Covered Call Tax Treatment Explained: Maximize Your Gains

If a stock moves past your strike, the option can be assigned — meaning you'll have to sell (in a call) or buy (in a put). Knowing the assignment probability ahead of time is key to managing risk.

Posted by

Related reading

A Step-by-Step Covered Calls Example for Consistent Income

Unlock consistent income with our step-by-step covered calls example. This guide breaks down the strategy, risks, and outcomes to help you trade confidently.

Long Call and Short Put The Ultimate Synthetic Stock Guide

Unlock the power of the long call and short put strategy. This guide explains how synthetic long stock works, its benefits, risks, and how to execute it.

What is a Call Spread? A Clear Guide to Bull and Bear Spreads

What is a call spread? Discover how bull and bear spreads limit risk and sharpen your options trading strategy.

Understanding Covered Call Tax Treatment Fundamentals

Covered calls can feel like a complex dance at first, but understanding the tax implications doesn't have to be a tango of confusion. Think of it like renting out your stocks. You collect rent (premiums) while still owning the property (your shares). The IRS sees this as one integrated transaction, not two separate events.

The good news is, the premiums you receive are usually treated as capital gains, not ordinary income. This shift, solidified back in the 1980s, is a big win for options traders. Why? Because capital gains are often taxed at a lower rate than ordinary income, especially if held long-term. This means you potentially keep more of your profits. Instead of keeping just 60%, you might keep 80%. This is a significant difference. You might be interested in learning more about the Covered Call Strategy.

Key Tax Implications of Covered Calls

Knowing when a taxable event occurs is crucial. Let's break it down:

Expiration: If the option expires worthless (the renter doesn't buy your stock), the premium is a short-term capital gain, no matter how long you've held the underlying stock.

Assignment: If the option is exercised (the renter buys your stock), the premium gets added to the stock's sale price. The tax treatment then depends on how long you held the stock—short-term or long-term.

Since the 1980s, this favorable capital gains treatment for covered call premiums has become a cornerstone of options strategies. As options trading grew between 1984 and the early 2000s, tax authorities clarified the rules around short-term and long-term capital gains for options income. In the U.S., profits or losses from covered calls have consistently been treated as capital gains, not ordinary income. For example, if your covered call expires worthless, the premium is a short-term capital gain, irrespective of how long you held the underlying stock. Discover more insights.

Premium's Impact on Cost Basis

The premium you receive also affects the cost basis of your stock. Think of it this way: the premium you receive effectively increases your cost basis. If your shares are assigned, this higher cost basis will reduce your taxable gain (or increase your loss) when you sell.

To understand this better, let's look at a few examples:

Let's illustrate these scenarios with a table:

Covered Call Tax Events and Their Treatment

A comparison of different covered call scenarios and their corresponding tax implications

| Scenario | Tax Treatment | Timing of Recognition | Rate Applied |

|---|---|---|---|

| Option Expires Worthless | Short-Term Capital Gain | Upon Expiration | Short-Term Capital Gains Rate |

| Option Exercised (Shares Held < 1 Year) | Short-Term Capital Gain (Premium + Stock Sale Profit) | Upon Assignment | Short-Term Capital Gains Rate |

| Option Exercised (Shares Held > 1 Year) | Long-Term Capital Gain (Premium + Stock Sale Profit) | Upon Assignment | Long-Term Capital Gains Rate |

As you can see, understanding how premiums influence your cost basis is key. It reinforces the idea that covered call taxation isn't about isolated events but about understanding the integrated nature of the transaction. It's not just about generating income; it's about using covered calls strategically within a larger tax-efficient investment plan.

How Strike Price Choices Impact Your Tax Situation

Your strike price isn't just a number you pick out of a hat. It's a key factor that influences how your covered calls are taxed. Think of it like setting the temperature on your oven – different temperatures yield different results. Similarly, choosing different strike prices will bake up different tax consequences. Understanding how they work together is crucial for getting the most out of your returns.

At-The-Money and Out-Of-The-Money Calls

When you write at-the-money or out-of-the-money covered calls, you're essentially letting the clock keep ticking on your stock's holding period. This can be a huge win for securing those desirable long-term capital gains rates. Imagine you've held a stock for almost a year, say 11 months. Writing an at-the-money call lets you hit that one-year mark and potentially unlock some serious tax savings. It’s like crossing the finish line of a marathon and collecting your medal.

In-The-Money Calls: The Holding Period Pause

Now, let's flip the script and look at in-the-money covered calls. Here, the holding period of your underlying stock usually takes a breather while the call option is active. Picture hitting the pause button on a stopwatch. While that call is open, the clock stops ticking towards those valuable long-term capital gains. This can be a real setback, particularly if you're close to the one-year milestone. Imagine owning that same 11-month stock, writing an in-the-money call, and having the clock reset—delaying your long-term gains even further.

For example, back in 1988, the IRS clarified that writing at-the-money or out-of-the-money covered calls doesn't reset the holding period of your stock. This helps you stay on track for those beneficial long-term capital gains rates. However, with an in-the-money covered call, the holding period typically pauses. This distinction is particularly important for investors earning $100,000 or more annually. The difference between short-term (up to 37% in the U.S. in 2024) and long-term capital gains rates (0–20%) can be massive, potentially saving thousands of dollars each year. Learn more about covered call tax treatment here.

Strategic Strike Price Selection for Tax Optimization

The bottom line? Choosing a strike price isn't just about getting the biggest premium; it's a strategic tax move. Smart investors use their strike price decisions to carefully manage their holding periods, making sure they grab those long-term capital gains benefits whenever they can. They know that a small difference in the strike price can have a big impact on their total tax bill. This strategic approach sets them apart from investors who are just chasing premiums without thinking about the bigger tax picture. By carefully considering the tax implications of each strike price, they can seriously improve their after-tax returns. This proactive approach to taxes is a crucial part of successful covered call writing.

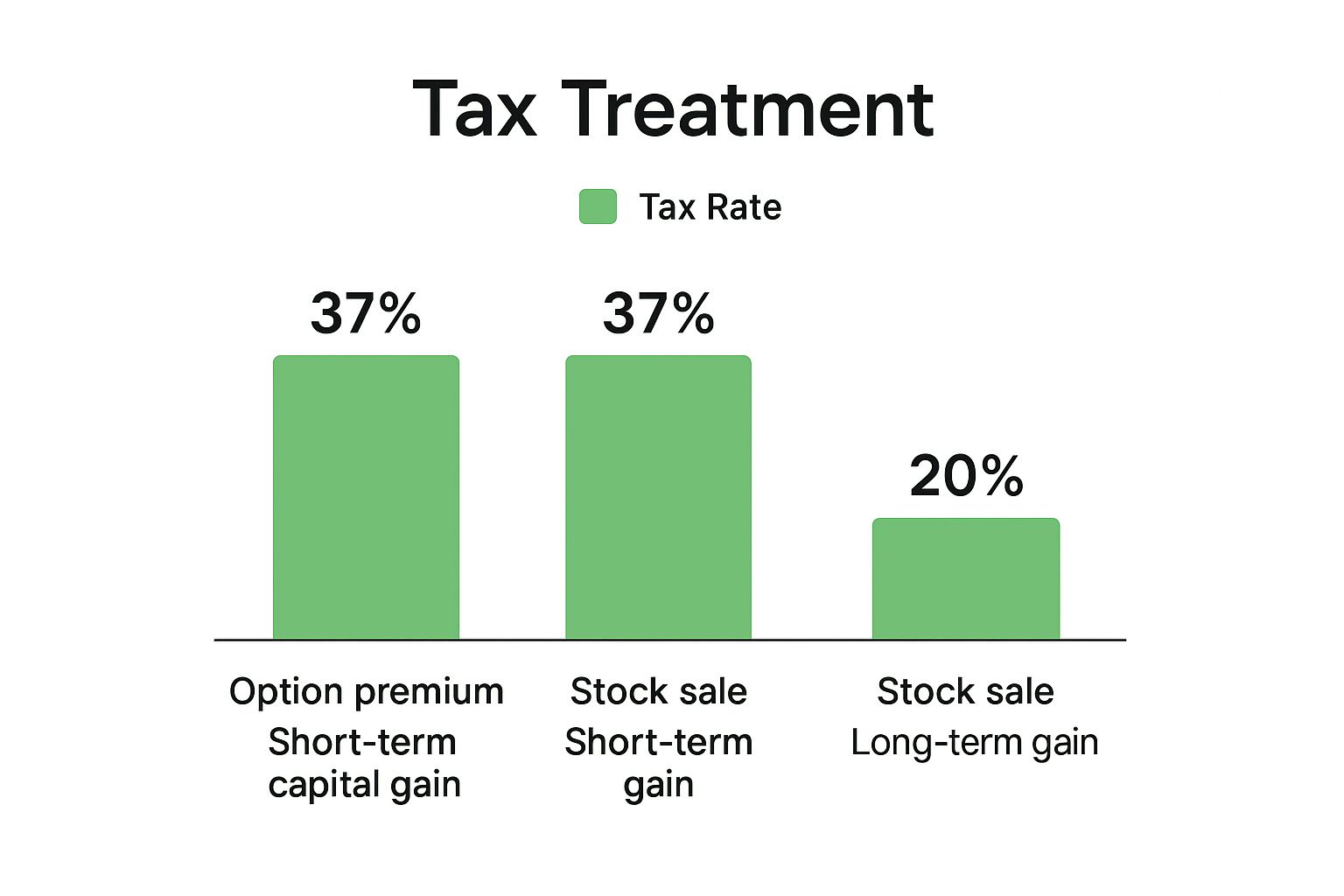

Covered Call ETFs Versus Direct Writing: Tax Reality Check

The infographic above illustrates the tax rates on different covered call scenarios, emphasizing the potential benefits of long-term capital gains. Long-term gains offer a sweeter deal compared to their short-term counterparts or ordinary income. This makes timing a crucial ingredient in the covered call recipe. While covered call ETFs seem convenient, their tax treatment can differ significantly from writing calls directly, potentially impacting your bottom line. Think of it like choosing between a pre-made sandwich and making one yourself. The pre-made option (ETF) is quick, but you lose control over the specifics (tax treatment).

While the simplicity of covered call ETFs is attractive, many investors overlook the tax implications until tax season rolls around. It's similar to buying something online that seems inexpensive, only to be surprised by hidden shipping costs at checkout. With ETFs, the fund manager is writing the calls for you, and the distributions you receive are often taxed as ordinary income. This could mean paying 17% more in taxes compared to writing calls directly and qualifying for lower capital gains rates.

Covered call ETFs, which gained traction in the 2010s, have made understanding tax treatment more critical than ever. By February 2025, the Global X Nasdaq 100 Covered Call ETF (QYLD) held over $7 billion in assets, showing just how popular this approach has become. Find more details on covered call ETFs and taxes here. Despite the general tax advantages of ETFs, covered call strategies within them add a layer of complexity. In the U.S., these ETFs often distribute 90% or more of their income as ordinary dividends, usually taxed at rates up to 37%, while call premiums are taxed at the capital gains rate. This often means 70-80% of distributions are subject to ordinary income tax, reducing your after-tax yield.

Analyzing Real-World Fund Performance and Tax Distributions

Let's illustrate this difference with a hypothetical scenario. Imagine two investors, each targeting a 5% yield. Investor A uses a covered call ETF and their entire distribution is taxed as ordinary income at 37%. Investor B writes calls directly, enjoying a 20% long-term capital gains rate on premiums. After taxes, Investor A’s 5% yield dwindles to about 3.15%, while Investor B keeps a much healthier 4%. Over time, this seemingly small gap can make a significant difference.

Weighing Convenience Against Tax Disadvantages

So, when are covered call ETFs a good choice? They can be suitable for smaller accounts where commission costs for writing individual calls outweigh the tax benefits, or for investors who prefer simplicity and accept the tax trade-off. It's a balancing act between convenience and tax efficiency. A new investor with a small account might appreciate the ease of an ETF, while a seasoned trader with substantial capital might prefer direct writing for the tax advantages.

To further illustrate the key tax differences, let's look at a comparison table:

Direct Covered Calls vs. Covered Call ETFs Tax Comparison: Side-by-side analysis of tax implications for direct covered call writing versus covered call ETF investing

| Investment Method | Tax Rate on Premiums | Tax Rate on Distributions | After-Tax Yield Impact | Complexity Level |

|---|---|---|---|---|

| Direct Covered Calls | Capital Gains Rate (e.g., 20%) | Varies; potential for long-term capital gains | Higher potential after-tax yield | Higher |

| Covered Call ETFs | Capital Gains Rate (e.g., 20%) | Primarily Ordinary Income Rate (e.g., 37%) | Lower potential after-tax yield | Lower |

This table highlights how the different tax treatments impact after-tax returns. Direct writing offers a higher potential after-tax yield due to the potential for long-term capital gains treatment on premiums. ETFs, while simpler, generally lead to lower after-tax yields because distributions are taxed as ordinary income.

Optimizing Your Strategy

The best strategy depends on your circumstances. For investors in higher tax brackets or with larger accounts, actively managing covered calls yourself might maximize after-tax returns. Using tax-advantaged accounts like IRAs can further enhance your strategy. These accounts offer tax-deferred growth for your covered call premiums, shielding them from immediate taxation, which is particularly beneficial for long-term strategies. Considering your individual situation, account types, and risk tolerance will help you craft a strategy aligned with your financial goals and tax situation.

Walking Through Real Covered Call Tax Scenarios

Real-world examples are often the best teachers, especially when it comes to something as potentially tricky as taxes on covered calls. So, let's dive into a few scenarios that mirror what many investors face, complete with calculations and strategic insights.

Scenario 1: Sarah's Tech Stock Tango

Sarah decided to write covered calls on some tech stocks she owned. She'd held these stocks for over a year, hoping to benefit from the lower tax rates associated with long-term capital gains. She wrote calls that were set to expire in December and received $500 in premiums. The options eventually expired worthless. This meant Sarah kept the $500, but it was taxed as a short-term gain, even though she’d held the underlying stock long-term. This little wrinkle impacted her year-end tax planning and reminded her that the expiration timing of her options is just as important as how long she holds the underlying stock.

Scenario 2: Mike's Early Assignment Experience

Mike liked writing covered calls on dividend-paying stocks. He held his shares for nine months before writing slightly in-the-money calls to grab a higher premium. Unfortunately, the stock price unexpectedly jumped, and his calls were assigned early. This forced Mike to sell his shares sooner than he’d planned, impacting his dividend income and resetting the clock on his holding period. This taught Mike a valuable lesson about the importance of strike price selection, especially with dividend-paying stocks. Early assignment can really disrupt income streams and throw off long-term gain strategies.

Scenario 3: The Retiree and the Tax Bracket

Imagine a retiree looking to supplement their income with covered calls, but also wanting to stay within a specific tax bracket. They wrote at-the-money calls expiring monthly, generating $200 in premiums each time. By carefully managing this extra income, they successfully stayed within their desired tax bracket. This shows how covered calls can be a useful tool for targeted tax management during retirement, allowing you to boost your income without getting bumped into a higher tax liability.

Scenario 4: The High Earner and Medicare Tax

Let's say a high-earner wrote covered calls on a large block of stock. The premiums they received were substantial, but this extra income triggered additional Medicare taxes. This highlights how covered call income, while often taxed favorably as capital gains, can still impact other tax calculations. For high earners especially, comprehensive tax planning is crucial, considering not just income tax but also related taxes like those for Medicare.

These scenarios highlight how different market outcomes can influence the tax implications of covered calls. Whether you're managing retirement income, aiming for long-term gains, or navigating higher tax brackets, understanding these practical applications is key for strategic covered call writing. By thinking through these real-world examples, you can anticipate potential tax consequences and make informed decisions that align with your financial goals. Planning ahead lets you shift from reacting to market events to proactively managing your investments for the best possible after-tax returns.

Strategic Tax Timing With Your Covered Calls

Smart covered call investors don't just trade; they orchestrate. They see the bigger picture, weaving their options activity into their overall financial plan. Think of it like a conductor leading an orchestra – each instrument (investment strategy) contributes to a harmonious whole (maximized after-tax returns). This isn't about arcane loopholes, but understanding how covered calls interact with the rest of your financial life.

Coordinating Covered Calls with Tax-Loss Harvesting

Savvy investors often use covered calls as part of a tax-loss harvesting strategy. Let's say a stock in your portfolio is down 20%. Selling it creates a capital loss, which can offset gains from your covered call premiums. This reduces your overall tax bill, essentially letting you use your losses to soften the blow of your gains.

Timing Option Expirations to Manage Tax Brackets

The timing of your option expirations plays a crucial role in managing your tax bracket. By controlling when your premiums become income, you can influence which bracket you fall into. Imagine you're on the cusp of a higher tax bracket. Letting some calls expire the following year defers the income, potentially keeping you in the lower bracket.

Coordinating with Other Portfolio Activities

Covered calls fit neatly into other portfolio activities like portfolio rebalancing. If you need to sell appreciated assets, writing covered calls generates extra income while you wait for the optimal selling window. Think about it as getting paid while you prepare to sell. This also works well with retirement contributions and charitable giving. Covered call income can offset the tax hit from Roth conversions or even help fund charitable donations.

Integrating Covered Calls with Life Events

Life throws curveballs – marriage, divorce, retirement. These events significantly impact your taxes. Smart investors adapt their covered call strategies accordingly. Approaching retirement? You might shift to longer-term covered calls to maximize qualified dividends and minimize short-term gains. For a deeper dive into implementing covered calls, check out our guide.

Bunching Income Strategically

Some investors use a technique called bunching income. This involves concentrating income into specific years to maximize deductions or credits. Covered calls give you control over when you realize your premiums. You can strategically bunch them into years with higher deductions, effectively using those deductions to offset the extra income.

Managing the Timing of Assignments

When your calls are assigned, the premium gets added to your stock's sale price, impacting your capital gain or loss. Understanding the timing and mechanics of assignments is crucial for anticipating the tax consequences. It's like factoring in the delivery fee when calculating the total cost of an online purchase.

Utilizing Different Account Types

Holding your investments in different account types – tax-deferred or tax-exempt – significantly changes the tax treatment of your covered calls. For example, writing calls within a Roth IRA lets your premiums grow tax-free. This is especially powerful for long-term investors.

By viewing covered calls as a piece of a larger tax strategy, you can significantly boost your after-tax returns. It requires planning and coordination, but the potential benefits make it a worthwhile endeavor.

Staying Organized Through Tax Season And Beyond

Imagine building a financial fortress, brick by brick. Each transaction, each record, strengthens your defenses. That's the power of meticulous record-keeping, especially when it comes to the sometimes surprising tax implications of covered calls. Even the best strategies crumble without it. Covered call transactions can trigger more taxable events than many investors realize initially, so being prepared is key.

Essential Record-Keeping Practices

Successful covered call investors get it. They know a solid tracking system is crucial. This isn't just about shoving receipts in a shoebox; it’s about diligently tracking premiums received, noting those key assignment dates, and keeping tabs on adjustments to your cost basis.

Let's say you write a covered call and receive a $100 premium. That premium actually increases the cost basis of the underlying shares. Later, if those shares are assigned, this adjusted cost basis will directly impact your final capital gain or loss calculation. Details like this might seem small at the time, but they become crucial pieces of the puzzle when tax season rolls around.

Here are some essential records to keep safe and sound:

- Option Contracts: Keep copies of every single option contract. Note the strike price, the expiration date, and that all-important premium received.

- Trade Confirmations: Think of these as your receipts. They verify the execution of your trades, with details like date, price, and quantity.

- Assignment Notices: If your covered calls get exercised, hold onto these notices. They’re proof of the transaction.

- 1099-B Forms: Your broker will send these, reporting your proceeds from transactions, including covered call premiums and stock sales.

- Cost Basis Records: Maintain accurate records of the original cost basis for every stock you own, adjusting it to reflect those premiums received.

Digital Tools for Automated Tracking

Thankfully, we live in an age of automation. Many brokerage platforms offer digital tools and software that handle a lot of the record-keeping heavy lifting for you. These tools can track your transactions, calculate those cost basis adjustments, and even generate helpful tax reports. Think of it as a digital filing cabinet, keeping everything organized and easily accessible. This not only saves you time but also minimizes the risk of errors that could cause trouble later.

Learning from IRS Inquiries

Sometimes, the best lessons come from others' experiences. Talking to investors who have faced IRS scrutiny reveals some common pitfalls. Incomplete records and discrepancies between reported income and actual transactions are often at the heart of the issue. Imagine meticulously tracking your premiums but forgetting to document a cost basis adjustment. A small oversight like that could raise questions and even lead to an audit.

Working Effectively with Tax Professionals

Finally, a tax professional who understands options strategies is like gold. Make sure your preparer has the expertise to handle the complexities of covered calls and optimize your tax returns. Their guidance ensures you're taking all applicable deductions and minimizing your tax liability. A qualified professional can translate the often confusing world of covered call tax treatment into a clear, actionable plan. They can also provide insight into tax law changes and strategic planning opportunities. This proactive approach transforms tax season from a stressful ordeal into a confident review of your smart financial decisions.

Your Covered Call Tax Action Plan and Next Steps

Now that we've untangled the tax implications of covered calls, let's map out a practical plan. This isn't about preparing for every imaginable scenario; it's about giving you clear, actionable steps aligned with your experience and goals.

Evaluating Covered Call Opportunities Through a Tax Lens

Think of this as your pre-flight check. Before writing any covered call, consider these points:

What's my holding period? Holding a stock for over a year unlocks those desirable long-term capital gains rates. Your strike price choice directly affects this.

What's my strike price? An in-the-money call might offer higher premiums now, but could postpone your long-term capital gains if assigned. Is that trade-off worth it?

When does the option expire? Even if you hold the underlying stock long term, a worthless expiring option means the premium is taxed as a short-term gain.

Recognizing Warning Signs and Adjusting Your Strategy

Sometimes, your covered call strategy needs a tune-up. Here are some potential trouble spots:

Early assignment risk: Are your calls assigned early often? This disrupts your income and resets holding periods. Rethink your strike price choices.

Unexpected tax implications: Did your covered call income bump you into a higher tax bracket or trigger extra Medicare tax? Adjust your strategy or talk to a tax professional.

Poor record keeping: Are you struggling to track premiums, assignments, and cost basis adjustments? Staying organized is crucial. Check out these compliance strategies to avoid tax penalties.

Measuring Your After-Tax Success Over Time

Don't just track your premiums; track your after-tax premiums. This is the true measure of your success. Factor in your tax bracket to calculate your effective after-tax yield. Are you hitting your income goals without sacrificing long-term capital gains?

When to Seek Professional Advice

Covered calls can get complicated, particularly when combined with other investment strategies. Talk to a tax advisor if:

- You're unsure about the tax implications of a specific strategy.

- You're using covered calls within a complex tax plan (like tax-loss harvesting).

- You're facing unexpected tax consequences.

Integrating Covered Call Tax Planning into Your Broader Approach

Think big picture. Coordinate your covered call activity with other financial moves, like retirement contributions, charitable giving, and portfolio rebalancing. Timing is key. Consider using different account types (like IRAs) to maximize tax advantages. For ideas on maximizing income with options, explore the best options strategy for income.

Staying Current with Tax Law Changes

Tax laws change. Stay informed about anything that could affect your covered call strategy. Subscribe to relevant publications, attend webinars, or regularly connect with a tax professional.

By using this action plan, you can confidently handle the tax complexities of covered calls and boost your after-tax returns. You'll gain control, making informed decisions based on clear, actionable steps.

Ready to move your options trading from guesswork to a strategic, income-generating process? Strike Price, our subscription platform, gives you data-driven probabilities and real-time insights for covered calls and secured puts. Discover how Strike Price can help you maximize your premium income.