Greeks Options Explained: greeks options explained for smarter income trading

If a stock moves past your strike, the option can be assigned — meaning you'll have to sell (in a call) or buy (in a put). Knowing the assignment probability ahead of time is key to managing risk.

Posted by

Related reading

Out of Money Call Options A Guide to Consistent Income

Learn how to use out of money call options to generate consistent income. This guide covers key strategies, risk management, and real-world examples.

How Options Are Priced A Practical Guide for Investors

Understand how options are priced with this clear guide. Learn about intrinsic value, implied volatility, and pricing models to improve your investing strategy.

Greek Options Explained for Income Traders

Unlock your options trading potential. This guide on greek options explained shows you how to use Delta, Gamma, and Theta to generate consistent income.

Options Greeks are, simply put, the vital signs of your options trade. They act like a car's dashboard, showing you how an option's price will likely react to changes in the underlying stock price (Delta), the steady march of time (Theta), and swings in market fear (Vega). They turn what can feel like a guessing game into a clear, data-driven process.

What Are Options Greeks and Why Do They Matter?

Think of the Greeks as the essential gauges on your options trading dashboard. Just like a car’s instruments show your speed, fuel level, and engine temperature, the Greeks reveal the hidden risks and opportunities inside every option contract.

This isn’t just theory for Wall Street pros; it’s fundamental for anyone serious about generating income through covered calls or cash-secured puts. The Greeks give you a clear advantage by putting a number on an option's sensitivity to the market forces that affect your bottom line.

From Greek Letters to Practical Tools

At first, the names—Delta, Gamma, Theta, Vega—might sound a bit intimidating. But they aren't abstract academic terms. They're practical tools that help you make more confident decisions by answering a few critical questions about your trade:

- How will my option's price change if the stock moves up or down?

- How much value will my option lose to time decay each day?

- How will a spike in market fear or uncertainty affect my position?

Answering these questions before you enter a trade is the cornerstone of successful, long-term options selling. At their core, the Greeks are really just a way of understanding market sensitivities in a very specific, practical way for options.

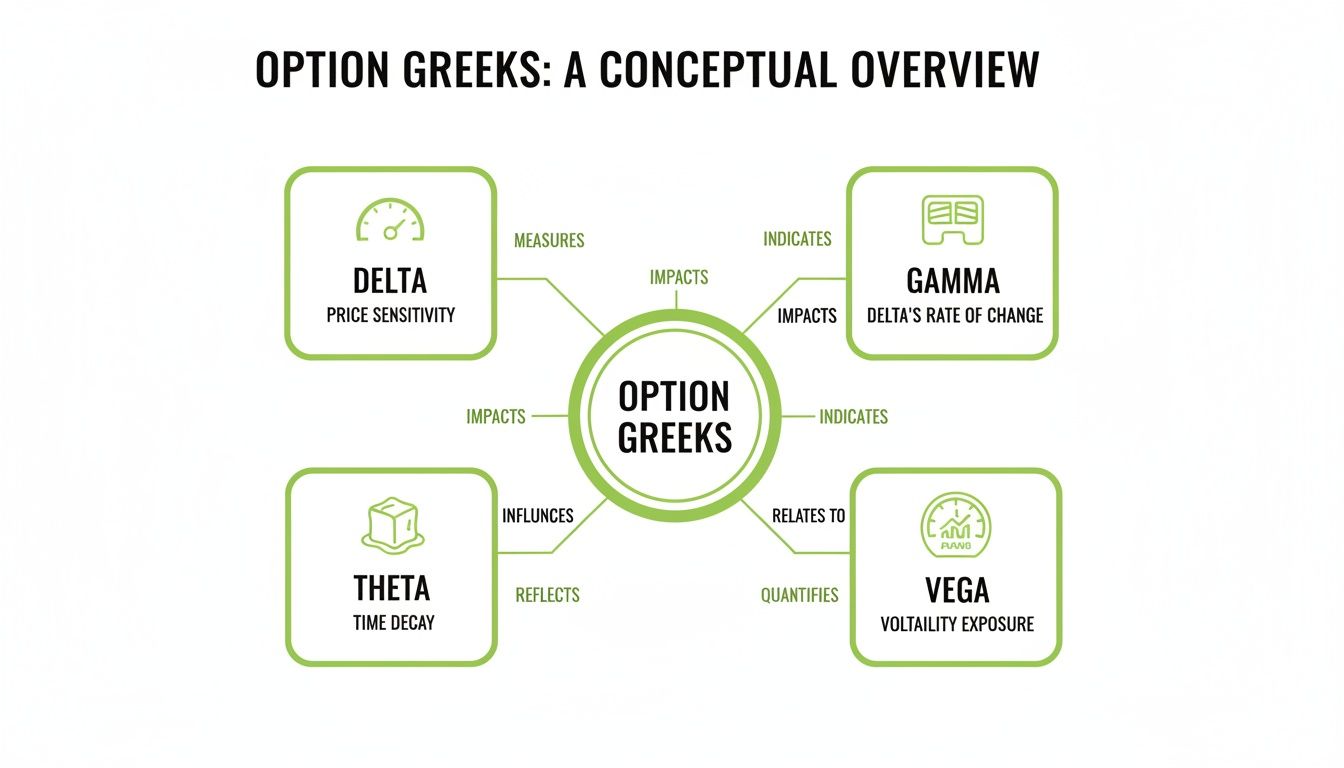

The Five Key Sensitivities

When options sellers talk about “the Greeks,” they’re usually focused on five key metrics. Each one describes how an option’s price reacts to a different market factor. For income-focused sellers, Delta is especially useful because it doubles as a rough probability of the option expiring in-the-money.

For instance, a call option with a Delta of 0.30 can be thought of as having about a 30% chance of finishing in-the-money. This also means you have a 70% probability that the option will expire worthless, allowing you to keep the entire premium you collected.

In essence, the Greeks turn a simple options premium into a multi-dimensional risk profile. They translate market variables into a quantifiable dashboard, enabling platforms like Strike Price to monitor your positions in real time and alert you to changing conditions.

Let’s quickly break down the main players.

The Core Options Greeks at a Glance

This table gives you a quick summary of the most important Greeks, what they measure, and why they matter so much to an option seller.

| Greek | What It Measures | Key Insight for Option Sellers |

|---|---|---|

| Delta | Change in option price per $1 move in the underlying stock. | Helps estimate the probability of expiring in-the-money. |

| Gamma | Rate of change of Delta. | Shows how quickly your directional risk (Delta) will accelerate as the stock price moves. |

| Theta | Change in option price per one-day passage of time. | Represents your daily "profit" from time decay, which is the primary goal for most sellers. |

| Vega | Change in option price per 1% change in implied volatility. | Measures your sensitivity to market fear or uncertainty. High vega can be good... until it isn't. |

Getting a feel for these four core Greeks is the first step toward managing your positions like a professional. They give you the data you need to stop guessing and start trading with a quantifiable edge.

Decoding the Four Most Important Greeks

While there are a ton of Greeks out there, you really only need to master four of them to make smart, probability-driven selling decisions. Think of them as the main gauges on your trading dashboard. Once you know what each one is telling you, you can turn a wall of abstract market data into a clear plan of action.

Let's walk through each one, using simple analogies to build a real, intuitive feel for how these numbers affect your trades every single day.

Delta: Your Speedometer and Probability Gauge

Delta (Δ) is, without a doubt, the most important Greek for an options seller. It pulls double duty. First, it’s like a speedometer, telling you how much an option's price should change for every $1 move in the underlying stock.

Let's say you sell a covered call on XYZ stock, which is trading at $100. The call has a Delta of 0.30. If XYZ rallies to $101, the price of your short call will go up by about $0.30—which is a loss for you. On the flip side, if the stock drops to $99, the option's value falls by $0.30, putting you that much closer to keeping the full premium.

But Delta has a second, incredibly useful trick up its sleeve for income traders. It doubles as a rough, real-time estimate of the probability that an option will expire in-the-money (ITM).

A Delta of 0.30 isn't just about price sensitivity; it also suggests there's roughly a 30% chance of the stock closing above your strike price by expiration. As a seller, that means you have a 70% probability of the option expiring worthless. That’s the goal.

This dual personality makes Delta the cornerstone of picking your strike prices.

Gamma: The Accelerator Pedal

If Delta is the speedometer, Gamma (Γ) is the accelerator. It measures how fast Delta itself changes. Put simply, Gamma tells you how quickly your speedometer is going to ramp up or down as the stock price moves.

Options that are at-the-money (ATM) and getting close to expiration have the highest Gamma. This is where the danger zone is for sellers. A small stock move can send Delta flying, turning a position that looked safe just a day ago into a high-risk gamble.

Imagine two call options, both with a 0.20 Delta:

- Option A: Has 90 days left and very low Gamma.

- Option B: Has 3 days left and sky-high Gamma.

If the stock pops $2, the Delta on Option A might inch up from 0.20 to 0.25. But for Option B, that same $2 move could launch its Delta from 0.20 to 0.60 or more. Your probability of getting assigned just exploded, and your entire risk profile changed in an instant. That’s Gamma risk in action, and you have to respect it if you want to avoid ugly surprises.

Theta: The Melting Ice Cube

Theta (Θ) is an option seller’s absolute best friend. It’s the engine of time decay, showing you how much extrinsic value an option is set to lose every single day, assuming the stock price and volatility don’t change.

I like to think of an option’s premium as a melting ice cube. Every day that passes, a little piece of it melts away, dripping profit straight into your account. This erosion is relentless, predictable, and it's the fundamental reason selling covered calls and cash-secured puts works for generating income.

Theta is always a negative number. A Theta of -0.05 means the option will lose about $5 (0.05 x 100 shares) in value each day, just from time passing. This decay isn't linear; it accelerates like crazy as expiration gets closer. An option with 30 days left might lose a few cents a day, but in its final week, it could be bleeding a dollar or more daily. You can learn more about harnessing the power of option time decay to really maximize this effect.

Vega: The Fear Gauge

Finally, there’s Vega (V), which measures how sensitive an option is to changes in implied volatility (IV). The easiest way to think about Vega is as the "fear gauge" for your option. When the market gets nervous or uncertain about a stock’s future, IV goes up, and so does the price of its options.

Vega tells you exactly how much an option's price will change for every 1% shift in IV. If your option has a Vega of 0.10, a 1% jump in implied volatility will add $10 (0.10 x 100 shares) to its premium.

For a seller, this is a double-edged sword.

- Selling into High IV: You want to sell options when the premium is as rich as possible. Selling when IV is high (meaning Vega's impact is big) lets you collect more cash upfront for the risk you're taking.

- The Risk of a Volatility Spike: But if you've already sold an option and IV spikes after your trade is on, the option's price will increase, creating an unrealized loss. This is what it means to be "short Vega."

The perfect scenario for a premium seller is to sell an option when IV is high, and then watch it fall back to earth—a phenomenon known as "volatility crush." This gives your trade an extra tailwind, pushing it toward profitability alongside the daily decay you get from Theta.

Seeing the Greeks Work Together in Real Time

The options Greeks never move in a straight line; they're in a constant, dynamic dance with each other. It’s easy to think of Delta, Gamma, Theta, and Vega as separate dials on a dashboard. But the real magic—and the key to managing your trades—is understanding how they influence each other to shape an option's value from one moment to the next.

Getting a feel for this interplay moves you from a static, textbook view to a real-time, intuitive grasp of options pricing.

This is a great high-level look at the four main forces acting on your trade.

Think of it this way: Delta is your position's sensitivity to price, Gamma is the acceleration of that sensitivity, Theta is the constant drip of time decay, and Vega is its reaction to market fear.

Let's walk through how these forces interact in a real-world covered call trade over a typical week. This will help you anticipate how your own positions will react to market news, earnings, or even just a few quiet days.

A Covered Call Trade in Motion

Imagine you own 100 shares of ABC stock, which is currently trading at $150. You decide to sell a covered call against your shares with a $155 strike price that expires in 30 days. For selling this contract, you collect a premium of $2.00 per share, or $200 total.

Here’s a snapshot of the initial Greeks for your short call position:

- Delta: -0.30 (Since you're short the call, your Delta is negative.)

- Gamma: -0.04

- Theta: +0.03

- Vega: -0.08

You are long Theta, which is exactly what an option seller wants. But you're short Delta, Gamma, and Vega. This means you profit as time passes, but you'll see unrealized losses if the stock price rises, if that price move accelerates, or if overall market volatility spikes.

Scenario 1: The Stock Jumps Suddenly

Three days later, ABC announces some good news. The stock jumps from $150 to $154, landing much closer to your short strike price. What happens to your Greeks now?

- Delta Changes: Your call is now closer to being in-the-money. Its Delta might jump from -0.30 to -0.48. That change is Gamma in action—it measures the rate of change of Delta. Your position just became much more sensitive to every little price move.

- Gamma Risk Increases: Because the option is now closer to the at-the-money point, its Gamma becomes more negative, maybe shifting from -0.04 to -0.07. This means your directional risk will now accelerate even faster with each subsequent dollar the stock moves up.

- Vega Also Rises: The sudden news probably caused implied volatility (IV) to jump. A rise in IV makes all option premiums more expensive, creating a temporary, unrealized loss on your short call. This is your "short Vega" risk coming to life.

Even though three days of Theta decay have worked in your favor, the negative hits from Delta and Vega have likely put your trade in the red for the moment.

Scenario 2: The Calm After the Storm

Now, let's say the dust settles and the stock just chops around $153 for the next two weeks. With only 15 days left until expiration, the dynamic shifts again. This is where the crucial Theta-Vega tradeoff really comes into play.

The "Theta-Vega tradeoff" is a core concept for option sellers. It describes how options with high premiums (often driven by high Vega from big IV) also offer the most potential time decay (Theta). As a seller, you collect that rich premium upfront but accept the risk that volatility will rise even more or the stock will make a sharp move against you.

With expiration getting closer:

- Theta Accelerates: Your Theta value starts to ramp up—big time. The option, which might have been losing $3 per day in value, could now be decaying by $6 or $7 daily. The ice cube is melting much, much faster.

- Vega Decreases: As time evaporates, the impact of volatility shrinks. The option’s Vega will get smaller, making your position far less sensitive to any new swings in IV.

This interaction is the primary profit engine for options sellers. You are essentially trading the initial risk of high Vega for the powerful, accelerating benefit of high Theta as expiration nears.

The ability to see these changes live isn't just for Wall Street anymore. Over the last decade, access to real-time Greeks data has become a global standard. This is how modern retail platforms like Strike Price can provide instant updates when a stock jumps or volatility spikes, giving income-focused sellers timely alerts on assignment probabilities and time decay throughout the day. You can learn more about the global infrastructure behind real-time options Greeks from Exchange Data International.

Applying the Greeks to Your Selling Strategy

Alright, you've got the individual definitions down. Now comes the fun part: putting that knowledge to work. Let's translate this Greek alphabet soup into a real-world playbook for selling covered calls and cash-secured puts.

This is where the numbers on your screen stop being abstract concepts and start becoming your trading plan. The goal isn't just to know what the Greeks are; it's about using them to build trades that perfectly match your income goals and how much risk you're willing to take.

Using Delta to Select Your Strike Price

For income sellers, Delta is your single most important tool for picking a strike price. Period. It's a two-for-one deal, telling you both how sensitive your option is to price changes and giving you a rough probability of assignment. No more picking strikes based on a hunch.

A common and powerful approach is to sell options at a specific Delta that reflects your target win rate. For instance, if you sell a call option with a 0.20 Delta, you’re effectively setting up a trade that has roughly an 80% chance of expiring worthless. That’s your sweet spot.

Using Delta as your guide transforms strike selection from an art into a science. It allows you to systematically choose trades that fit your risk profile, whether you're aiming for conservative, high-probability income or seeking higher premiums with slightly more risk.

So, how do different Delta ranges translate into an actual trading plan for covered calls and secured puts? Let's lay it out.

Using Delta to Guide Your Selling Strategy

This table breaks down how you can use different Delta ranges to align your trading style with your goals, whether you're playing it safe or looking for bigger premiums.

| Delta Range | Strategy Type | Typical Risk/Reward Profile | Best For |

|---|---|---|---|

| 0.10-0.20 | Conservative | Low premium income, but a very high probability of expiring worthless. | Generating consistent, smaller income streams with minimal risk of assignment. |

| 0.21-0.35 | Balanced | A solid mix of premium income and a high probability of success. | The "sweet spot" for many sellers aiming for a good balance of income and safety. |

| 0.36-0.50 | Aggressive | Higher premium income, but with a much lower probability buffer. | Experienced sellers who are comfortable managing trades and accepting higher assignment risk. |

This framework gives you a clear, data-driven starting point for every single trade you make. It’s a core principle behind how platforms like Strike Price help sellers find trades that line up with specific, measurable probability targets.

A Practical Walkthrough Selling a Covered Call

Let’s make this real. Imagine you own 100 shares of TechCorp (TC), currently trading at $250 per share. You want to generate some income. Instead of just picking a strike that "looks good," you're going to use the Greeks.

You're aiming for a balanced trade—a nice premium with a high probability of success. You decide a Delta around 0.30 is your target.

- Analyze the Options Chain: You look at the contracts expiring in 45 days and find the $265 strike call. It has a Delta of -0.28. Perfect. That’s close to your target and implies roughly a 72% probability the option expires worthless.

- Check Theta and Vega: The option's Theta is +0.06, meaning you'll collect about $6 per day from time decay. Its Vega is -0.15, so if volatility drops, your position benefits.

- Execute the Trade: The premium is $3.50 per share. You sell one contract and instantly collect $350 in cash.

See the difference? By using the Greeks, you've built a trade with a known probability profile. You understand your daily decay and volatility risk. It's a world away from guessing. For a deeper dive, our guide on how to sell covered calls for income is a great next step.

A Practical Walkthrough Selling a Cash Secured Put

Now, let's flip it. Say you want to buy 100 shares of RetailGiant (RG), trading at $120. You'd be happy to own it, but even happier to get it at a discount. A cash-secured put is the perfect tool for the job.

You decide you'd be a buyer at $115, so you look at puts with that strike price expiring in 30 days.

- Find Your Strike's Delta: The $115 put has a Delta of -0.32. This tells you there’s about a 32% chance the stock drops below $115 by expiration—and a 68% chance it stays above it.

- Evaluate the Premium: The premium is $2.10, so you collect $210 for selling the put. If you get assigned, this premium effectively lowers your cost basis to $112.90 per share ($115 - $2.10).

- Monitor Gamma Risk: Since this option is closer to the money, its Gamma will be higher. You know you'll need to watch this one more closely if the stock starts to drop, because your probability of assignment will start changing much faster.

In this scenario, the Greeks clearly defined your risk and reward. You either keep the $210 and the stock stays above $115, or you buy a stock you already wanted at a nice discount. It's a strategic, win-win setup built on data, not hope.

Three Simple Rules for Probability Driven Selling

Alright, we’ve taken a close look at the individual Greeks. Now it’s time to put them to work. The good news is, you don’t need a math degree or a wall of monitors to successfully sell options for income. You just need a simple, repeatable framework built on the principles of probability.

This is where everything we've covered comes together into three memorable, actionable rules. Think of this as your pre-trade checklist—a straightforward guide to making smarter, data-driven decisions every time you sell a covered call or cash-secured put.

Rule 1: Let Delta Guide Your Strike Price

For an option seller, Delta is easily the most powerful tool in the box. Its ability to act as a rough probability gauge is the bedrock of strategic selling. Instead of just guessing which strike price feels right, you can use Delta to systematically align every trade with your personal risk tolerance.

This flips the script on how most people trade. You decide on your desired probability of success first, then you go find the strike that matches it. For example, selling a call with a 0.20 Delta isn't a random act; it's a conscious decision to enter a trade with an approximate 80% chance of success.

By letting Delta guide your strike selection, you remove emotion and guesswork from the equation. You're no longer just selling an option; you're selling a contract with a predefined and measurable probability of profit.

If you really want to get this concept down, our guide on calculating the options probability of profit is the perfect next step. It's a crucial part of building a disciplined, consistent strategy.

Rule 2: Make Theta Your Best Friend

As an option seller, Theta is your paycheck. Time decay is the relentless force working in your favor, day in and day out, slowly eroding the value of the option you sold. Your job is simply to put your trades in the best position to benefit from it.

That means actively seeking out situations where Theta is working its hardest for you. Most traders find the sweet spot is selling options with 30 to 45 days until expiration. This window typically offers the best daily decay without taking on the wild Gamma risk that comes with weekly options.

Making Theta your best friend also means knowing when to stay away. It's usually a bad idea to hold a short option through a high-stakes event like an earnings report, unless it's a calculated part of your strategy. One big price move can wipe out weeks of hard-earned Theta gains in an instant.

Rule 3: Respect Gamma's Power

Finally, and this is a big one, you must always respect the power of Gamma. If Theta is your best friend, Gamma can be your worst enemy, especially as expiration gets closer. Think of Gamma as the accelerator for your risk, and it really kicks into high gear for at-the-money options in their final week.

A position with high Gamma can turn a comfortable, winning trade into a massive headache with just a small move in the stock. That’s why knowing how to manage your trades near expiration is such a critical skill.

Here are two easy ways to keep Gamma risk in check:

- Close or Roll Early: You don't get extra points for holding a winning trade to the very last day. Closing a position after it's hit 50-75% of its max profit is what the pros do. It's a smart way to lock in gains and take risk off the table.

- Avoid Weekly Options (At First): Unless you're an experienced trader who understands the dynamics, the extreme Gamma of weekly options introduces a ton of risk for a relatively small amount of extra premium.

By sticking to these three simple rules, you can build a solid framework that turns the theory of the Greeks into a practical, powerful, and profitable trading strategy.

Look, the goal here isn't to turn you into a math whiz crunching numbers all day. It's about making you a smarter, more strategic trader. The Greeks aren't just abstract theory; they're your core risk management tools for trading options for income.

By getting a feel for how Delta, Gamma, Theta, and Vega play off each other, you've suddenly got a roadmap for navigating the day-to-day chop of the market. Instead of just placing a trade and hoping for the best, you can start making decisions based on probabilities.

The real takeaway is this: while you absolutely need to understand these concepts, modern tools do all the heavy lifting for you. Your job is to interpret the data, not calculate it by hand.

Platforms like Strike Price were built from the ground up to turn these complex sensitivities into simple, actionable insights. It shows you the probability of success for every single trade. It’s time to stop trading in the dark.

You now have the foundation to use these powerful tools and start trading with confidence, turning risk into something you can actually measure and manage. You’re moving from guesswork to executing a clear, data-driven plan.

A Few Lingering Questions on Options Greeks

We've covered a lot of ground, but a few questions always pop up when traders start digging into the Greeks. Let's tackle some of the most common ones you’ll run into.

Which Greek Is Most Important for a Covered Call Seller?

For anyone selling covered calls, it really boils down to two: Delta and Theta. Think of them as your primary tools for success.

Delta is your guide for picking a strike price. A low Delta signals a high probability that the option will expire worthless, which is exactly what you want. Theta, on the other hand, is the engine of your income. It’s that steady time decay that chips away at the option's value every single day, putting premium in your pocket.

Do I Need to Calculate the Greeks Myself?

Absolutely not. Thankfully, those days are long gone. Every modern brokerage platform and specialized tool like Strike Price handles all the heavy lifting, calculating and displaying the Greeks for you in real time.

Your job isn't to be a mathematician. It's to understand what those numbers are telling you so you can make smarter, more informed decisions with your trades.

What Is a Gamma Squeeze and Should I Worry About It?

A Gamma squeeze is one of those wild market events you hear about—a sudden, explosive price move that feeds on itself. It’s often triggered when market makers who are short a ton of calls have to rush to hedge their positions as a stock price screams upward. To stay neutral, they have to buy the underlying stock, which just pushes the price even higher.

As an individual retail trader, you won't be the one causing a Gamma squeeze. However, you can definitely get caught in the tidal wave of volatility it creates. It’s a powerful reminder of why managing your risk is non-negotiable, especially as your options get closer to expiration.

Stop guessing and start trading with a data-driven edge. Strike Price turns complex Greeks into simple probabilities, giving you real-time alerts and tailored strategies to consistently generate income. Discover how Strike Price can transform your options selling strategy today.