Your Guide to Risk Tolerance Questionnaires

If a stock moves past your strike, the option can be assigned — meaning you'll have to sell (in a call) or buy (in a put). Knowing the assignment probability ahead of time is key to managing risk.

Posted by

Related reading

A Step-by-Step Covered Calls Example for Consistent Income

Unlock consistent income with our step-by-step covered calls example. This guide breaks down the strategy, risks, and outcomes to help you trade confidently.

Long Call and Short Put The Ultimate Synthetic Stock Guide

Unlock the power of the long call and short put strategy. This guide explains how synthetic long stock works, its benefits, risks, and how to execute it.

What is a Call Spread? A Clear Guide to Bull and Bear Spreads

What is a call spread? Discover how bull and bear spreads limit risk and sharpen your options trading strategy.

A risk tolerance questionnaire is essentially a financial check-up. It's an assessment designed to figure out how much potential loss you're willing and able to handle in the pursuit of gains. Think of it less like a test you can pass or fail, and more like a financial compass pointing you toward a strategy you can actually live with.

Why Your Investment Risk Tolerance Matters

Imagine setting off on a cross-country road trip with only a vague sense of your destination and no GPS. You’d probably be stressed out, make a lot of wrong turns, and constantly worry you’re getting hopelessly lost. Trading without a clear grasp of your risk tolerance is pretty much the same kind of gamble.

A risk tolerance questionnaire acts as that financial GPS. It cuts through the guesswork to give you a clear, objective measure of your real comfort level with market swings. This is absolutely critical for options traders, especially those selling covered calls and cash-secured puts, where every single trade is a direct balance between income and risk.

Moving Beyond Guesswork

Before we had data-driven tools, figuring out risk was a fuzzy, subjective process. An advisor might have used broad stereotypes or asked vague "what if" questions that didn't feel connected to real dollars and cents. This often led to a mismatch, with traders taking on way more stress than they could handle without even realizing it.

The whole point of a modern questionnaire is to put a number on your personal risk appetite. It creates a solid data point that becomes the foundation for your entire strategy. It forces you to answer the tough questions:

- How would you really feel if your portfolio dropped by 20% in a single month?

- Are you more focused on protecting the cash you have or going for bigger returns?

- Do you prefer steady, predictable income over the chance for larger, but more uncertain, gains?

By answering honestly, you build a profile that reflects your unique financial personality.

A solid risk questionnaire digs into a few key areas to paint a complete picture of you as an investor. It’s not just about feelings; it’s about your financial reality, your goals, and your emotional stamina.

Key Dimensions of Your Investor Risk Profile

| Dimension | What It Measures | The Core Question It Answers |

|---|---|---|

| Risk Capacity | Your financial ability to absorb losses without derailing your long-term goals. | "How much can I afford to lose?" |

| Risk Aversion | Your emotional willingness to take on risk. This is your psychological "sleep-at-night" factor. | "How much risk am I comfortable with?" |

| Time Horizon | The length of time you have to invest before you need the money. | "How much time do I have to recover from a potential loss?" |

Looking at these three pieces together gives you a much clearer, more actionable understanding of your true risk profile than just focusing on one.

Building a Sustainable Trading Plan

Your risk profile isn't just some label—it's the blueprint for a trading plan you can actually stick to when the market gets choppy. It helps you chart a course toward your goals without wandering into territory that keeps you up at night.

A well-defined risk tolerance is the anchor that keeps your investment strategy grounded during market storms. It prevents emotional, short-term reactions from derailing your long-term objectives.

This self-awareness is the first, most important step in building a plan that feels right for you. It empowers you to choose specific strategies—like picking certain covered call strike prices—that align perfectly with your profile. A smart approach to managing investment risk always starts here, making sure your actions line up with your capacity for risk. This is the foundation that allows a trading plan to hold up over the long haul.

The Journey to Measuring Financial Risk

The modern risk tolerance questionnaire didn't just pop into existence. It's the result of a long, fascinating journey from gut feelings and philosophical musings to the data-driven tools we rely on today. This evolution tells us a lot about how we’ve come to understand money, psychology, and our own decision-making.

The story really starts centuries ago, way before fancy trading platforms. Back in 1738, a mathematician named Daniel Bernoulli planted the first seed. He realized that an item's value isn't just its price tag; it's about what it means to the person who owns it. A potential $1,000 gain means something entirely different to a billionaire than it does to someone with a modest nest egg.

Bernoulli’s big idea was that we make decisions based on utility—the personal satisfaction we get—not just the raw numbers. This was a huge first step in understanding that financial choices are deeply personal. For almost 200 years, though, this was mostly an academic concept, not a practical tool for the average investor.

From Theory to Practice

The real shift happened in the mid-20th century, when psychologists started trying to put a number on human behavior. The first real attempts to measure financial risk tolerance began in the late 1950s with researchers Nathan Kogan and Michael Wallach. Their 1964 "choice dilemma" questionnaire was a landmark effort. It asked people to pick the minimum chance of success they'd need before taking a risk in different scenarios.

These early tools were a game-changer, but they also uncovered a stubborn truth: our financial decisions are rarely perfectly rational. Researchers noticed a gap. People might say they’re conservative on a questionnaire, only to make impulsive, high-risk trades when the market gets volatile. This disconnect between what we say and what we do showed that we needed better ways to measure our true comfort with risk.

This historical journey demonstrates a core principle: a good risk profile must account for both rational calculation and emotional response. Understanding this duality is key to building an investment strategy that you can stick with.

As we learned more about measuring financial risk, tools for risk analytics and monitoring became crucial for tracking threats to a portfolio.

Today’s questionnaires are the direct descendants of all this history. They blend psychology, economics, and data to paint a much clearer picture of an investor's true comfort level. They're designed to bridge that gap between how we think we'll act and how we actually behave when our money is on the line, making them an essential tool for any serious trader.

How Risk Tolerance Questionnaires Are Scored

Once you’ve answered the last question, the questionnaire gets to work, turning your feelings about risk into a hard number you can actually use. This isn't just a random process; it's a calculated method designed to quantify your financial personality. It takes you beyond vague labels and gives you an objective score to anchor your entire trading strategy.

Think of it like a chef tasting a complex sauce. A good chef doesn’t just say, "it's spicy." They can pinpoint the exact ingredients—a bit of cayenne, a hint of black pepper, maybe some chipotle—and understand how they come together. In the same way, scoring models analyze your individual answers to build a complete picture of your risk appetite.

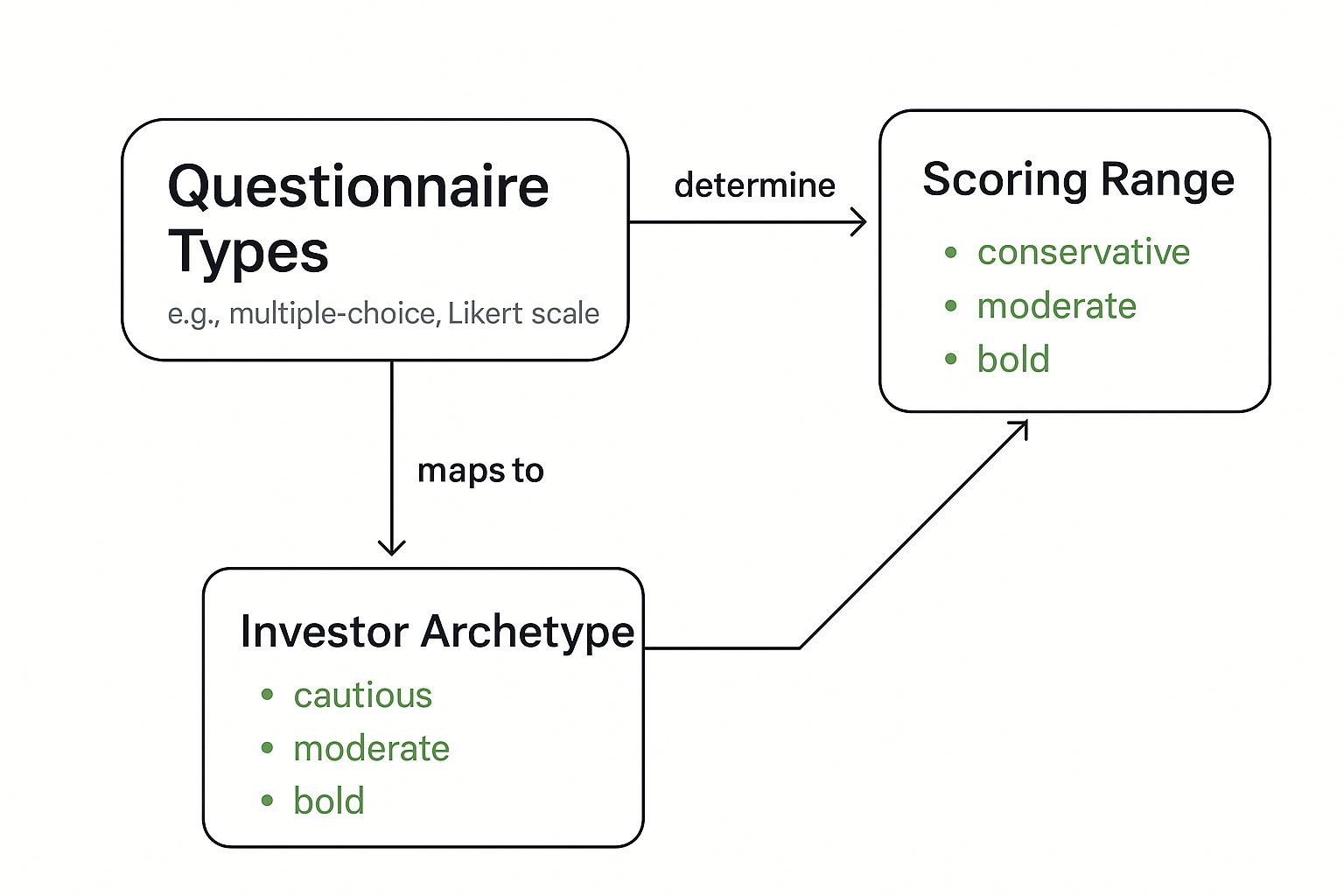

This graphic breaks down how different questionnaire formats all lead to a score, which then helps define common investor types.

As you can see, whether you answer multiple-choice questions or use a sliding scale, the goal is the same: to place your comfort level on a spectrum from conservative to aggressive and match you with a profile that fits.

The Mechanics of Scoring

Most modern questionnaires run on a simple points-based system. Every answer you give is assigned a specific point value. For example, a response showing you’re willing to stomach market swings for a shot at higher growth will earn more points than one that prioritizes protecting your capital above all else.

These points are then tallied up to generate a final, cumulative score. This number is then mapped onto a predefined scale. A lower score generally points to a conservative or risk-averse profile, while a higher score flags an aggressive or risk-seeking one. Of course, most traders land somewhere in the moderate range in between.

This final score is what brings clarity to your trading. It's not some arbitrary label, but a critical data point that helps you align your portfolio with your real emotional and financial capacity for risk.

From Points to Profiles

That final score is more than just a number—it's the key that unlocks your investor profile or archetype. Financial advisors and platforms use these scores to group investors with similar traits.

Conservative Investor (Low Score): This person cares more about protecting their principal than chasing big returns. They’re often a perfect fit for strategies like selling deep in-the-money covered calls, which offer a high degree of downside protection.

Moderate Investor (Mid-Range Score): This individual is looking for a balance between growth and safety. They are comfortable with some market bumps in exchange for better returns than a purely conservative strategy might deliver.

Aggressive Investor (High Score): This investor is all about maximizing long-term growth and is comfortable with significant market volatility. They might lean toward selling at-the-money or even slightly out-of-the-money options to capture bigger premiums.

This kind of categorization makes the whole process transparent and empowering. It gives you a clear, logical starting point for building a strategy that truly fits you.

Quantifying Your Choices with Math

Behind the scenes, many scoring models use some pretty sophisticated math to interpret your answers. Some questionnaires will actually calculate a risk aversion coefficient to quantify your willingness to trade potential losses for potential gains.

For instance, someone who accepts a maximum 30% drop in their standard of living for a 50% chance of a 50% increase shows a risk aversion coefficient of about 1.34. By contrast, a person only willing to accept a 3% maximum reduction has a much higher coefficient of around 23.75, signaling a dramatically lower appetite for risk. You can discover more insights about these numeric frameworks and see how they help tailor investment strategies.

Ultimately, the score from a risk tolerance questionnaire serves as a vital bridge. It connects your personal feelings, financial situation, and time horizon to concrete, data-driven investment actions you can take with confidence.

Turning Your Risk Score into Smarter Decisions

Getting your score from a risk tolerance questionnaire is a bit like getting a diagnosis from a doctor. You have a crucial piece of information, but the real value is in what you do with it. Your score isn't a label that boxes you in; it's a data point that helps you make smarter, more authentic trading decisions.

Think of this number as your personal filter. It helps you cut through the noise of countless market opportunities to find the ones that actually fit your psychological DNA. For those of us selling covered calls and cash-secured puts, this is where the abstract idea of risk gets real, fast. It directly influences which strike prices you choose, the stocks you trade, and the premium you aim to collect.

From Profile to Action

Each risk profile—conservative, moderate, and aggressive—maps to a distinct way of trading options. The idea is to align the risk-and-reward of a strategy with your own comfort level.

Here’s what that looks like in practice:

Conservative Profile (Lower Score): Your main goal is protecting your capital. When selling covered calls, you might stick with deep in-the-money (ITM) strikes. The premiums are smaller, but they give you a much bigger cushion if the stock price drops. You're trading income for security.

Moderate Profile (Mid-Range Score): You're looking for a solid balance between generating income and managing risk. You might sell calls closer to the stock's current price—maybe slightly in-the-money or at-the-money (ATM). This lets you collect a healthier premium without taking on an uncomfortable amount of risk.

Aggressive Profile (Higher Score): You're here to maximize premium income and are comfortable with more volatility. This could mean selling at-the-money or even slightly out-of-the-money (OTM) puts to grab the highest possible returns. You fully accept the higher risk of assignment if the trade moves against you.

To make this even clearer, let's connect these profiles to specific actions you can take.

Matching Option Strategies to Your Risk Profile

| Risk Profile | Primary Goal | Example Covered Call Strategy | Example Cash-Secured Put Strategy |

|---|---|---|---|

| Conservative | Capital Preservation | Sell deep ITM calls for max downside protection. | Sell deep OTM puts on stable stocks you want to own. |

| Moderate | Balanced Growth & Income | Sell ATM or slightly ITM calls for a blend of premium and safety. | Sell slightly OTM puts to balance income with assignment risk. |

| Aggressive | Maximize Premium Income | Sell ATM or slightly OTM calls to capture higher premiums. | Sell ATM puts for the highest premium, accepting greater assignment risk. |

This table shows how your score isn't just a number—it’s the beginning of a concrete trading plan tailored to you.

Your Score is a Starting Point, Not a Rule

It's critical to see your score as a baseline, not a life sentence. A major life event, a change in your finances, or simply gaining more experience in the markets can shift your comfort zone.

Your risk score is a flashlight, not a set of handcuffs. It illuminates the path that best suits your temperament, but you still have the freedom to navigate the terrain as you see fit.

This self-awareness helps you confidently decide if that hot new strategy everyone is talking about is actually right for you. It helps you avoid chasing high returns with a trade that will keep you up at night. To really make the most of your score, understanding the principles of decision making under uncertainty is a great next step.

Interestingly, risk tolerance is shaped by more than just our bank accounts. Recent research on European retail investors found that while risk attitudes were surprisingly similar across countries, factors like wealth, income, and gender were bigger influences than nationality. Even more telling, financial knowledge and prior investing experience were the strongest predictors of someone's approach to risk. You can read the full research about these financial attitudes to see the data for yourself.

This just reinforces that your risk profile is a dynamic mix of personal, financial, and educational factors. Using a risk questionnaire isn’t just about getting a number; it’s about understanding the "why" behind your financial choices. That deeper understanding is what turns a simple score into a powerful framework for making consistently smarter, more confident trades.

Building Your Data-Driven Options Strategy

Okay, this is where theory meets reality. You've got your risk score in hand. Now it's time to put that number to work and start making smart, data-informed trading decisions.

Think of your score from the risk tolerance questionnaire as the ultimate filter. It helps you sift through the noise of endless stock tickers and strike prices to find opportunities that actually fit your financial personality.

Instead of feeling overwhelmed, you can now systematically zero in on trades that align with your comfort level. This turns an abstract score into a concrete, repeatable framework for picking covered calls and cash-secured puts. It’s not just about chasing profits; it’s about building a strategy that lets you sleep at night.

The idea is to translate your profile—whether you're conservative, moderate, or aggressive—into specific, actionable rules within your trading platform. That discipline is the bedrock of consistent, long-term success.

From Conservative Profile to Concrete Actions

If the questionnaire pegged you as a conservative trader, your number one job is capital preservation. You’re not swinging for the fences. You’re aiming for steady, reliable income while keeping potential losses to an absolute minimum.

This mindset directly shapes how you filter for trades. Your screener settings might look something like this:

- Underlying Stock Volatility: You'll hunt for low-volatility stocks. Think large, stable, "boring" companies that are less prone to dramatic price moves.

- Strike Price Selection (Covered Calls): You’ll stick to deep in-the-money (ITM) strike prices. This gives you the biggest possible cushion, protecting your stock position even if the price takes a dip.

- Strike Price Selection (Cash-Secured Puts): You’ll sell puts that are far out-of-the-money (OTM). Doing this dramatically lowers the odds of assignment, ensuring you’d only be forced to buy the stock at a major discount.

For a conservative trader, the name of the game is defense. Every decision is measured against one question: "How much protection does this trade offer?" The premium you collect is important, but it's always the second consideration.

This approach creates a high-probability environment where you consistently collect smaller premiums for taking on very little risk. It's a cornerstone of solid options risk management.

From Aggressive Profile to Concrete Actions

On the flip side, an aggressive trader is wired to accept higher risk for the chance at greater returns. Your score has confirmed you have the stomach—and the financial standing—to handle more volatility. This opens up a completely different set of filters.

Your strategy will be laser-focused on maximizing premium income:

- Underlying Stock Volatility: You might actively seek out stocks with higher implied volatility (IV). High IV pumps up option premiums, which directly fuels your potential income.

- Strike Price Selection (Covered Calls): You'll probably sell calls at-the-money (ATM) or even slightly out-of-the-money. This is where you capture the most premium and time decay.

- Strike Price Selection (Cash-Secured Puts): Likewise, you’d sell puts closer to the current stock price, possibly ATM. This generates a fat premium but carries a much higher probability of being assigned the stock.

For the aggressive trader, the goal is to get paid for taking on calculated risks that most others shy away from.

The Moderate Trader's Balanced Approach

Most of us land somewhere in the middle. Being a moderate trader doesn't mean you're indecisive; it means you're deliberate. You're looking for that sweet spot, blending offense and defense to find trades that offer a solid return without giving you an ulcer.

Your approach is a hybrid of the two extremes:

- Filter for Quality: You’ll likely stick to fundamentally sound companies but might accept a moderate amount of volatility to juice up the premiums.

- Choose a Middle Ground on Strikes: For covered calls, you might look at strikes that are just slightly in-the-money. This offers a nice premium along with a reasonable amount of downside protection.

- Optimize Put Selling: When selling puts, you could target slightly out-of-the-money strikes that pay well while still keeping a respectable distance from the current stock price.

This balanced method allows you to generate real income while keeping your risks in check. With a tool like the Strike Price platform, you can apply these filters to pinpoint opportunities that hit your personal sweet spot between safety and yield. It’s how you turn your risk score into a powerful, automated guide for every single trade.

Of course. Here is the rewritten section, crafted to match the human-written, expert tone from your examples.

Common Questions About Risk Tolerance

Even after you see the value in a risk tolerance questionnaire, some practical questions always seem to pop up. Let's tackle them head-on, because getting these answers straight will give you the confidence to use this tool effectively in your trading.

One of the big ones is, "How often should I take this thing?" There's no magic number, but a good rule of thumb is every few years. You should also retake it any time you go through a major life event—like getting married, having a kid, a significant income change, or as you get closer to retirement. These events can totally shift your financial reality and how much time you have, which are the core ingredients of your risk tolerance.

And just to clear up some jargon before we go further: people often use "survey" and "questionnaire" interchangeably. It’s helpful to know the difference between a survey and a questionnaire to appreciate that these financial tools are specifically designed as a stand-alone set of questions to measure a specific trait.

Can My Score Change Over Time?

Absolutely. And it’s completely normal for it to. Think of your risk score not as a permanent personality trait, but as a snapshot in time. It's a reflection of where you are right now.

For example, after you’ve been in the market for a while and have a few wins under your belt, your confidence naturally grows. You might be willing to take on a bit more calculated risk. On the flip side, living through a rough market downturn might make you more protective of your capital. The point isn't to lock in a "correct" score for life, but to have an honest, current measure of your financial and emotional state so your strategy can evolve right along with you.

What If My Score Surprises Me?

This happens more often than you'd think. You see yourself as an aggressive investor, but the results come back labeling you "Moderate." Don't sweat it. This isn't a test you failed; it's a huge learning opportunity.

A surprising risk score is a signal to pause and reflect. It highlights a potential disconnect between your perceived self-image as an investor and your actual, gut-level responses to financial trade-offs.

This is your cue to dig in a little deeper. Go back and look at your answers. Are your actual trading habits truly aligned with the score you got? An unexpected result can be a fantastic guide, pointing you toward options selling strategies that are a much better fit for your real comfort level. That's how you avoid unnecessary stress and build a trading plan that you can actually stick with for the long haul.

At Strike Price, we turn these insights into action. Our platform helps you use your risk profile to find covered call and put opportunities that perfectly match your score, balancing safety and yield. Transform your trading from guesswork to a data-driven strategy.