Intrinsic vs Extrinsic Option Value: Key Differences Explained

If a stock moves past your strike, the option can be assigned — meaning you'll have to sell (in a call) or buy (in a put). Knowing the assignment probability ahead of time is key to managing risk.

Posted by

Related reading

A Step-by-Step Covered Calls Example for Consistent Income

Unlock consistent income with our step-by-step covered calls example. This guide breaks down the strategy, risks, and outcomes to help you trade confidently.

Long Call and Short Put The Ultimate Synthetic Stock Guide

Unlock the power of the long call and short put strategy. This guide explains how synthetic long stock works, its benefits, risks, and how to execute it.

What is a Call Spread? A Clear Guide to Bull and Bear Spreads

What is a call spread? Discover how bull and bear spreads limit risk and sharpen your options trading strategy.

The real difference between intrinsic and extrinsic value is pretty straightforward. Think of intrinsic value as the actual cash value an option has if you exercised it this very second. Extrinsic value, on the other hand, is all about potential—it’s the speculative juice priced in based on time and how much the market expects the stock to move.

An option's total price, its premium, is just these two parts added together.

Decoding the Price of an Option Premium

Before you even think about placing a trade, you need to know what you’re paying for. Every option premium is a mix of two different components, and each one tells you something important about the contract's real worth. Peeling back the layers of the premium helps you look past the sticker price and see what an option is truly made of.

These two components are:

- Intrinsic Value: This is the real-deal, measurable value. It only exists for in-the-money (ITM) options and is the instant profit you’d make if you exercised. It's the simple, black-and-white part of the price.

- Extrinsic Value: People often call this "time value," and it's the speculative side of the coin. It’s what traders are willing to pay for the chance that an option will become even more profitable before it expires, fueled by things like time decay and market jitters.

An option's premium is a blend of reality and potential. Intrinsic value is the reality—what it's worth right now. Extrinsic value is the potential—what it could be worth down the road.

The mix between these two is critical. For an option with about 30 days left, it's not uncommon for extrinsic value to make up 50%-60% of its total premium, especially when implied volatility is high. This dynamic is the key to understanding how options are priced and why their values are always changing. You can dig into more options pricing data on Nasdaq.com.

To see exactly how these values add up, check out our guide on how to calculate an option premium. The formula couldn't be simpler: Option Premium = Intrinsic Value + Extrinsic Value. Getting this equation down is your first step toward making smarter trades.

Calculating an Option's Intrinsic Value

Let's get down to the brass tacks. Intrinsic value is the option's real, tangible worth—it's what you'd pocket if you exercised the contract right now. Think of it as the straightforward part of the premium, tied directly to where the stock is trading relative to your strike price. For an option to have any intrinsic value at all, it must be in-the-money (ITM).

One hard rule to remember: intrinsic value can never be negative. If a formula gives you a negative number, the intrinsic value is simply zero. This is just common sense. You wouldn't exercise an option to lock in a loss, so its immediate value in that situation is nothing.

The Simple Formulas for Intrinsic Value

Figuring out the intrinsic value is just basic math, with a slight difference between calls and puts. Once you get these two simple formulas down, you can instantly see an option's concrete value.

For Call Options: A call option is ITM when the stock's current price is above the strike price.

- Formula:

Intrinsic Value = Current Stock Price - Strike Price

Let's say XYZ stock is trading at $155 and you're holding a call option with a $150 strike. The math is $155 - $150 = $5. That option has $5 of intrinsic value per share. Simple.

For Put Options: A put option is the opposite—it's ITM when the stock's current price is below the strike price.

- Formula:

Intrinsic Value = Strike Price - Current Stock Price

So, if XYZ is at $155 but this time you have a put option with a $160 strike, the calculation is $160 - $155 = $5. This put option also has $5 of intrinsic value per share.

The core difference between intrinsic vs extrinsic option value is certainty. Intrinsic value is a known quantity based on current prices, while extrinsic value is a speculative premium paid for future potential.

Nailing this calculation is the first step to really understanding an option's total price. It lets you peel back the layers and separate the real value from the fluff—the part driven by time and volatility. For anyone selling options for income, this distinction is absolutely essential for making smart decisions.

Decoding Extrinsic Value: Time and Volatility

While intrinsic value is all about an option's here-and-now worth, extrinsic value is a bet on the future. Think of it as the time value — it’s the extra premium traders pay for the chance that an option could become even more profitable before it expires. This premium for uncertainty is shaped by two key forces.

The biggest driver is simply time to expiration. An option with six months left on the clock has way more extrinsic value than one expiring tomorrow. Why? Because more time means a wider range of possible price moves, increasing the odds that the option could end up in the money.

This brings us to the second force: implied volatility. This metric is the market’s best guess of how much a stock’s price will swing. Big uncertainty—like right before an earnings report or major news—pumps up implied volatility, which inflates an option's extrinsic value. Traders will pay more for options on jumpy stocks because the potential for a huge price swing is greater. If you want to dive deeper, check out our guide on how to calculate implied volatility.

The Unstoppable Force of Time Decay

Extrinsic value is a melting ice cube. This predictable erosion of value is known as theta decay, a concept every options trader has to burn into their brain. As an option gets closer to its expiration date, its potential for future movement shrinks, and its extrinsic value evaporates along with it.

This decay isn't a slow, steady drip; it accelerates, especially in the final 30-45 days. For an option with more than 45 days left, it's not unusual for 70%-90% of its premium to be extrinsic value. But in that last week, it can plummet to under 20%.

Theta decay is the enemy of the option buyer but the best friend of the option seller. Sellers aim to profit directly from this predictable daily erosion of an option's premium.

For buyers, the clock is always ticking against them. But for sellers using strategies like covered calls, this decay is exactly where they make their money.

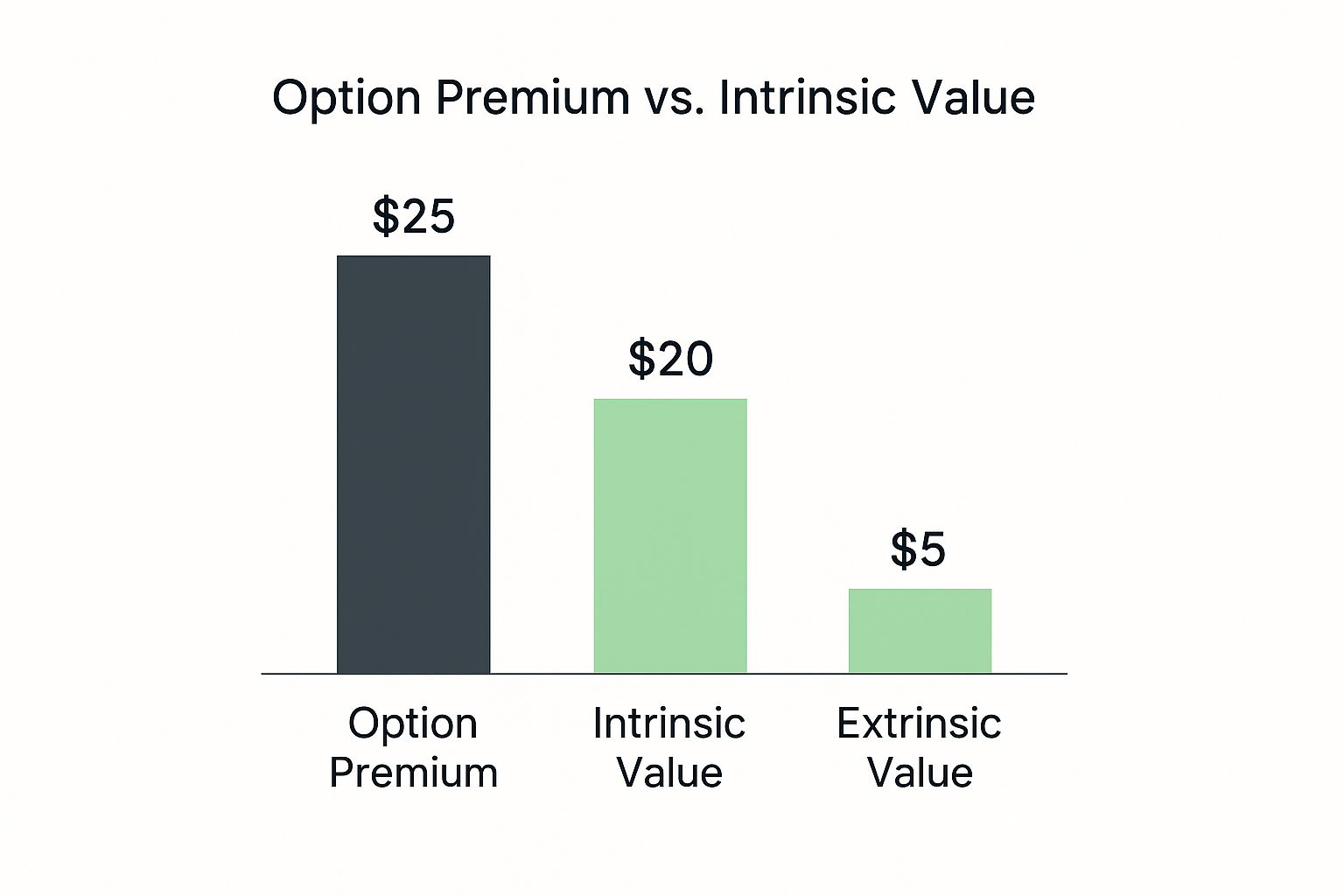

A Practical Comparison of Intrinsic and Extrinsic Value

To make smart options trades, you first have to understand what you're actually paying for. Every option's price, or premium, is made of two distinct parts: intrinsic value and extrinsic value. They work together but come from completely different places and behave in opposite ways.

Think of it this way: intrinsic value is the real, tangible value an option has right now if it were exercised. Extrinsic value is the speculative part—the premium paid for the potential of what could happen between now and expiration.

This image breaks down how an option premium is split into these two core pieces.

As you can see, the total price is a simple sum of its current, factual value and its future, hopeful value.

Dissecting the Key Differences

Let's put these two value types head-to-head to really see how they differ. This side-by-side comparison makes it clear why they play such different roles in an option's price and your trading strategy.

Intrinsic vs Extrinsic Value Key Differences

Here’s a quick breakdown of the core differences that every options trader should know.

| Attribute | Intrinsic Value | Extrinsic Value |

|---|---|---|

| Source of Value | The direct relationship between the stock price and the strike price. | Time left until expiration and the stock's implied volatility. |

| Certainty | Factual and can be calculated precisely. It's a known quantity. | Speculative and uncertain. It’s a bet on future price movement. |

| Behavior Over Time | Stable. It only changes if the underlying stock price moves. | Always decaying (theta decay), and this decay speeds up as expiration gets closer. |

| Existence | Only exists for in-the-money (ITM) options. | Exists for all options until the moment they expire. |

This table shows the fundamental tug-of-war within every option premium. One part is real and stable, while the other is based on probability and constantly losing value.

Here's a real-world example: A Tesla (TSLA) call option with a strike price of $162.50 while the stock was trading at $166.11 had an intrinsic value of $3.61. The option's total premium was around $7.27. That means the remaining $3.66 was pure extrinsic value—the amount traders were willing to pay for the chance that TSLA would climb even higher before expiration. You can find more practical examples on Optionsamurai.com.

Intrinsic value is what you have. Extrinsic value is what you hope for. Recognizing which one you are paying for is the foundation of a sound options strategy.

Practical Implications for Traders

This isn't just theory; it directly shapes your trading strategy.

When you buy an option, you pay for both values. To profit, the stock must move enough to build intrinsic value faster than the extrinsic value is decaying away. You're in a race against the clock.

On the other hand, if you're an option seller, your main goal is to pocket the extrinsic value as it predictably melts to zero. You are essentially selling that "hope" premium to buyers, turning the certainty of time decay into your potential income. Knowing this dynamic is critical to matching your strategy with your goals.

How Option Sellers Leverage Extrinisic Value

For option sellers, the difference between intrinsic and extrinsic value isn't just theory—it's the entire game. Option buyers are betting on a big price move to create intrinsic value, but sellers are playing a different hand. They focus on a much more reliable force: the slow, steady decay of extrinsic value. This decay is the profit engine for any income-focused options strategy.

When you sell a covered call or a cash-secured put, you pocket a premium right away. That premium is your maximum possible profit, and it's almost all extrinsic value. Your goal is for this "time value" to melt away to zero by expiration, letting you keep the full amount without the option ever being exercised.

Turning Time Decay into Income

The core strategy is simple: you're selling time and volatility to someone else. You’re collecting cash from buyers who are speculating that a stock will make a big move. The perfect scenario for a seller is for the underlying stock to go nowhere or move only slightly against them, giving time decay all the room it needs to work its magic.

For an option seller, extrinsic value is a perishable good they sell at full price. Their profit comes from the certainty that its value will diminish every single day.

This approach works especially well when you sell options with 30 to 45 days left until expiration. In this window, time decay (theta) really kicks into high gear, causing the extrinsic value to evaporate much faster. It's the sweet spot that balances a decent premium with a rapid decay timeline. To really get this down, it helps to understand the fundamentals of generating consistent options trading for income.

Selecting the Right Options to Sell

The key is finding options with plenty of extrinsic value but a low chance of moving deep in-the-money. This usually means selling at-the-money (ATM) or slightly out-of-the-money (OTM) contracts. These are the options with the most "air" in them—the highest extrinsic value and, therefore, the most premium to decay.

By selling these contracts, you're positioning yourself to profit from the market’s tendency to overestimate how much a stock will actually move. You collect a premium for taking on a calculated risk and let the predictable march of time do the heavy lifting for you.

Common Questions About Option Value

As traders start digging into intrinsic vs extrinsic option value, a few key questions always pop up. Getting these points straight is the difference between guessing and having a real strategy. Let's tackle some of the most common ones.

Think of this as the practical side of the theory. Once you nail these concepts, you'll be able to look at any option's price and know exactly what you’re paying for. That clarity is crucial whether you're buying options for a big speculative bet or selling them to generate steady income.

Can an Option Have Only Extrinsic Value?

Yes, absolutely. In fact, most options traded fall into this category.

Any option that is at-the-money (ATM) or out-of-the-money (OTM) has zero intrinsic value. Its entire price tag is made up of extrinsic value. What you're really paying for is time and possibility—the market's bet that the stock could move in your favor before the contract expires.

That's why even an option that seems hopelessly out-of-the-money still costs something. You're buying a lottery ticket, and that potential has a price.

How Do Earnings Reports Affect Extrinsic Value?

Earnings announcements are where things get really interesting for extrinsic value. They are massive, scheduled events of pure uncertainty, and that uncertainty pumps up an option's premium like nothing else.

In the days leading up to an earnings report, implied volatility often skyrockets. Since volatility is a key ingredient in extrinsic value, the option's price swells.

But the moment the earnings numbers are out, all that uncertainty disappears. Volatility plummets, and the extrinsic value collapses right along with it. Traders call this the "volatility crush," and it can wipe out an option's premium even if the stock moves in the right direction.

Should a Buyer Focus on Intrinsic or Extrinsic Value?

It completely depends on your goal. There’s no single right answer, just the right tool for the job.

- Buying for Leverage: If you want to capitalize on a stock that's already moving, you might buy a deep in-the-money option. This contract is almost entirely intrinsic value and moves nearly point-for-point with the stock, giving you a powerful, leveraged position.

- Buying for Speculation: On the other hand, if you're betting on a big, unexpected price swing, you might buy a cheap, out-of-the-money option. This contract is 100% extrinsic value. You're essentially betting that some future event will create intrinsic value before time decay eats away your entire premium.

The right focus depends entirely on your strategy. A trader wanting to leverage an existing stock move might buy a deep in-the-money option, which is mostly intrinsic value. In contrast, a speculator might buy a cheap, OTM option that is 100% extrinsic value.

Ready to stop guessing and start making data-driven decisions? Strike Price provides real-time probability metrics to help you find the safest and most profitable covered call and put selling opportunities. Turn your options strategy into a consistent income stream.