The Trader's Guide to Option Time Decay

If a stock moves past your strike, the option can be assigned — meaning you'll have to sell (in a call) or buy (in a put). Knowing the assignment probability ahead of time is key to managing risk.

Posted by

Related reading

Out of Money Call Options A Guide to Consistent Income

Learn how to use out of money call options to generate consistent income. This guide covers key strategies, risk management, and real-world examples.

How Options Are Priced A Practical Guide for Investors

Understand how options are priced with this clear guide. Learn about intrinsic value, implied volatility, and pricing models to improve your investing strategy.

Greek Options Explained for Income Traders

Unlock your options trading potential. This guide on greek options explained shows you how to use Delta, Gamma, and Theta to generate consistent income.

Picture an ice cube melting in your hand. Whether you do anything or not, it gets smaller over time. Option time decay, known in the trading world as Theta, works the exact same way on an option's value. It's the silent, invisible force that chips away at an option's price every single day, even if the stock it's tied to doesn't move a penny.

What Is Option Time Decay and Why It Matters

Time decay is the steady erosion of an option’s value as it creeps closer to its expiration date. This happens because the "time value" portion of an option's premium shrinks with each passing day.

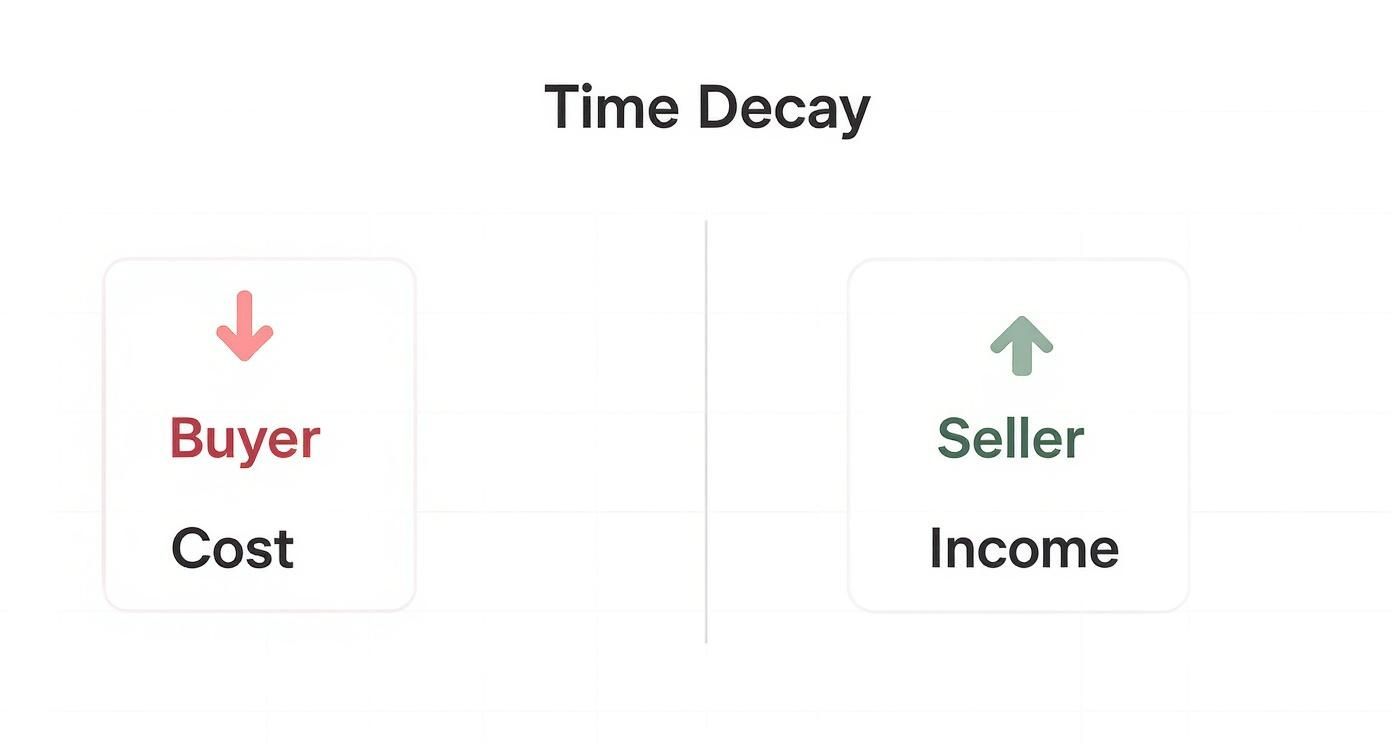

Put simply, the less time an option has left, the less time there is for the underlying stock to make a big, profitable move. For an option buyer, this decay is a constant headwind—a daily 'tax' just for holding the position. For an option seller, however, it's the gift that keeps on giving. This is why getting a handle on time decay is non-negotiable for any serious options trader.

Intrinsic vs. Extrinsic Value

To really get how time decay works, you have to understand that an option's price is made of two parts:

- Intrinsic Value: This is the option's real, tangible worth if you were to exercise it right now. For a call option, it's how much the stock price is above the strike price.

- Extrinsic Value: Think of this as the "hope" premium. It's the extra amount you pay for the potential of the option becoming more profitable before it expires.

Time decay is a sniper that only targets an option's extrinsic value. It never touches the intrinsic value. As expiration gets closer, that extrinsic value starts to melt away, and the melting speeds up dramatically in the final few weeks.

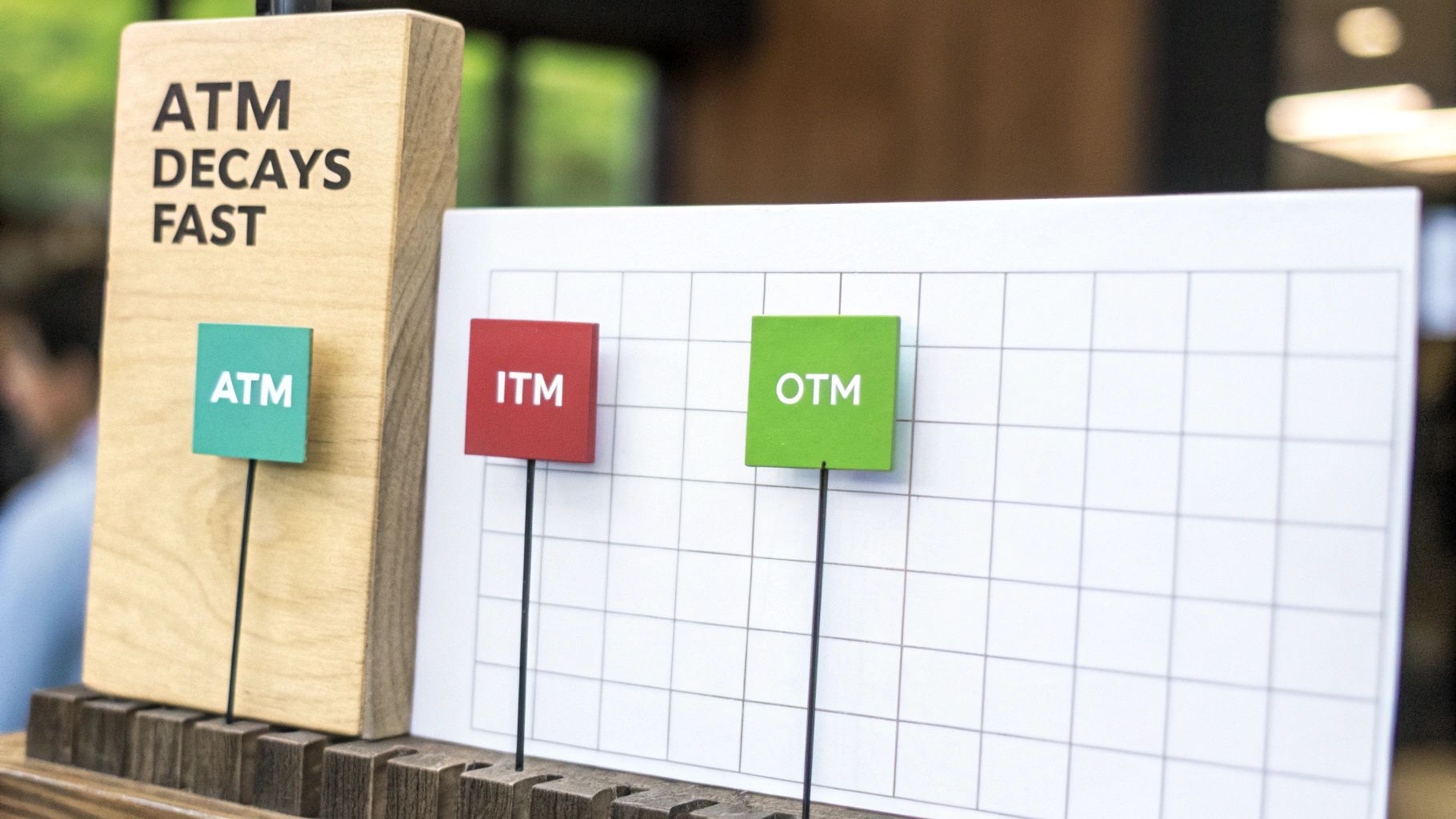

An at-the-money (ATM) option is the most exposed to time decay. Since its value is almost entirely made of extrinsic premium, it has the most to lose from the simple passage of time.

This decay, measured by the Greek letter Theta, isn't a straight line. For example, a 30-day ATM call option might have a Theta of -0.05. This means it's set to lose about $0.05 per share ($5 per contract) each day, assuming nothing else changes. But this erosion gets much faster in the last couple of weeks before expiration—a critical window for traders.

Deep in-the-money or far out-of-the-money options decay much slower because they have less extrinsic value to begin with. You can dive deeper into the critical role of Theta and the other Greeks in our complete option greeks explained guide. This is a fundamental principle of options pricing, and you can explore more about how time decay patterns work on barchart.com.

To help you get a clear picture of how Theta works, here's a quick summary of its key characteristics.

Key Characteristics of Option Time Decay (Theta)

| Characteristic | Impact on Option Value | Who Benefits |

|---|---|---|

| Passage of Time | Always negative for long options (buyers). The option's value decreases every day. | Option Sellers |

| Proximity to Expiration | The rate of decay accelerates significantly as the expiration date approaches. | Option Sellers |

| Moneyness | At-the-money (ATM) options experience the fastest decay. | Sellers of ATM Options |

| Volatility | Not a direct driver, but high volatility inflates extrinsic value, giving Theta more to erode. | Option Sellers |

This table makes it clear: time is the natural enemy of the option buyer and the best friend of the option seller. Understanding this dynamic is the first step toward building smarter, more resilient options strategies.

The Accelerating Nature of the Theta Decay Curve

One of the biggest mistakes new options traders make is thinking that option time decay is a slow, steady drip. It’s not. A better way to think about it is like a snowball rolling downhill—it starts off small and slow, but it picks up a dangerous amount of speed the closer it gets to the bottom.

This is what we call the Theta decay curve. It’s a visual representation of how an option's value bleeds away exponentially, not in a nice, neat straight line.

An option with 90 days left until it expires might barely lose any value to time from one day to the next. In this early stage, time is almost a non-factor. But as that expiration date gets closer, the decay starts to accelerate, hitting its stride in the last 30 to 45 days. This is what seasoned traders call the "danger zone" for option buyers.

Just to put some numbers on it, an option might lose only one-third of its time value in the first 60 days of its life. But in those final 30 days? It can easily burn through the remaining two-thirds. Why? Because with each passing day, the chances of the stock making a big, profitable move shrink dramatically. Less time equals less hope.

The Final 30 Days

This is where the real action happens. In the last month of an option's life, the Theta decay curve gets incredibly steep, meaning the value is evaporating at its fastest possible rate.

If you’re an option buyer holding a contract in this window, you're in a race against the clock. Even if you're right about the stock's direction, a slow-moving stock might not be enough to outpace the rapid decay of your premium. It's a tough spot to be in.

On the flip side, if you're an option seller, these last 30 days are your sweet spot. That accelerated decay is working for you, chipping away at the value of the option you sold and making it more likely you’ll get to keep the entire premium.

This chart really drives home the fundamental conflict between the buyer and the seller.

As you can see, it's a zero-sum game. Every dollar the buyer loses to time decay is a potential dollar the seller gains.

Key Takeaways from the Decay Curve

Getting a feel for the shape of this curve is a game-changer. It tells you everything you need to know about when to get in or out of a trade to either protect your capital or lock in your profits.

The big lesson here is simple: time is not an option's friend. For buyers, hanging on too long is an expensive mistake. For sellers, that accelerating decay is the engine that powers their entire income strategy.

At the end of the day, you have to respect the curve. Ignoring the exponential nature of option time decay is one of the fastest ways for an option buyer to watch their investment vanish into thin air. For a seller, understanding it is the foundation of their success.

How Strike Price Affects Time Decay

Not all options are created equal when facing the relentless clock of time decay. Where an option's strike price sits relative to the stock's price—its moneyness—is a huge factor in how quickly its value evaporates.

The most vulnerable options are those that are At-The-Money (ATM). An ATM option has a strike price right around the current stock price, meaning it has little to no intrinsic value. Its premium is almost entirely made of extrinsic value—basically, the "hope" and time premium.

Because its value is all extrinsic, an ATM option has the most to lose from the simple passage of time. This makes ATM options the fastest-decaying contracts, a critical insight whether you're buying or selling.

Comparing Decay Across Moneyness

The rate of option time decay changes dramatically based on whether an option is In-the-Money, At-the-Money, or Out-of-the-Money. Each has a totally different risk profile when it comes to Theta.

In-the-Money (ITM) Options: These options already have intrinsic value, which acts as a buffer against time decay. While their extrinsic value still decays, that built-in profit provides some protection, leading to a slower overall loss of value compared to ATM options.

Out-of-the-Money (OTM) Options: Far OTM options don't have much premium to begin with. Although they're very likely to expire worthless, their low starting value means the dollar amount they lose each day is small. Theta's impact is less dramatic in absolute terms, even if the percentage loss is high.

The key takeaway is that ATM options experience the highest rate of Theta decay in absolute dollar terms. They sit in that sweet spot of maximum uncertainty and, therefore, maximum time premium for Theta to eat away.

This relationship between an option’s strike price and its decay rate is fundamental. Truly understanding what is moneyness in options gives you a strategic edge, letting you pick contracts that fit your timeline and risk tolerance.

This is where traders move beyond basic theory and into making smart, strategic choices. Option sellers often target ATM options to maximize the income they earn from decay. On the other hand, buyers might prefer ITM options for their relative stability or OTM options for their low-cost, high-leverage potential—fully aware of the risks.

Your strategy dictates whether decay works for you or against you.

Seeing Time Decay in Real-World Scenarios

Theory is one thing, but watching option time decay eat into a real trade is where the lesson truly sinks in. Let's walk through two practical scenarios to see how Theta works—first as an enemy to the option buyer, and then as a powerful friend to the option seller.

Example 1: The Call Buyer’s Race Against Time

Imagine a trader, Alex. He's convinced that XYZ stock, currently trading at $48 a share, is about to break out. To play this hunch, he decides to buy a call option.

Here’s the setup:

- Action: Buys one XYZ Call Option

- Strike Price: $50 (just a bit out-of-the-money)

- Expiration: 30 days from now

- Premium Paid: $2.00 per share, which comes out to $200 for the contract (covering 100 shares)

For the next week, the stock just... sits there. XYZ barely budges from $48, making no big moves in either direction. Even though the stock price hasn't dropped, Alex checks his account and sees his call option is now only worth $1.65 per share, or $165.

That $35 loss is pure option time decay in action. Every single day that ticked by chipped away at his contract's extrinsic value, pushing his break-even point further out of reach.

Example 2: The Put Seller’s Ally

Now, let's flip the script and meet another trader, Sarah. She's neutral to bullish on ABC stock, which also happens to be trading at $48 per share. She wouldn't mind owning the stock if it dips a little, but she's mainly looking to collect some income. She decides to sell a cash-secured put.

Here are the details of her trade:

- Action: Sells one ABC Put Option

- Strike Price: $45 (safely out-of-the-money)

- Expiration: 30 days away

- Premium Received: $1.50 per share, putting $150 in her account upfront.

Just like in the first scenario, ABC stock trades sideways for a week, hovering around the $48 mark. When Sarah pulls up her position, she sees the value of the put she sold has dropped to $1.10, or $110.

This is fantastic news for Sarah. Since she's a seller, the option's decaying value works in her favor—it is her profit. She could choose to buy back the put for $110 right then and there, locking in a $40 profit without having to wait for expiration. All thanks to time decay.

These examples perfectly illustrate the two-sided nature of Theta. For Alex, the buyer, it was a constant drain on his position. For Sarah, the seller, it became a steady source of potential income.

Statistical studies show this effect gets far more dramatic as expiration approaches. An option might lose just 0.5% of its value per day when it's far from expiration, but that can jump to 5% or more per day in the final week. You can find more insights on how time decay patterns accelerate on einvestingforbeginners.com. Getting a handle on this acceleration is absolutely critical for managing your risk and maximizing returns.

Strategies to Profit From Option Time Decay

Understanding time decay is one thing, but actually turning it into a profitable strategy is a whole different ballgame. For option sellers, Theta isn't just a risk factor—it's the engine that powers the entire income machine.

This is what allows you to get paid for taking on calculated risk over a set period.

On the flip side, if you're buying options, Theta is the constant, nagging headwind you're fighting against. To succeed, you have to think beyond simple directional bets and structure your trades to sidestep that daily decay.

Harnessing Theta as an Option Seller

Sellers intentionally put themselves on the winning side of the time decay equation. The entire game plan is to collect a premium upfront and then let the clock do the heavy lifting.

As Theta chips away at the option's value, the goal is for it to expire worthless, letting you pocket the entire premium. Two of the most common strategies are built specifically for this purpose.

- Selling Covered Calls: This is where you sell a call option against stock you already own (100 shares for every contract). Think of it as generating rent from your existing holdings. As time ticks by, the call option you sold loses value, and if it expires worthless, you keep the full premium. Learn how to sell covered calls for income and start turning your portfolio into a cash-flow generator.

- Selling Cash-Secured Puts: With this strategy, you sell a put option on a stock you'd be happy to own at the strike price. You get paid a premium for agreeing to buy the stock if its price drops below your strike. If the stock stays above it, the option expires worthless, and that premium is pure profit, thanks almost entirely to time decay.

For an option seller, time is your greatest asset. Every day the market is open—and even when it’s closed over the weekend—Theta is silently working in your favor, reducing the liability of the option you sold.

Mitigating Theta as an Option Buyer

Option buyers are in a constant battle against the clock. Since time decay ramps up as expiration gets closer, just buying a short-term option and hoping for a quick, massive price move is a low-probability play.

Instead, smart buyers use specific tactics to give themselves a fighting chance against Theta's relentless drain. These strategies either slow down the rate of decay or use a second option to help pay for the cost of the first.

- Buying Longer-Dated Options (LEAPS): Rather than buying an option that expires in 30 days, a trader might buy one that expires in a year or more. These are called LEAPS (Long-Term Equity AnticiPation Securities). Their rate of time decay is much, much slower, which gives the underlying stock plenty of time to make the big move you're expecting.

- Using Vertical Spreads: A vertical spread involves buying one option and selling another of the same type and expiration, just at a different strike price. For a debit spread (where you pay to open the position), the premium you collect from the option you sold helps offset the cost and time decay of the option you bought. This can slash the position's Theta, making it far less of a drag on your trade.

Comparing Strategies For Managing Theta

Whether you're selling options to collect premium or buying them for a directional bet, your relationship with Theta is what defines your strategy. Sellers embrace it, while buyers have to find clever ways to neutralize its impact.

The table below breaks down how some common strategies interact with time decay.

| Strategy | Primary Goal | How It Uses Time Decay | Ideal for |

|---|---|---|---|

| Selling Covered Calls | Generate income from existing stock holdings | Profits directly as Theta erodes the option's value | Investors seeking to enhance returns on long-term stock positions. |

| Selling Secured Puts | Generate income or acquire stock at a lower price | Profits directly as Theta erodes the option's value | Investors who are willing to buy a specific stock if the price drops. |

| Buying LEAPS | Long-term directional bet with less decay | Minimizes the impact of Theta by using very long expiration dates | Traders who want to control a large stock position with less capital and time. |

| Buying Vertical Spreads | Directional bet with reduced cost and risk | The sold option's premium helps offset the Theta of the bought option | Traders who want to make a directional bet with a defined risk and lower cost. |

Ultimately, understanding your relationship with option time decay is non-negotiable. It dictates which strategies you should use and how you should manage your trades from start to finish.

Common Questions About Option Time Decay

Even when you get the mechanics down, some real-world questions about option time decay always seem to pop up. It's one thing to understand the theory, but another to see how it plays out day-to-day. Let's walk through some of the most common points of confusion to make sure this critical concept is crystal clear.

Getting these answers straight will help you go from just knowing the definition to actually using Theta to your advantage.

Does Time Decay Happen Over the Weekend?

Yes, it absolutely does. The stock market might close up shop on Friday afternoon, but time keeps marching on through Saturday and Sunday. Because of this, an option's time value continues to quietly burn away.

This is why you'll often see a noticeable drop in the value of near-the-money options on Monday morning compared to Friday's close, even if the underlying stock hasn't moved a penny. Option sellers love this "weekend decay" effect—it's a big reason why selling weekly options is such a popular income strategy. You get to collect premium for two full days while the market is completely still.

For an option seller, the weekend is your silent partner. Time doesn't stop, and neither does Theta's relentless march. That steady 48-hour erosion of premium can give your short option positions a serious profitability boost.

How Does Volatility Affect Time Decay?

Volatility and time decay have a push-and-pull relationship. Think of high implied volatility (IV) as an air pump for an option's price—it inflates the extrinsic value, giving Theta more premium to chew on every single day.

When IV is high, options are more expensive, and sellers can collect a bigger paycheck for taking on risk. But here's the double-whammy: if that IV later drops (something traders call "volatility crush"), the option's premium gets squeezed from two sides. Time is still passing, and now the volatility premium is deflating, too.

This makes selling options during periods of high IV a potent one-two punch. You're set up to benefit from both the steady tick of the clock (Theta) and a potential drop in market anxiety (Vega).

Is Time Decay the Same for Calls and Puts?

Yep. Assuming all other variables are the same—same underlying stock, same strike price, same expiration date—time decay treats calls and puts exactly the same. Theta is always a negative number for an option buyer, whether you bought a call or a put. It's a cost that reduces the option's value over time.

Picture an at-the-money call and an at-the-money put on the same stock with the same expiration. Their rate of option time decay will be nearly identical. Decay is all about an option's extrinsic value and its remaining lifespan, not which direction you think the stock is headed.

What Is the Best Way to Avoid Losing Money to Time Decay?

If you're an option buyer, time is not your friend. So, how do you fight back?

- Buy More Time: The simplest method is to buy options with much longer expiration dates, like those with 90+ days left. The daily decay rate (Theta) on these long-dated contracts is painfully slow compared to the rapid decay of weekly options.

- Use Debit Spreads: This is a savvier tactic. You buy one option and simultaneously sell another, further out-of-the-money option. The cash you collect from selling the second option helps pay for the time decay on the one you bought.

Of course, the best way to stop losing to Theta is to get it on your side. When you become an option seller using strategies like covered calls or cash-secured puts, you flip the script entirely. Time decay goes from being a headwind you fight every day to the very engine that drives your potential income.

Stop guessing and start selling with confidence. Strike Price provides real-time probability data for every strike, helping you find the perfect balance between premium income and safety. Turn your portfolio into a consistent income stream with smart alerts and data-driven strategies. Discover your next winning trade.