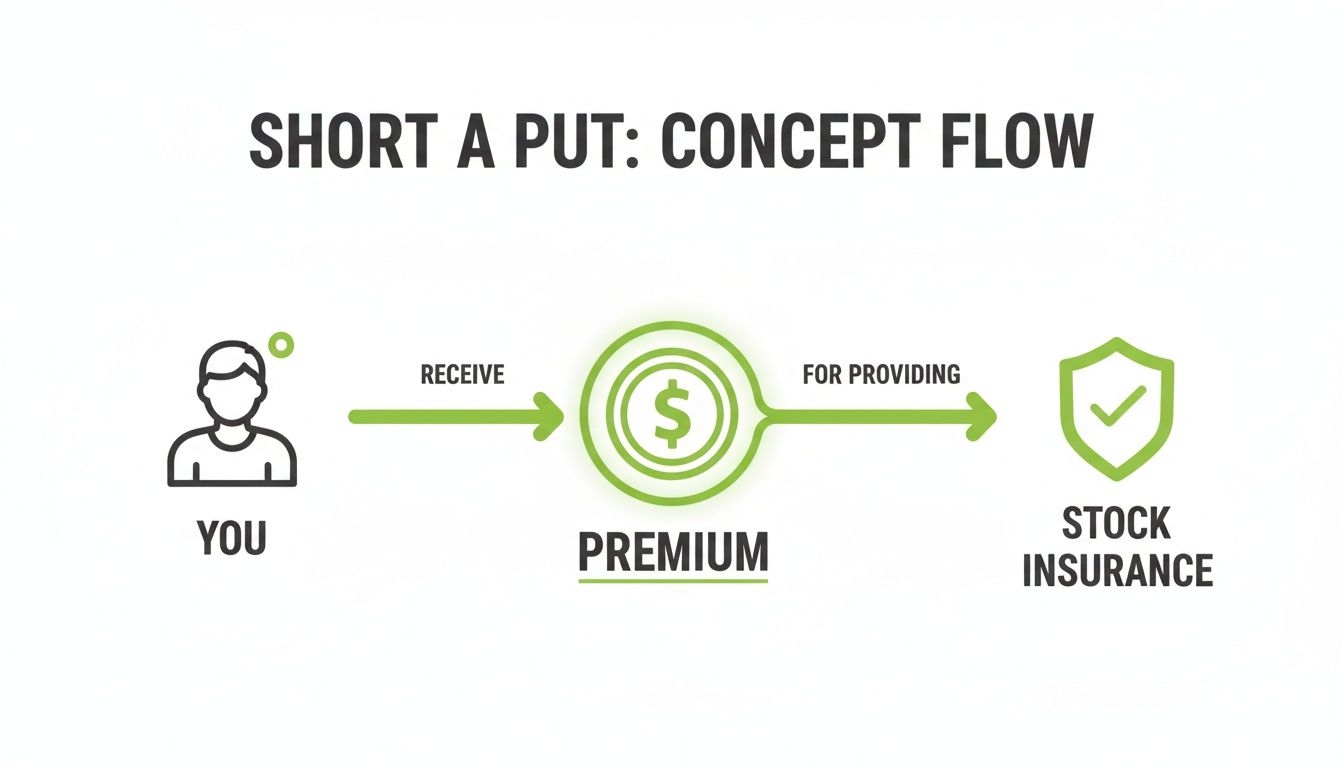

When you short a put, you’re essentially selling an insurance policy on a stock. You agree to buy shares at a specific price (the strike price) if the stock drops to that level by a certain date. In return for taking on that obligation, you get paid an upfront fee called a premium.

That premium is yours to keep, no matter what. That’s the core appeal of the strategy and why it’s a favorite for so many income-focused traders.

The Core Concept of Selling a Put

Think of yourself as an insurance company, but for stocks. Another investor is worried their stock might fall, so they pay you that premium for a policy. The policy gives them the right to sell their stock to you at a pre-determined price if it drops.

If the stock stays above that price, the policy expires, and you just keep the cash. You were paid for your willingness to buy a stock at a price you already liked.

Your Dual Objectives

Selling a put isn't just about collecting a single payment; it’s a strategy with two powerful goals. Getting this right is the key to using it effectively.

- Generating Consistent Income: The most obvious goal is pocketing premiums. By repeatedly selling puts on stocks you think will hold steady or rise, you can create a reliable stream of cash flow. Many traders treat this like collecting monthly rent on a property they don’t even have to own yet.

- Acquiring Stocks at a Discount: The other objective is to buy stocks you already want, but cheaper. If you like a company, you can sell a put with a strike price below where it's currently trading. If the stock drops and you get assigned, you end up buying the shares you wanted anyway—but at a discount to the price it was when you opened the trade.

Framed this way, you can create a win-win scenario for yourself. Either you pocket the premium as pure profit, or you get to buy a great stock at a price you were happy with from the start.

The Mindset of a Put Seller

Adopting the right mindset is absolutely crucial here. A put seller isn’t a speculator gambling on a huge price jump. You’re acting more like a business owner, carefully weighing risk to earn a predictable return.

You’re betting that a stock will not go down significantly. That’s a fundamentally different game than betting it will go up. This position makes time your best friend. Every single day that goes by, the "insurance policy" you sold loses a tiny bit of its value—a phenomenon called time decay. This decay works in your favor, pulling you closer to realizing your maximum profit: the premium you collected on day one.

The Mechanics of a Short Put Trade

To really get how a short put works, we need to pop the hood and look at the moving parts. Every options trade has a lifecycle, defined by a few key pieces and driven by forces already at play in the market. Knowing these elements is what separates a blind guess from a smart, strategic decision.

At its heart, selling a put is a simple agreement with three parts:

- The Underlying Stock: The company you’re focused on, like Apple or Ford.

- The Strike Price: The price where you agree to buy the stock if it drops.

- The Expiration Date: The day your obligation officially ends.

The moment you sell the put, you collect a cash premium. From that point on, the value of that option will bounce around until its expiration date. Your goal is for its value to shrink, ideally all the way to zero. The good news? Two powerful forces are already working in your favor to make that happen.

Time Decay: Your Greatest Ally

The first and most reliable force is time decay, which traders call theta. Think of an option's value like a block of ice melting in the sun—it naturally shrinks a little bit every single day. The "insurance policy" you sold simply becomes less valuable as there’s less time for the stock to make a big, unexpected move against you.

This steady, predictable erosion of value is the main engine of profit for an options seller. You are literally being paid to wait. In fact, an analysis of over 10,000 stocks showed that 72% of short puts sold at a standard probability level (16-delta) expired worthless between 2010 and 2020. This incredible success rate is largely thanks to theta decay, which chips away at an option's value daily. You can find more research on options pricing at OptionMetrics.

This infographic shows the simple exchange: you receive a premium for offering what is essentially stock insurance.

It’s a direct trade-off. You accept a potential obligation and are immediately paid in cash for taking on that risk.

The Impact of Volatility

The second force is implied volatility (IV), also known by its Greek name, vega. Implied volatility is just a fancy way of saying how much the market thinks a stock price will swing in the future. When uncertainty is high—like right before an earnings report or during major market news—IV spikes, and option premiums get much more expensive.

As a seller, high IV is your best friend. Selling puts when volatility is juiced up means you collect a much bigger premium for taking on the same level of risk. That higher starting credit gives you a bigger cushion against price drops and boosts your potential profit.

It's like selling flood insurance. You can charge a whole lot more during hurricane season than you can during a drought. Your goal is to be the insurer during the storm, collecting those inflated premiums when buyers are feeling the most anxious.

The Three Possible Trade Outcomes

Once you sell a put, the trade can only end in one of three ways. A disciplined trader has a clear plan for every single one.

- Outcome 1: The Option Expires Worthless. This is the best-case scenario. The stock price finishes above your strike price on expiration day. The put option is now worth zero, and you keep 100% of the premium you collected as pure profit. Your obligation is gone.

- Outcome 2: You Get Assigned the Stock. If the stock price is below your strike at expiration, you get "assigned." This means you have to make good on your promise and buy 100 shares of the stock at the strike price. This isn't necessarily a failure, especially if you sold a put on a company you wanted to own at that lower price anyway.

- Outcome 3: You Close the Position Early. You don't have to ride it out until the very end. Many traders choose to close their positions early to lock in a profit (like buying the put back after its value has dropped by 50%) or to cut their losses if the trade starts moving against them.

Understanding the Risk and Reward

Every trading strategy has a trade-off, and when you short a put, the equation is crystal clear. The "reward" side is simple and defined—your maximum possible profit is the premium you collect the moment you sell the option.

That premium is yours to keep, no matter what happens next. If you sell a put for a $200 credit, the absolute most you can ever make from that single trade is $200. This happens if the stock price stays above your strike price and the option expires worthless. Simple enough.

The "risk" side of the equation, however, is where your attention needs to be. While the reward is capped, the potential for loss is significant if you don't manage it with discipline. This is why understanding your total exposure is non-negotiable before you ever click the "trade" button.

Cash Secured Puts vs Naked Puts

The most critical distinction in managing this risk comes down to one thing: how you back up the trade. There are two primary ways to short a put, and one is vastly safer for most of us.

When you're deciding how to structure your short put trade, you're really choosing between two very different risk profiles: one that’s measured and controlled, and another that’s, frankly, playing with fire. Here's a quick breakdown to make the choice obvious.

| Feature | Cash Secured Put | Naked Put |

|---|---|---|

| Capital Requirement | Cash equal to (Strike Price x 100) is reserved in your account. | No cash is reserved; relies on margin. |

| Maximum Risk | Defined: (Strike Price x 100) - Premium. | Potentially unlimited; catastrophic losses possible. |

| Best For | Retail investors, income-focused traders. | Institutional traders, hedge funds with large portfolios. |

| Worst-Case Scenario | You buy 100 shares of a stock you wanted at a discount. | Forced to buy shares on margin, leading to massive debt. |

| Brokerage Access | Widely available in standard brokerage accounts. | Requires highest-level options approval; not available to most. |

For individual investors, the path is clear: always use the cash-secured put strategy. This method turns the worst-case scenario from a financial disaster into a planned stock purchase at a price you already decided was a good deal.

Calculating Your Maximum Loss

When you short a put that is cash-secured, your maximum loss isn't infinite. It's substantial, for sure, but it is defined. The absolute worst that can happen is the company goes bankrupt and the stock price drops to $0.

In that situation, you’d still be obligated to buy 100 shares at your strike price. Your maximum loss is calculated like this: (Strike Price x 100) - Premium Received. You get to subtract the premium because that initial credit helps offset a small part of your loss.

A Practical Example of Risk and Reward

Let's put this into a real-world context to see how the numbers play out.

Imagine XYZ Corp is currently trading at $105 per share. You're bullish on the company but feel the price is a bit high. You decide to short a put with a strike price of $100 that expires in 30 days, and you collect a premium of $3.00 per share, or $300 total.

Here’s how the risk-reward profile breaks down:

| Feature | Calculation | Amount |

|---|---|---|

| Capital Required | ($100 Strike Price x 100 Shares) | $10,000 |

| Maximum Profit | ($3.00 Premium x 100 Shares) | $300 |

| Maximum Loss | ($10,000 Capital) - ($300 Premium) | $9,700 |

| Breakeven Price | ($100 Strike Price) - ($3.00 Premium) | $97.00 |

Your breakeven price is the point where you neither make nor lose money on the trade. As long as XYZ stock closes above $97 at expiration, your trade is profitable. Understanding the probability of profit in options trading is a key skill that helps you pick trades with a higher likelihood of success. This defined risk profile is what empowers you to make informed decisions, ensuring you never take on more risk than you're comfortable with.

How to Select the Right Put to Short

Knowing the theory is one thing, but putting it into action is where real trading begins. To consistently generate income by shorting puts, you need a repeatable process for spotting the right opportunities. It's more than just picking a stock you like; it’s about using data to stack the odds in your favor.

Three core metrics will guide your search: Delta, Implied Volatility (IV), and the option's expiration date. Once you get a feel for these three levers, you can systematically find trades that fit your income goals and risk tolerance.

Target a Low Delta for a Higher Probability of Success

The first metric to check is Delta. Think of it as a quick cheat sheet for an option's probability of expiring in-the-money. A Delta of 0.30 roughly translates to a 30% chance the stock will close below that strike price by expiration.

Since we’re playing for income, we want the odds on our side. That’s why many traders focus on selling puts with a Delta of 0.30 or lower. This simple filter instantly narrows your search to trades with a high statistical chance of expiring worthless, letting you pocket the premium.

By choosing a lower Delta, you are intentionally picking a strike price that’s further away from where the stock is trading right now. This builds a bigger "cushion" into your trade, giving the stock more room to fall before your position is at risk of assignment.

This approach is all about consistency. A smaller, high-probability premium collected over and over is often a much more sustainable strategy than chasing bigger, riskier payouts.

Sell Into High Implied Volatility

The second key ingredient is Implied Volatility (IV). Remember, high IV means option premiums are pumped up because of market fear or uncertainty. As a put seller, that’s exactly what you want to see.

Selling puts when IV is high is like selling umbrellas in a rainstorm—you get to charge a much higher price. This inflated premium does two great things for your trade:

- It boosts your potential return. You collect more cash upfront for the same amount of capital you have to secure.

- It widens your breakeven point. A bigger premium pushes your breakeven price even lower, giving you an even larger buffer if the stock price drops.

The goal is to be the seller when everyone else is an anxious buyer. Tools can help you spot when a stock's current IV is high compared to its own history, signaling a great time to sell. This is where you find a real statistical edge.

Finding the Sweet Spot for Expiration

Finally, you have to pick the right timeframe. You could sell a put that expires next week or next year, but the sweet spot for balancing premium with risk is typically between 30 and 45 days to expiration (DTE).

This window is ideal because it’s where the rate of time decay, or theta, really starts to accelerate. Options in this range lose their value faster, which is perfect for you as the seller.

- Shorter than 30 days: Time decay is lightning-fast, but the premiums are smaller, and a sharp move against you leaves almost no time to react.

- Longer than 45 days: You collect a bigger premium, but your cash is tied up for longer, and the trade is exposed to more potential market surprises.

Sticking to the 30-45 DTE range gives you the best of both worlds: meaningful premiums and the full benefit of accelerating time decay. Historical data shows just how powerful this methodical approach is. From 2015-2025, SPX short puts at 20-delta strikes returned 12.4% annualized on capital, largely because sellers consistently captured the edge between implied and realized volatility. You can dig into the full SPX options historical data analysis at MarketXLS to see these trends for yourself.

Platforms like Strike Price are built to help you find these opportunities in seconds. Its Target Mode, for example, lets you set your desired safety level (like an 80% chance of success) and income goals. The app then scans the market to find trades that match your exact criteria. You can use our guide on the cash-secured put calculator to see how these returns are calculated. This turns a complex analysis into a simple, actionable workflow.

Managing Your Trades and Planning Your Exit

Nailing your entry is only half the battle. What truly separates consistent options sellers from gamblers is a disciplined plan for managing the trade and knowing exactly when to get out.

Once you’ve shorted a put, the real work begins. Having a clear set of rules takes the emotion out of the equation, letting you act decisively whether the trade is a winner or a loser. Your plan needs to cover taking profits, cutting losses, and knowing when to adjust your position.

When to Take Your Profits

It’s tempting to hold a winning trade until the very end to squeeze out 100% of the premium. But that’s a rookie mistake. As the option gets closer to expiring, you’re holding onto all the risk for just a few extra dollars of profit. The final gains are the hardest to earn, yet you're still completely exposed to a sudden market dive.

A much smarter approach is to set a profit target and close the trade early.

- The 50% Rule: Many seasoned traders live by this. Once you’ve captured 50% of the premium you collected, you close the trade. If you sold a put for a $200 credit, you’d set an order to buy it back for $100. Simple.

- Why It Works: This gets your capital back in your hands faster, so you can redeploy it into new trades and compound your returns. It also dramatically cuts down the time you're exposed to risk, which is a huge factor in boosting your overall win rate.

Think of it like harvesting a crop when it’s ripe instead of waiting until the last possible second. By banking your profits, you turn a paper gain into real cash.

Defensive Tactics When a Trade Goes Against You

Look, not every trade is going to work out. Knowing how to react when a stock moves against you is what keeps you in the game. The goal isn’t to avoid losses—it's to manage them intelligently. One of the best defensive moves in your playbook is rolling the position.

Rolling is a two-part move you execute in a single order:

- Close the current option: You buy back the short put that’s now in the red.

- Open a new one: At the same time, you sell another put on the same stock, but with a later expiration date.

This simple maneuver gives your trade more time to become profitable. Even better, you can often collect an additional credit in the process, which lowers your breakeven price and gives you a better chance of turning a loser into a winner. We have a full guide that breaks down exactly how to master rolling over options.

Setting a Hard Stop Loss

Sometimes a stock moves too far, too fast, and rolling just isn't a viable option. In these situations, you need a pre-planned exit ramp to cut your losses and live to trade another day. "Hoping" a trade will come back is a recipe for disaster.

A disciplined exit strategy is just as important for losing trades as it is for winners. A small, managed loss is always better than a catastrophic one that wipes out weeks of gains.

A common rule of thumb is to close the position if the loss hits a certain multiple of the premium you received, like 2x or 3x. A massive backtest of over 41,600 short put trades showed that smart management rules—like closing at a -300% loss relative to the premium—delivered far better risk-adjusted returns than just holding to expiration. This one rule capped the worst-case drawdowns at just -$561, a nearly fourfold improvement.

And finally, don't forget that if the stock drops below your strike and you still like the company long-term, getting assigned is a perfectly valid outcome. You simply buy the shares at the discounted price you agreed to, which might have been your goal all along.

Your Top Questions About Shorting Puts

As you get into selling options, a few questions pop up time and time again. Getting these sorted out is the fastest way to build the confidence you need to trade well. Let's tackle them head-on.

Think of this as your go-to reference for the real-world situations you’ll run into when shorting a put.

What Happens If I Get Assigned on a Short Put?

First off, getting assigned isn’t a failure—it’s one of the planned outcomes. When you’re assigned, you’re simply holding up your end of the bargain. You agreed to buy 100 shares of the stock at the strike price, and now you’re doing it.

If you sold a cash-secured put, the process is dead simple. The cash you set aside is automatically used to buy the shares. No scrambling for funds, no surprises. The money was already waiting.

Once those shares land in your account, you're officially a stockholder. This opens up a whole new way to generate income. Many traders who get assigned immediately turn around and start selling covered calls against their new stock. This one-two punch of shorting puts and selling calls is known as "the wheel," a popular strategy for continuously generating premiums. The golden rule here is simple: only sell puts on high-quality companies you'd be happy to own at your chosen strike price.

Is Shorting a Put a Bullish or Bearish Strategy?

Shorting a put is a neutral to bullish strategy. At its core, you're betting that the stock's price will not drop significantly. Your trade makes money in three different scenarios:

- The stock price goes up.

- The stock price moves sideways.

- The stock price dips a little but stays above your breakeven point.

This flexibility is what makes it so powerful. It's a great move when you're feeling pretty good about a stock but aren't necessarily expecting a massive rally. If you were extremely bullish, buying a call option would offer more explosive upside. But when you short a put, that premium you collect acts as a buffer, giving you a cushion against small price drops and more ways to win the trade.

How Do I Calculate My Return on a Short Put?

Knowing your return is how you decide if a trade is worth the risk. The key here is that your return on investment (ROI) is based on the actual capital required to secure the trade, not the full cost of the shares.

The formula is straightforward: (Premium Received ÷ Capital Secured) × 100.

For a cash-secured put, the capital your broker holds is calculated like this: (Strike Price × 100) – (Premium Received × 100). The premium you pocketed upfront slightly reduces the cash you have to tie up.

Let's walk through an example:

- You sell a put with a $50 strike price.

- You collect a $2.00 premium per share (that's $200 in your pocket).

- Your capital secured is ($50 × 100) - ($2 × 100) = $4,800.

Now, let's find your return: ($200 ÷ $4,800) × 100 = 4.17%.

That 4.17% is your potential return over the life of the option, which is often just 30-45 days. When you start to annualize that figure, you really see the income-generating power of selling short-term options contracts.

Can I Lose More Than the Premium I Collect?

Yes, absolutely. This is the single most important risk to understand before you place a single trade. While your maximum profit is capped at the premium you collect, your potential loss is substantial.

Your profit is defined, but your risk is not. The worst-case scenario for a cash-secured put is if the company goes bankrupt and the stock price craters to zero. You would still be on the hook to buy 100 shares at your strike price, even if they're now completely worthless.

Your maximum loss would be the strike price multiplied by 100, minus the small premium you collected. For a $50 strike put, that's nearly $5,000 on the line. This is exactly why it's critical to follow two simple rules:

- Only sell puts on fundamentally strong companies you believe in for the long haul.

- Always use a cash-secured approach so you know you can comfortably cover the purchase if you get assigned.

This discipline is what separates strategic income generation from reckless gambling. Respect the risk, and you can harness the power of shorting puts to hit your financial goals.

Ready to turn these strategies into action? Strike Price provides real-time probability metrics and smart alerts to help you find the safest and most profitable short put opportunities. Stop guessing and start making data-driven decisions by visiting https://strikeprice.app to see how our platform can help you consistently generate income.