Greek Options Explained for Income Traders

If a stock moves past your strike, the option can be assigned — meaning you'll have to sell (in a call) or buy (in a put). Knowing the assignment probability ahead of time is key to managing risk.

Posted by

Related reading

Out of Money Call Options A Guide to Consistent Income

Learn how to use out of money call options to generate consistent income. This guide covers key strategies, risk management, and real-world examples.

How Options Are Priced A Practical Guide for Investors

Understand how options are priced with this clear guide. Learn about intrinsic value, implied volatility, and pricing models to improve your investing strategy.

How to Trade Stock Options for Steady Weekly Income

Learn how to trade stock options with a simple, data-driven approach. This guide covers covered calls, puts, and risk management for consistent income.

For income traders, understanding the Options Greeks is the key to managing risk, picking better strike prices, and consistently bringing in cash from strategies like covered calls and cash-secured puts. They're not just for academics; they're your guide to smarter, safer trading.

Your Dashboard for Smarter Options Trading

Think of the Options Greeks—Delta, Gamma, Theta, and Vega—as the dashboard for your trading portfolio. Just like your car's gauges show your speed, fuel level, and engine temp, the Greeks reveal the hidden risks and opportunities inside every options contract.

We’re going to pull these concepts out of the textbook and put them into practice. Forget the dense formulas for a minute. The real goal is to understand what each Greek is telling you and, more importantly, how to act on that information.

Quick Guide to the Core Options Greeks

To get started, here's a simple reference table that breaks down what each Greek measures and why it's so important for anyone selling options for income.

| Greek | What It Measures | Why It Matters for Sellers |

|---|---|---|

| Delta | Sensitivity to the stock's price | Shows your directional risk and the odds of assignment. |

| Gamma | The rate of change of Delta | Warns you about how quickly your risk can accelerate. |

| Theta | Sensitivity to the passage of time | Represents your daily income from time decay. It's your best friend. |

| Vega | Sensitivity to implied volatility | Shows how market "fear" pumps up the premium you collect. |

Think of this table as your roadmap for the rest of this guide. We’ll dive deep into each one, showing you how to use them to nail your strike prices, manage your positions, and build a reliable income stream.

Key Takeaway: The Greeks aren't just numbers on a screen; they're actionable signals. They turn abstract market forces into clear data, helping you shift from guessing to making informed, probability-driven decisions.

By the end of this guide, you’ll be able to read this "dashboard" with confidence. You'll see exactly what forces are moving your trades, giving you the power to stay in control, sidestep nasty surprises, and build a much stronger income strategy. Let's get into it.

Delta and Gamma: The Speed and Acceleration of Your Trade

If you think of your options portfolio as a high-performance car, Delta and Gamma are its speedometer and accelerator. They're the first two Greeks most traders learn because they directly measure how your position reacts to the underlying stock price. Mastering them is non-negotiable for managing risk.

Delta is the speedometer. It tells you exactly how much your option's price should change for every $1 move in the stock. It’s your most direct measure of directional risk.

Understanding Delta in Action

Delta measures an option's sensitivity to price changes in the underlying stock. For call options, Delta ranges from 0 to 1, while for puts it ranges from -1 to 0.

So, if you own a call option with a 0.50 Delta, its value will increase by about $0.50 for every $1 the stock price rises. Simple enough.

But for income sellers, Delta pulls double duty. It also works as a quick, real-world estimate of the probability that an option will expire in-the-money (ITM).

- A 0.30 Delta Call: This contract has roughly a 30% chance of finishing ITM. If you sold a covered call, this means there's a 30% chance your shares get called away.

- A -0.20 Delta Put: This contract has roughly a 20% chance of finishing ITM. For a cash-secured put seller, that's a 20% probability you'll be assigned and have to buy the shares.

This simple interpretation turns Delta into a powerful tool for picking strike prices that match your comfort zone. A conservative seller might choose a call with a 0.15 Delta, targeting an 85% chance of success. For a deeper dive, check out our guide on how Delta works in option trading.

Gamma: The Accelerator Pedal

While Delta shows your current speed, Gamma is the accelerator—it measures how fast your Delta will change. It’s the rate of change in Delta for every $1 move in the stock.

A high Gamma means your risk profile can shift dramatically with little warning.

Think of it this way: a low-Gamma option is like a cruise ship. It moves, but its speed (Delta) doesn't change much. A high-Gamma option is like a sports car; a small tap on the gas can send your speed soaring.

Key Insight: Gamma risk is highest for at-the-money (ATM) options that are very close to expiration. This is why a "safe" trade can suddenly become very risky in the final week.

How Delta and Gamma Work Together

Let’s say you sold a covered call with a 0.20 Delta. The stock is at $95, and your strike is $105. The position feels safe; the stock needs to rally $10 to threaten your shares.

Now, imagine the stock suddenly jumps to $104 just one day before expiration.

- Your Delta Skyrockets: Because Gamma is so high near expiration, your Delta might jump from 0.20 to 0.60 or more. Your speedometer just went from 20 mph to 60 mph.

- Assignment Risk Explodes: Your probability of assignment is no longer 20%—it's now closer to 60%. The entire risk profile of your trade just flipped.

This explosive shift is all thanks to Gamma. An option with a Gamma of 0.05 will see its Delta increase by 0.05 for every $1 the stock rises. If that stock rallies $5, your initial 0.20 Delta becomes 0.45 (0.20 + (5 * 0.05)), completely changing the game. Understanding this relationship is how you avoid nasty surprises and manage your trades before they get away from you.

If Delta and Gamma are about reacting to a stock's price moves, Theta and Vega are the two Greeks that truly define the income seller's game. They represent the forces we rely on most: the unstoppable march of time and the emotional tides of the market. Getting this pair right is the secret to consistently collecting premium.

Think of Theta as your silent partner, the one working for you 24/7, even on weekends. It's the measure of how much an option's price decays with each passing day.

For a seller, this decay is your bread and butter. You're essentially selling an asset that's designed to lose value over time—like selling a scoop of ice cream on a hot summer day. Profit is practically built-in.

Theta: The Slow, Inevitable Melt

Every options contract has an expiration date stamped on it. As that date draws closer, the "what if" value of the option—its extrinsic value—starts to evaporate. We call this time decay, and Theta puts a dollar amount on it.

A Theta of -0.05 means the option's price is expected to drop by $0.05 every day, assuming nothing else changes. Since one contract controls 100 shares, that's a $5 daily profit dripping into your account just for holding the position.

Key Takeaway: As an income seller, you are "Theta positive." Time is your greatest ally. Your job is to sell options with healthy premium and let Theta do its thing, slowly melting that value down to zero.

But this melt isn't a steady drip. Theta decay accelerates. It’s slow and gradual for options far from expiration but picks up speed dramatically in the last month or so. This is why many sellers focus on contracts with 30 to 45 days left—it's the sweet spot where the decay really starts to kick in.

Vega: The Market's Fear Gauge

Now for Vega. This Greek measures an option's sensitivity to changes in implied volatility (IV). You can think of IV as the stock market's collective guess on how much a stock will swing around in the near future. It’s often called the "fear gauge."

When the market gets nervous—maybe an earnings report is coming up, or there's big economic news on the horizon—implied volatility shoots up. This inflates option premiums because the perceived risk of a big move is higher. Vega tells you exactly how much an option's price will change for every 1% shift in IV.

For sellers, this creates a huge opportunity:

- High IV: This is when you want to sell. It means you can collect fatter premiums for taking on the same level of risk.

- Low IV: Premiums are thinner because the market isn't expecting much action.

If an option has a Vega of 0.15, its price will climb by $0.15 for every 1% jump in implied volatility. As a seller, you have negative Vega, which means a drop in IV is what you want. Selling an option when IV is sky-high and watching it fall back to earth—a phenomenon traders call "volatility crush"—can hand you a quick and tidy profit. You can dive deeper into how to use Vega in your options trading strategy in our detailed guide.

The Balancing Act: Theta vs. Vega

Theta and Vega are in a constant dance. High implied volatility gives you that juicy premium (which is great), but it also means the stock is expected to be a wild ride. On the other hand, stable, low-volatility stocks offer smaller premiums but a much calmer experience.

An effective income strategy is all about finding that balance. You want to sell options with enough IV to make the trade worthwhile, but without taking on so much directional risk that you're constantly sweating a huge price swing.

By understanding both Theta and Vega, you can see the complete picture. It’s not just about where the stock price might go; it’s about how time and market fear will impact the premium you’ve collected. That’s how you move from just picking a direction to truly managing a trade.

A Real-World Covered Call Case Study

Theory is one thing, but seeing the Greeks in action is where it all clicks. Let's walk through a real-world covered call trade, step by step, to see how these numbers guide your decisions from start to finish. This is where a true understanding of the Greeks transforms your trading.

Imagine you own 100 shares of XYZ Inc., which is currently trading at $152 per share. You want to generate some extra income from those shares, so you decide to sell a covered call.

Step 1: Using Delta to Pick the Right Strike Price

First things first: which strike price should you choose? You're not just throwing a dart at the option chain. You're using Delta to match the trade to your personal risk tolerance. The goal is to collect a nice premium while having a high probability of keeping your shares.

Looking at the option chain for XYZ with about 35 days to expiration, you see a couple of choices:

- $160 Strike Call: This option has a Delta of 0.30. That number tells you two things. First, the option’s price will go up by about $0.30 for every $1 XYZ stock rises. More importantly, it signals a rough 30% chance of the option expiring in-the-money. That gives you a 70% probability of success (keeping your shares and the full premium).

- $165 Strike Call: This one has a Delta of 0.18. This translates to an 18% chance of your shares being called away, giving you an even higher 82% probability of success.

For this trade, let's go with the more conservative $165 strike, aiming for that 82% probability. You sell one contract and collect a premium of $2.50 per share, pocketing $250 upfront.

Step 2: Sizing Up Your Income and Risk with Theta and Gamma

With the position open, it's time to check the other critical Greeks. The Theta for your $165 call is -0.06. This is your income engine. It means the option is losing $0.06 in value every single day from time decay alone. For you, the seller, that’s a $6 daily profit, assuming nothing else changes.

The Gamma is 0.02. A small number here is a good thing. It tells you that your Delta of 0.18 isn't going to swing wildly with small moves in the stock price. Your risk is low and stable. If XYZ's price climbs by $1, your Delta only inches up to 0.20 (0.18 + 0.02).

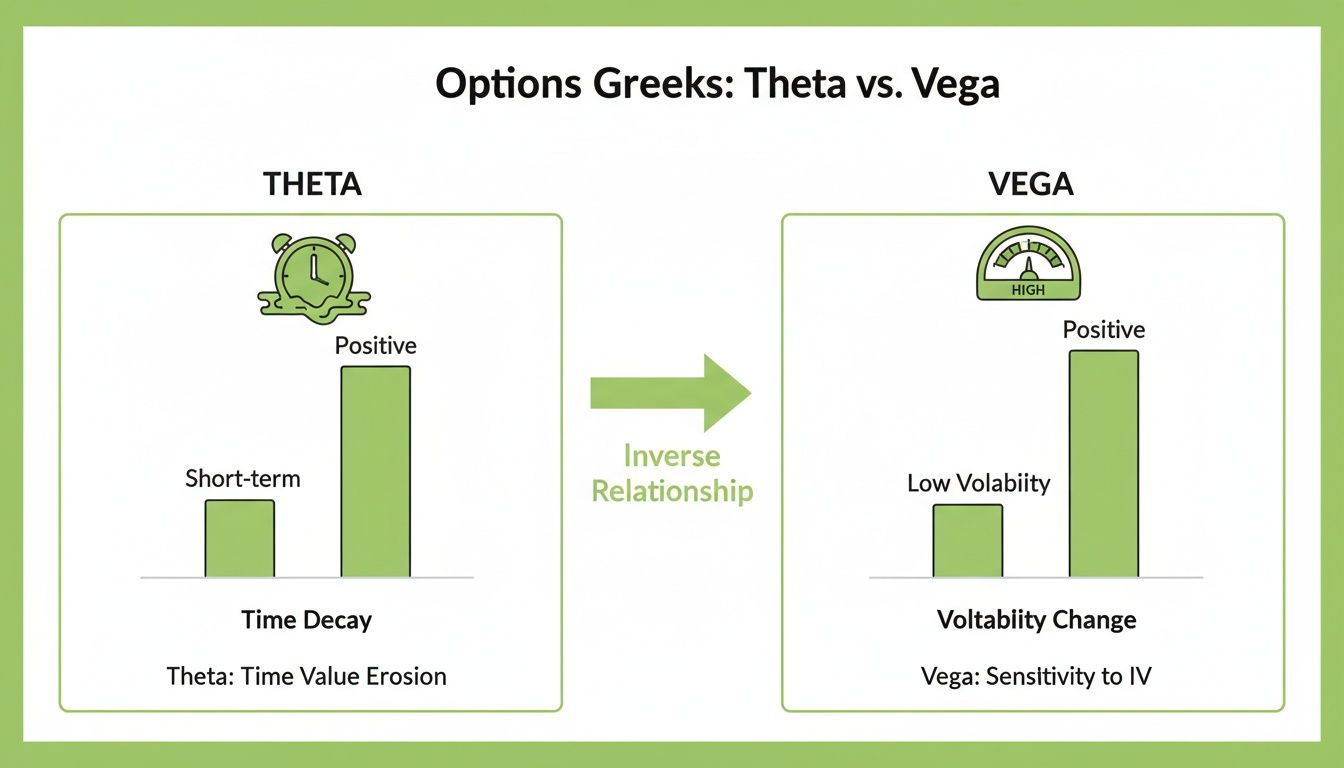

This infographic perfectly captures the constant tug-of-war between Theta (your friend) and Vega (your risk).

As sellers, we love Theta's steady decay. But we always have to watch out for Vega, because a sudden spike in volatility can pump up the option's premium and work against us. A solid covered call strategy for income is all about finding that sweet spot.

Step 3: Tracking the Trade as Time Passes

Let's fast-forward two weeks. XYZ's stock has drifted up to $156. How does our position look now?

The option's premium has actually fallen from $2.50 to $1.80, giving you an unrealized profit of $70. This happened because the power of Theta decay (14 days x ~$6/day) was stronger than the upward pressure from the stock's price increase. Your Delta has crept up to 0.28, and Gamma is now a bit higher at 0.03. The probability of assignment has increased, but it's still well within a manageable range.

Step 4: Making a Decision Based on Data, Not a Hunch

With about 21 days left until expiration, you have a choice to make. You could close the trade right now and lock in that $70 profit. Or, you could let it ride and wait for more Theta to work its magic.

Since the stock is still a long way from your $165 strike and your Delta is comfortably below 0.30, you decide to hold the position.

Key Insight: This wasn't a gut feeling. The decision came directly from reading the Greeks. The low Gamma and manageable Delta told you that your risk profile was still right where you wanted it to be.

To see how this works in practice, we've put together a table showing how the trade might evolve.

Covered Call Example: The Greeks in Action

This table shows our hypothetical covered call on XYZ stock, illustrating how the Greeks shift and inform our decisions as market conditions change.

| Event | Stock Price | Option Delta | Option Gamma | Option Theta | Trade Decision |

|---|---|---|---|---|---|

| Day 1: Trade Opened | $152 | 0.18 | 0.02 | -0.06 | Sell to open the $165 call, collecting a $250 premium. |

| Day 15: Price Drifts Up | $156 | 0.28 | 0.03 | -0.05 | Hold. Delta is still low and time decay is working in our favor. |

| Day 22: Stock Pulls Back | $154 | 0.22 | 0.02 | -0.04 | Close. We've captured a $160 profit (64%) and Theta is slowing. |

| Day 35: Expiration | (N/A) | (N/A) | (N/A) | (N/A) | Option would have expired worthless, capturing the full $250. |

As you can see, a week later the stock pulled back to $154. The option's value dropped to just $0.90. You've now captured $160 of the original $250 premium. With Theta decay starting to slow down, it's a great time to close the trade and lock in that profit.

This walk-through shows how a solid understanding of the Greeks turns options selling from a guessing game into a repeatable, strategic process.

Where the Greeks Come From

Ever look at your trading screen and wonder where all those Greek letters—Delta, Gamma, Theta—actually come from? They aren't just random numbers. They’re the direct result of a foundational formula in finance known as an option pricing model.

You definitely don't need a Ph.D. in math to trade options, but knowing the origin story of the Greeks gives you a massive edge. It explains why they behave the way they do, constantly shifting as the market breathes. Think of the Greeks as a dynamic, real-time X-ray of an option's risk.

The Black-Scholes Model

The most famous of these formulas is the Black-Scholes model. Developed in the 1970s, this model was a game-changer. For the first time, it gave traders a mathematical framework to figure out what an option should be worth. While today's markets use more advanced models, Black-Scholes is still the bedrock for understanding how options work. You can learn more about its role as a foundation for modern volatility and Greek calculations.

The model is like a recipe. It needs a few key ingredients to calculate an option’s price and its corresponding Greeks.

- Underlying Stock Price: The current market price of the stock.

- Strike Price: The price where you agree to buy or sell.

- Time Until Expiration: How much life the contract has left.

- Risk-Free Interest Rate: A baseline rate, usually tied to government bonds.

- Dividends: Any payments the stock is expected to make before expiration.

There's one more ingredient, though—and it’s the one that gives options their unique personality and risk.

The Role of Implied Volatility

The final, and arguably most important, input is implied volatility (IV). Unlike historical volatility, which is backward-looking, implied volatility is all about the future. It's the market's collective guess on how much a stock is going to move.

Key Takeaway: Implied volatility isn't a fact; it's a forecast. It's the "fear gauge" or "excitement meter" baked right into an option's premium. Higher IV means higher option prices because the market sees a bigger chance of a dramatic price swing.

This is exactly why option premiums for a company like NVIDIA can explode right before an earnings report. The market is pricing in the unknown, and that uncertainty pumps up the IV.

Because implied volatility is always changing based on news, sentiment, and expectations, the Greeks are also in constant motion. They aren't static figures. They're living metrics that update with every tick of the stock and every shift in the market's mood. That direct link is precisely why understanding the Greeks is so vital for any serious trader.

Go From Guessing to Data-Driven Trading

Once you understand the Greeks, you've taken the most important step from being a passive investor to becoming a strategic income trader. You now know that Delta is your guide to probability, Theta is your income engine, and Gamma and Vega are your risk managers. This knowledge is your edge—it’s what lets you stop guessing and start making smart, data-driven decisions.

But knowing the theory is one thing. Applying it consistently and efficiently is what separates successful traders from the rest. The days of busting out a calculator and building complex spreadsheets are over. Modern tools now bridge the gap between theory and action.

Automating Your Greek-Based Strategy

Just a few years ago, getting your hands on real-time Greeks data was a luxury reserved for the pros. Today, that data has become widely accessible, and it’s a game-changer for retail traders. We can now tap into the same kind of analytics that professional desks use to make smarter, probability-based decisions. This shift has been huge, turning what was once a complex, opaque process into something any motivated trader can master. The CME Group notes that this increased availability has leveled the playing field significantly.

What this really means is you can now automate the tedious work of monitoring your trades and get clear alerts based on Greek-driven insights. Instead of being glued to your screen watching option chains all day, you can let technology do the heavy lifting.

Key Takeaway: The goal isn't just to learn the option Greeks in theory. It’s about building a system that puts that knowledge to work for you. The best platforms today turn raw Greek data into simple, actionable signals—like assignment risk warnings and high-probability trade ideas.

For example, platforms like Strike Price are built to translate this data into clear, visual guidance. The screenshot below shows how our "Target Mode" takes your income goals and risk tolerance and turns them into specific, high-probability trade ideas.

A tool like this automatically scans the market for opportunities that actually fit your criteria. In seconds, it shows you the potential premium, probability of success, and assignment risk. It’s the perfect example of how to turn what you’ve learned into a repeatable, data-driven process that gets results.

Common Questions About Options Greeks

As you start working the Greeks into your trading, a few questions always seem to come up. Let's tackle the most common ones to clear up any confusion that trips up new income traders.

Which Greek Is Most Important for a Covered Call Seller?

While all the Greeks play a role, your two most important gauges are Delta and Theta. Think of them as the primary instruments on your trading dashboard.

Delta is your go-to for picking the right strike. It gives you a surprisingly solid estimate of the probability that your option will expire worthless—which is exactly what you want as a seller. A low Delta strike (like 0.25) tells you you’re aiming for a high probability of keeping both your shares and the full premium you collected.

Theta, on the other hand, is what pays you. As an option seller, time decay is your best friend. A healthy Theta means the option's value is reliably bleeding out each day, and that value gets transferred directly into your pocket as profit.

Can I Ignore Gamma if I Only Sell Far Out-Of-The-Money Options?

Ignoring Gamma is a dangerous game, even for those far OTM options. It's true that Gamma is tiny for strikes way out in the distance, but it won't stay tiny if the stock makes a surprise move against you. That’s the heart of Gamma risk.

Imagine a big, unexpected rally. As the stock price screams toward your strike, Gamma acts like an accelerator pedal for your Delta. Your directional risk and the odds of getting assigned can explode much faster than you’d expect.

Key Insight: You don't watch Gamma for what it is today; you watch it for what it could become tomorrow. It’s your early warning system, letting you know a "safe" trade might be heading for trouble.

Do I Need to Calculate the Greeks Myself?

Absolutely not. The days of wrestling with complex spreadsheets to calculate Greeks are long gone. Today, any modern trading platform or specialized tool does the heavy lifting for you, displaying the Greeks in real time.

Your job isn't to be a mathematician—it's to be a risk manager. The real skill is learning to interpret what the Greeks are telling you about your trade's risk, its potential reward, and its probability of success. Modern tools make this easy by translating that raw data into insights you can actually use, like profit probabilities or assignment risk alerts, so you can focus on making smarter decisions.

Ready to stop guessing and start making data-driven trades? Strike Price translates complex Greek data into simple, actionable insights. Find high-probability trades, get real-time risk alerts, and manage your income strategy with confidence. Start your free trial at https://strikeprice.app.