What Is Delta in Options Trading Explained Simply

If a stock moves past your strike, the option can be assigned — meaning you'll have to sell (in a call) or buy (in a put). Knowing the assignment probability ahead of time is key to managing risk.

Posted by

Related reading

A Step-by-Step Covered Calls Example for Consistent Income

Unlock consistent income with our step-by-step covered calls example. This guide breaks down the strategy, risks, and outcomes to help you trade confidently.

Long Call and Short Put The Ultimate Synthetic Stock Guide

Unlock the power of the long call and short put strategy. This guide explains how synthetic long stock works, its benefits, risks, and how to execute it.

What is a Call Spread? A Clear Guide to Bull and Bear Spreads

What is a call spread? Discover how bull and bear spreads limit risk and sharpen your options trading strategy.

When you're trading options, if there’s one metric you absolutely have to understand, it’s delta. Think of it as the speedometer for your option’s price. It tells you pretty much exactly how much its value should change for every $1 move in the underlying stock. Grasping this concept is fundamental, as it's directly tied to your risk and potential profit.

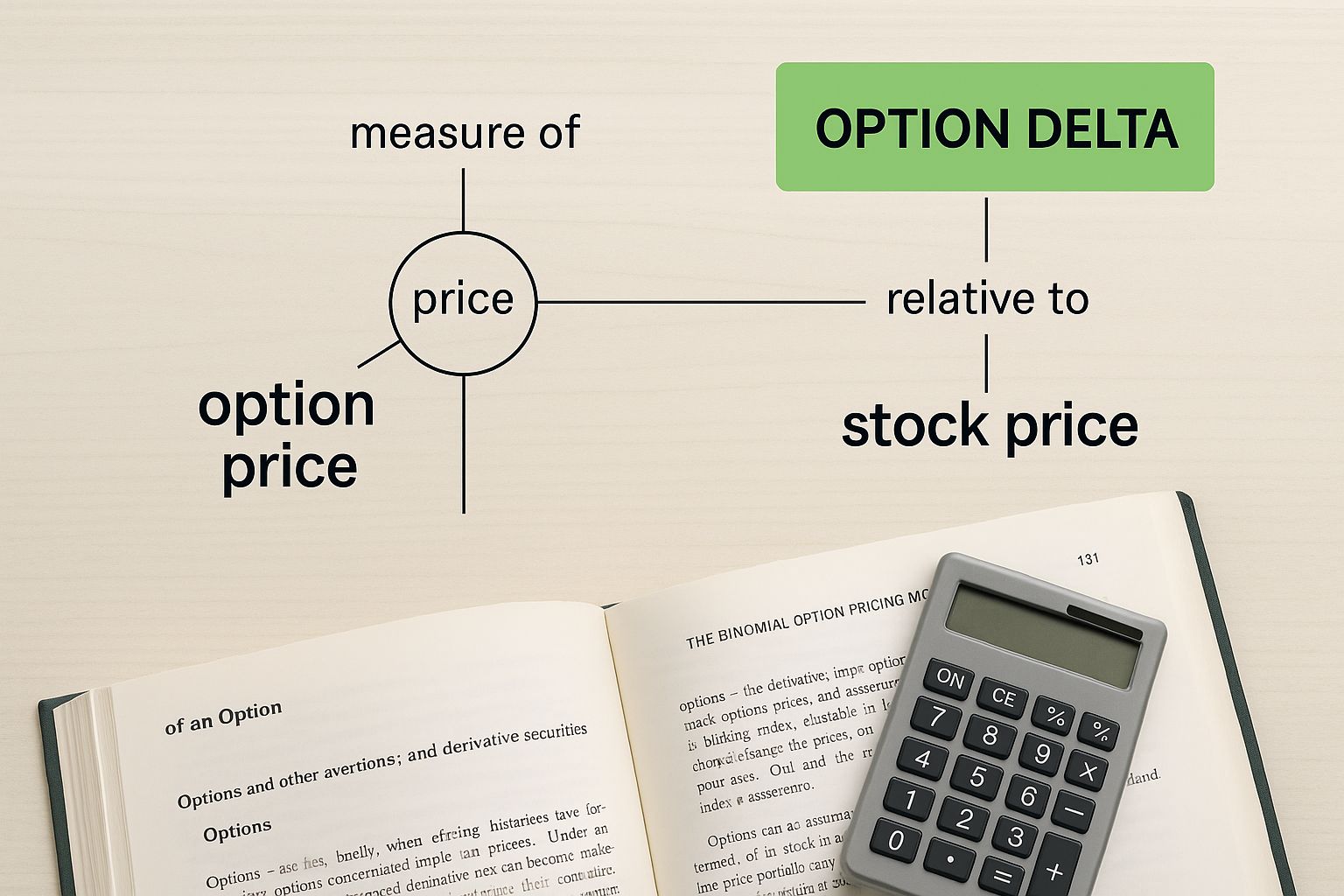

Understanding Option Delta in Plain English

Delta is one of the "Option Greeks"—a handful of key metrics that help traders figure out the risks and rewards of a trade. While the name might sound a little intimidating, delta's job is actually pretty straightforward. If you want to dive deeper into all of them, check out our full guide on what are the Option Greeks.

This infographic breaks down what delta is and what it does in a really simple, visual way.

As you can see, delta is the bridge connecting an option's price to the stock's price, giving you a quick read on both its sensitivity and its probability of success.

Delta’s Two Main Jobs

So, what does delta really do? It has two critical functions that every options trader needs to know inside and out.

First, delta tells you how sensitive an option's price is to a $1 change in the stock price.

It’s that simple. If you have a call option with a delta of 0.30, you can expect its price to go up by about $0.30 if the stock climbs by $1. On the flip side, it would lose $0.30 if the stock dropped by $1.

Second, and this is where it gets really useful for sellers, delta gives you a rough probability of the option expiring in-the-money (ITM).

Key Takeaway: A call option with a 0.40 delta has roughly a 40% chance of finishing in-the-money. That makes delta an incredibly powerful, at-a-glance tool for sizing up the risk of any trade you’re considering.

Understanding this dual role is your first step to using delta like a pro. It's not just some abstract number; it's a dynamic gauge that measures your directional exposure and your trade's odds of success. It’s what helps you move from just guessing to making strategic, data-driven decisions.

Call vs Put Delta at a Glance

To make this even clearer, it helps to see how delta behaves for both call and put options. They're essentially mirror images of each other.

This quick table breaks down the core differences.

| Attribute | Call Options | Put Options |

|---|---|---|

| Value Range | 0 to +1.0 | 0 to -1.0 |

| Stock Price Up | Delta increases | Delta decreases (moves closer to 0) |

| Stock Price Down | Delta decreases | Delta increases (moves closer to -1.0) |

| Meaning | Positive delta shows a direct relationship to the stock price. | Negative delta shows an inverse relationship to the stock price. |

As you can see, call deltas are always positive because their value moves with the stock price. Put deltas are always negative because their value moves against the stock price. This simple distinction is the bedrock of understanding how to use delta to your advantage.

How Delta Translates to Real-World Gains and Losses

Theory is great, but let's connect delta to what really matters: your bottom line. At its core, delta shows you exactly how much your option's value will change for every dollar the underlying stock moves. It’s the bridge between a stock’s price action and your P&L.

For call options, a positive delta means your position profits as the stock price climbs. Simple enough. For put options, a negative delta means you make money when the stock price drops. This direct relationship is what lets you place clear, calculated bets based on where you think the market is headed.

But the real game-changer is thinking of delta as a stock equivalent. It’s how you can control the directional exposure of hundreds of shares with just a fraction of the capital.

Calculating Your Share Equivalent

This is where you see the leverage of options in action, without the hefty price tag of owning stock outright. Let's walk through a quick example.

Say you think XYZ stock, currently trading at $50, is about to rally. Instead of buying 600 shares — which would cost you a cool $30,000 — you decide to use options to make the same bet.

You buy 10 call option contracts, each with a delta of 0.60. Since every options contract represents 100 shares, the math to find your total directional exposure is straightforward:

Share Equivalent = Number of Contracts x 100 Shares/Contract x Delta

Let’s plug in our numbers:

10 Contracts x 100 Shares/Contract x 0.60 Delta = 600 Share Equivalent

What this means is that for every $1 increase in XYZ stock, your options position will gain approximately $600. That’s the exact same profit you would have made from owning 600 shares directly.

You’ve just made the same directional bet for a tiny fraction of the upfront cost. This is why getting a handle on delta is so crucial for managing your capital efficiently.

Using Delta as a Probability Gauge

Beyond telling you how an option's price might move, delta has another trick up its sleeve that experienced traders rely on. Think of it as a quick, back-of-the-napkin probability calculator. It gives you an immediate estimate of an option's chances of expiring in-the-money (ITM), turning a complicated forecast into a simple number you can glance at.

For example, if you see a call option with a delta of 0.40, you can read that as having roughly a 40% chance of finishing ITM by its expiration date. No, it's not a crystal ball, but it's an incredibly useful estimate for sizing up the risk and reward of a trade before you pull the trigger.

This isn't just a trader's rule of thumb; it's a concept backed by market data. Delta serves as a reliable proxy for an option's probability of expiring ITM. The Chicago Mercantile Exchange (CME) even notes that a delta value can be read as the approximate chance of an option expiring with some value. So, an option with a 0.20 delta is priced as having about a 20% shot of ending in the money.

Applying Probability to Your Strategy

This insight is a complete game-changer when it comes to picking a strategy. It lets you match your trades directly to how you see the market and how much risk you're willing to take on.

For Premium Sellers: If your goal is to generate income, you’ll often sell out-of-the-money options with a low delta—say, 0.20 or less. You're essentially placing a high-probability bet that the option will expire worthless, letting you pocket the entire premium.

For Directional Buyers: On the other hand, if you're confident a stock is about to make a big move, you might buy a higher-delta option, like 0.60 or more. You're accepting a lower chance of success in exchange for a much bigger potential payout if you're right.

Key Insight: Using delta as a probability gauge helps you stop guessing and start making strategic decisions based on quantifiable odds.

It's a similar principle to risk and probability assessment in other markets such as cricket betting. Whether you're trading options or analyzing sports, understanding the probabilities is the foundation for making smarter, more informed decisions.

Why Your Option's Delta Is Never Static

One of the biggest mistakes new traders make is thinking delta is a set-it-and-forget-it number. You might sell a put with a 0.40 delta today, but that value is almost guaranteed to be different tomorrow. It’s constantly in motion, reacting to the market in real-time.

Several forces are always at play, pushing and pulling on your option’s delta. The most powerful of these is a related Greek known as gamma.

Think of it like this: if delta is your car's speed, gamma is its acceleration.

Key Concept: Gamma measures how fast an option's delta changes for every $1 move in the underlying stock. High gamma means your delta will change very quickly as the stock price moves. Low gamma means it will change more slowly.

The Role of Gamma, Time, and Fear

Gamma has the most dramatic effect on options that are at-the-money (ATM). These options have the highest gamma, which makes their deltas incredibly sensitive to even small shifts in the stock's price. An ATM option can see its delta swing from 0.50 to 0.70 in a hurry if the stock rallies, rapidly increasing your directional exposure.

But gamma isn’t the only factor. Two other Greeks also have a say:

- Theta (Time Decay): As time passes and an option gets closer to expiration, its delta tends to move toward either 0 or 1.0. For out-of-the-money options, delta shrinks toward zero every single day.

- Vega (Volatility): A big spike in market fear—what we call implied volatility—can also mess with an option's delta. It generally pushes the deltas of out-of-the-money options higher.

This is exactly why you can't just set a trade and walk away. Your position's risk profile isn't static; it evolves with every tick of the stock price and every passing day. If you ignore these changes, you’re flying blind to your true market exposure.

Putting Delta to Work in Your Trading Strategies

Alright, enough with the theory. Let's get into how delta actually makes you a smarter trader. Think of delta not just as a number on a screen, but as a tool you can actively use to build positions, manage your risk, and bend your portfolio to your will.

One of the most powerful ways traders do this is with delta hedging. At its core, this is just a fancy way of saying you're trying to neutralize your exposure to the market's daily whims, creating a position that doesn't really care if the stock goes up or down.

Hedging a Stock Portfolio

Let’s make this real. Say you own 1,000 shares of XYZ stock. Right now, your position has a delta of +1000. You're long and loving it, but you're getting a little nervous about a potential dip. You don't want to sell your shares, but you want some protection.

This is where put options come in. To cancel out your bullish risk, you can buy some puts to create an opposing negative delta. For example, you could buy 20 put option contracts, each with a delta of -0.50. Let's do the math:

1,000 shares (Delta: +1000) + 20 put contracts x -50 Delta/contract (Delta: -1000) = A perfect net delta of 0

Just like that, your portfolio is now delta-neutral. A small drop in XYZ's stock price will sting less because it's cushioned by a corresponding gain in your put options. It's a classic move used by big-money investors to protect their holdings from short-term bumps without having to liquidate.

Building Delta-Neutral Strategies

You don't just have to use delta for defense. You can build entire trading strategies that are delta-neutral from the very beginning. These trades aren't about betting on which way the market will go; they’re designed to make money from other factors, like the relentless march of time (theta decay) or shifts in market fear (vega).

A textbook example is the iron condor. This strategy involves selling an out-of-the-money put spread and an out-of-the-money call spread at the same time. The goal? For the stock to just... do nothing. You want it to stay trapped within a specific price range until expiration, letting all the options you sold expire worthless.

By combining positive and negative deltas right from the start, you construct a position with a net delta hovering around zero. As long as the market doesn't make any crazy moves, you can just sit back and profit from time decay. Getting a grip on how time eats away at an option's value is huge for these strategies, and you can dig deeper into how to calculate option premium to see exactly how it works.

Common Delta Mistakes That Cost Traders Money

Knowing what delta is gets you in the game. But avoiding the common traps is what helps you win it. Falling for these myths is a fast way to let expensive errors quietly drain your account.

One of the most dangerous beliefs is that delta is a static, set-it-and-forget-it number. It’s not. As we've seen, your position's delta is always in motion, reacting to every price tick (gamma), the passing of time (theta), and shifts in market fear (vega). If you ignore this dynamic, you’re flying blind to your true directional risk.

Another costly mistake is thinking a 0.50 delta automatically means a 50% chance of profit.

This is a critical distinction: A 0.50 delta suggests a roughly 50% chance of the option expiring in-the-money, but it says nothing about profitability. Your actual breakeven point is always the strike price plus or minus the premium you paid or collected.

Ignoring The Other Greeks

Finally, so many traders get tunnel vision and convince themselves delta is the only Greek that matters. That’s a shortcut to disaster.

Focusing only on delta while ignoring its rate of change (gamma) can expose you to sudden, explosive risk—especially as expiration gets closer. Likewise, overlooking time decay (theta) is like having a slow leak in your portfolio. Eventually, it causes real damage.

A holistic view is non-negotiable for real success. To build a more resilient trading approach, you have to integrate all these concepts into a broader framework. You can learn more about creating one in our complete guide to options risk management. Properly managing all the Greeks is what turns a speculative bet into a calculated strategy.

Your Questions About Delta, Answered

As you get more comfortable with delta, a few common questions always pop up. Getting these sorted out is key to really cementing the concept in your mind. Let's run through them.

Can Delta Go Higher Than 1 or Lower Than -1?

Nope. For a standard, single option, delta is always locked within a specific range.

Call options will always have a delta between 0 and +1.0. Put options stay between 0 and -1.0. A delta of exactly 1.0 is the ceiling—it means the option is moving dollar-for-dollar with the stock, almost as if you were holding 100 shares yourself.

What's Considered a High or Low Delta?

Good question. It's a bit relative, but traders generally follow a few rules of thumb.

High Delta: Anything above 0.70 on a call or below -0.70 on a put is considered high. These are typically deep in-the-money options that have a very strong, almost one-to-one relationship with the stock's price.

Low Delta: A delta under 0.30 for calls (or above -0.30 for puts) is considered low. This is the territory of out-of-the-money options, where the connection to the stock's daily moves is much weaker.

And if you're wondering about your overall portfolio, its total delta is just the sum of all the individual deltas from every position you hold, stocks and options combined.

Ready to stop guessing and start making data-driven trades? Strike Price provides real-time probability metrics for every strike price, turning complex data into clear, actionable insights for options sellers. Sign up and trade smarter today at https://strikeprice.app.